da-kuk/E+ through Getty Photos

It’s been about 22 months since I walked away from Gentex Company (NASDAQ:GNTX), and since I offered, the shares have returned one other 15% towards a achieve of ~44% for the S&P 500. A charitable learn of that is that I walked away from an organization that will go on to underperform the S&P 500. Since I’m seemingly in a everlasting “glass half empty” state of mind, my method of deciphering it’s that I walked away too quickly and missed out on some additional upside. A small voice in my head would possibly remind me that whereas I held the shares they outperformed the market, however I hardly ever take note of that a part of myself.

At present I wish to work out whether or not or not it is sensible to purchase again in, because the shares have truly declined a good bit over the previous 12 months. I’ll make that willpower by wanting on the monetary historical past right here, and by wanting on the inventory as a factor distinct from the underlying enterprise. Additionally, though I offered my shares, I additionally offered put choices on the enterprise, and that commerce labored out very nicely. For that motive, I completely want to jot down about my choices commerce.

It’s that point once more. It’s the time once I supply up my “thesis assertion” paragraph to readers who’re thinking about my perspective, however in no way thinking about wading by my verbiage. I’ll come proper to the purpose. I feel Gentex inventory stays very costly, despite the truth that the enterprise has simply posted mediocre outcomes. I’m additionally of the view that investments are relative to one another, and in a world the place you possibly can clip 2.9% from a authorities observe, why would you purchase a sluggish grower like this that’s at the moment yielding a a lot decrease dividend? I made superb cash on this identify prior to now, and can be keen to once more, however for now I’m nonetheless avoiding the identify.

Monetary Snapshot

I’m simply gonna come out with it. For my part, the monetary efficiency in 2021 was mediocre. Gross sales in 2021 had been barely (about 2.55%) greater, and internet earnings was up by lower than 4%, relative to 2020. On condition that 2020 was no nice shakes, that’s not an amazing accomplishment in my opinion. When in comparison with 2019, the newest 12 months seems to be even worse. Gross sales in 2021 had been about 7% decrease, and internet earnings was down totally 15% relative to the pre-pandemic interval.

Turning now to the quarter simply introduced this morning, plainly issues have gone within the fallacious route. Particularly, gross sales are down aboot 3.2% relative to 2021, and the primary quarter of 2022 noticed internet earnings totally 22.85% decrease than the 12 months in the past interval. There’s not a lot to get enthusiastic about right here in my opinion.

All that mentioned, the stability sheet stays a optimistic standout, and is among the strongest I’ve seen. That is evidenced by the truth that as of their newest reporting date, the corporate had money on the books of $262.3 million, and complete liabilities equaled solely $193.4 million. Thus, I don’t assume debt or curiosity bills will crowd out dividend funds anytime quickly. Talking of the dividend…

The whole lot’s Relative

I’ve acquired a confession to make, pricey readers. I’ve the capability to be fairly unpleasant. Please comprise your shock. One of many many ways in which this has manifested through the years is by the truth that I used to be all the time bothered by the argument that individuals had been compelled to purchase shares as a result of authorities bonds supplied such paltry returns. It all the time bothered me that buyers with decrease threat tolerances had been pushed into shares as a result of there’s no various (and likewise as a result of we on Bay Road acquired paid extra once we jammed purchasers into equities). That dynamic appears to be reversing itself in my opinion. Now that buyers can gather 2.92% from 10-year treasury notes, how ought to they give thought to the dividend yield of a given inventory?”

That is clearly a really complicated query, with many variables, however I feel a useful first step in deciding what we’d be keen to pay for shares can be to have a look at the money flows between a 10-year Treasury observe and a given inventory. The inventory might get a valuation “bonus” from potential development, however I feel it’s worthwhile figuring out how a lot of the present worth is a perform of that development, and the way a lot is a perform of the money buyers can pocket.

In assist of answering the primary a part of this query, I’ve created a easy spreadsheet that tries to begin to sort out this query. It compares the money flows from each the treasury and the inventory over a 10-year interval. It additionally compares the fixed money flows from the treasury to rising dividends on the fairness. I assume the dividend will develop on the identical price for the subsequent decade because it did for the interval 2015-2019. That is clearly a quite simple assumption, and gained’t be good, clearly, however I feel it’s going to assist supply some perception into the relative funding deserves of every asset.

I’ve utilized this software to Gentex with the next beginning guidelines, and have discovered the next:

-

The investor can make investments $20,000 in both the treasury or they will make investments that $20,000 to purchase precisely 699 shares of Gentex.

-

Within the state of affairs the place Gentex doesn’t increase its dividend over the subsequent decade, the treasury investor finishes with an additional $2,380 in money flows, or an additional 11.9% of the unique funding.

-

Within the state of affairs the place Gentex raises its dividend at a price of three%, the treasury investor finishes with an additional $1,8760.28 or 9.38% of the unique funding.

For my part, this evaluation means that for an investor to be detached between Gentex inventory, and a 10-year U.S. Treasury observe, they’d must assume two issues. First, that the corporate will develop its dividend over the subsequent decade on the price that it did over the interval 2015-2019. Second, that the shares will admire by ~9.5% from now to 2032. Alternatively, if the corporate doesn’t increase the dividend, it’ll want to understand by slightly below 12% between now and 2032.

This software doesn’t reply the query “shares or bonds” definitively, clearly. It doesn’t discuss in regards to the dangers related to every funding, and there are apparent, and enormous, variations between the dangers of the inventory versus the U.S. authorities. That mentioned, I feel it’s a worthwhile first step. It helps quantify the relative deserves of every, which fits a protracted method to answering the query in my opinion.

Lastly, I ought to say that some variables are a wash. Inflation, for example, will influence $1 obtained from a dividend identically as will influence $1 obtained from Uncle Sam. There are probably vital tax variations for Individuals, although. Dividends are taxed in a different way, so chances are you’ll wish to issue your individual relationship with the Inside Income Service into this evaluation. Or, this evaluation could also be related to tax sheltered property.

In closing, I feel this software helps to quantify the variations between shares and authorities bonds in the intervening time. I’d recommend that basically, shares are extra dangerous, and are paying buyers much less within the phrases of money flows. Thus, buyers are actually reliant on worth appreciation stemming from both earnings development or a number of enlargement. For my part, it is a fairly heavy carry. Regardless of that, I’d be snug shopping for the shares on the proper worth.

Gentex dividend v 10 Yr Treasuries (Writer calculations primarily based on public sources)

Gentex Finanacials (Gentex investor relations)

The Inventory

A few of you who comply with me repeatedly for some motive know what time it’s. It is the purpose within the article the place I flip much more bitter, as a result of I begin writing about risk-adjusted returns, and the way a inventory with a well-covered dividend generally is a horrible funding on the fallacious worth. Even when an organization grows earnings properly, which isn’t the state of affairs right here, the funding can nonetheless be a horrible one if the shares are too richly priced. It is because this enterprise, like all companies, is an organisation that takes a bunch of inputs, provides worth to them, after which sells them for a revenue. That is all a enterprise is within the remaining evaluation. The inventory, alternatively, is a proxy whose altering costs mirror extra in regards to the temper of the gang than something to do with the enterprise. For my part, inventory worth modifications are rather more in regards to the expectations of an organization’s future, and the whims of the gang than something to do with the enterprise. This is the reason I have a look at shares as issues other than the underlying enterprise.

Should you had been hoping that I’d cease blathering about this, and transfer on to my subsequent level, you’d be fallacious, pricey reader. I wish to drive dwelling the significance of wanting on the inventory as a factor distinct from the enterprise by utilizing Gentex itself for example. The corporate solely launched quarterly outcomes this morning, so there’s no historical past to be guided by but, so I’ll have a look at the interval between the discharge of their newest annual outcomes by to yesterday. The corporate launched annual outcomes on February twenty third. Should you purchased this inventory that day, you are down about 3.3% since then. Should you waited till April seventh to select a date completely at random, you are up about 4% since. Clearly, not a lot modified on the agency over this quick span of time to warrant a 7% variance in returns. The variations in return got here down completely to the value paid. The buyers who purchased nearly an identical shares extra cheaply did higher than those that purchased the shares at a better worth. This is the reason I attempt to keep away from overpaying for shares.

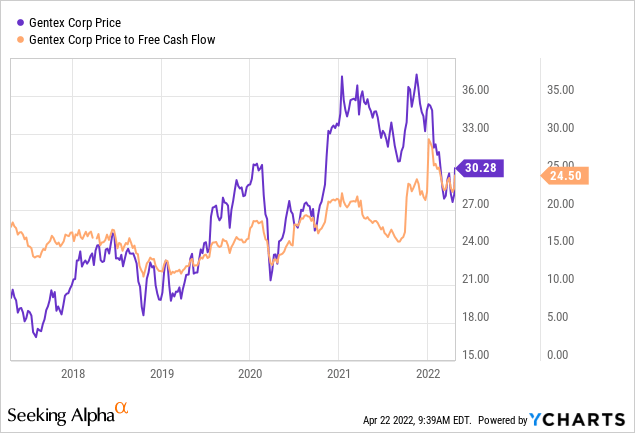

Should you’re one of many masochists who reads my stuff usually, you already know that I measure the cheapness of a inventory in a couple of methods, starting from the easy to the extra complicated. On the easy aspect, I have a look at the ratio of worth to some measure of financial worth like gross sales, earnings, free money movement, and the like. Ideally, I wish to see a inventory buying and selling at a reduction to each its personal historical past and the general market. In my earlier missive, one of many causes I walked away was as a result of the shares had hit a worth to free money ratio of 15.27. This was 24% costlier than the value that excited me initially. Regardless of the fairly massive drawdown in worth over the previous 12 months, issues are much more costly now, per the next:

Supply: YCharts

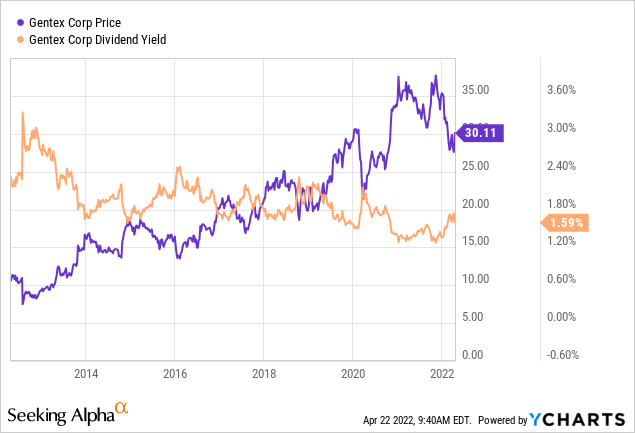

On the identical time that shares are priced close to document valuations, buyers are getting close to low dividend yields. I do not know aboot you, pricey reader, however I do not like paying extra and getting much less.

Supply: YCharts

Along with easy ratios, I wish to attempt to perceive what the market is at the moment “assuming” about the way forward for this firm. In an effort to do that, I flip to the work of Professor Stephen Penman and his guide “Accounting for Worth.” On this guide, Penman walks buyers by how they will apply the magic of highschool algebra to a typical finance method to be able to work out what the market is “considering” a few given firm’s future development. This includes isolating the “g” (development) variable within the mentioned method. Making use of this strategy to Gentex in the intervening time suggests the market is assuming that this firm will develop at a price of about 4.5% over the long run. That is fairly optimistic in my opinion, particularly in mild of the truth that internet earnings continues to slip decrease. Given all of this, I am taking my chips off the desk right here.

Choices Scale back Threat, Improve Returns

Whereas I took earnings in June of 2020, I offered 10 December Gentex places with a strike of $20 for $0.70 every, and these expired worhthless, and that enhanced my returns properly. I level this out to be able to brag most significantly, but additionally to exhibit but once more how quick put choices supply the chance to boost returns whereas reducing threat. Had the shares fallen, I’d have been obliged to purchase at an amazing worth of $19.30. Because the shares remained above this strike worth, these places expired nugatory, which was additionally an amazing consequence.

Whereas I wish to attempt to repeat success once I can, I can’t do it on this case as a result of the premia on supply for cheap strike costs is non-existent. For example, I’d be keen to promote the December Gentex put with a strike of $20, however the bid on these is at the moment zero. Thus, I have to merely watch for the shares to drop additional in worth earlier than contemplating shopping for again in.

Conclusion

I feel the shares of Gentex stay costly, despite the truth that the corporate has simply posted mediocre outcomes. That is notably troubling in mild of the truth that an investor can now clip 2.9% on a “sleep at evening” commerce. I made good cash on this inventory prior to now, and I’d be joyful to purchase again in on the proper worth. The issue is that we’re not close to that worth at the moment.