Mario Tama/Getty Photographs Information

With the subscriber loss in 1Q22 and steering for additional subscriber deterioration in 2Q22, the weaknesses in Netflix’s (NASDAQ:NFLX) enterprise mannequin are plain, as we have been stating for years. Even after falling 67% from its 52-week excessive, 56% from our report in April 2021 and 39% since our report in January 2022, we predict the inventory has far more draw back.

Robust competitors is taking market share, limiting pricing energy, and making it clear that Netflix can’t generate something near the expansion and earnings implied by the present inventory worth.

First Subscriber Loss In Over 10 Years Ought to Not Be A Shock

Netflix misplaced 200,000 subscribers in 1Q22, which is effectively under its prior steering for two.5 million additions and is the corporate’s first subscriber loss in 10 years. Extra alarming, administration guided for a further lack of 2 million subscribers in 2Q22.

We anticipate subscriber contraction could possibly be the norm shifting ahead, as famous in our January 2022 report as a result of competitors is taking significant market share and Netflix’s constant worth will increase are clearly not effectively obtained in such a aggressive market.

We anticipate Netflix will proceed to lose market share as extra opponents bolster their choices and deep-pocketed friends corresponding to Disney (DIS), Amazon (AMZN), and Apple (AAPL) proceed to take a position closely in streaming.

Aggressive Pressures Have Undermined Subscriber Development For Years

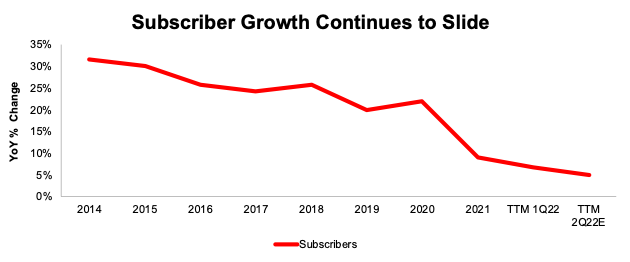

Whereas Netflix plans to proceed rising its content material spending “relative to prior years”, it is not clear that could be a successful technique to spice up subscriber development. Per Determine 1, Netflix’s subscriber development has fallen from 31% YoY in 2014 to 7% YoY within the trailing twelve months led to 1Q22.

Netflix’s steering, which requires a lack of 2 million subscribers, implies subscriber development of simply 5% YoY within the TTM ended 2Q22.

Determine 1: YoY Subscriber Development Charge Since 2014

NFLX Subscriber Development YoY Since 2014 (New Constructs, LLC)

Income Development Follows A Related Path

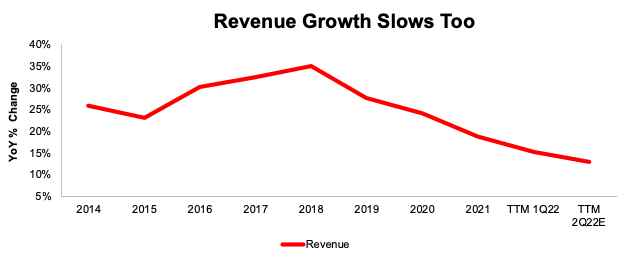

In its 1Q22 earnings press launch, Netflix acknowledged “excessive family penetration, mixed with competitors, is creating income development headwinds.” As well as, administration famous “the massive COVID enhance to streaming obscured the image till lately.” Nonetheless, slowing income development is nothing new.

The truth is, Netflix’s income development has fallen from 26% YoY in 2014 to fifteen% YoY within the TTM ended 1Q22. Administration’s steering implies income development falls even additional, to only 13% YoY within the TTM ended 2Q22.

Determine 2: YoY Income Development Charge Since 2014

NFLX Income Development YoY Since 2014 (New Constructs, LLC)

Advertisements To The Rescue? Or Simply Worse Person Expertise

Netflix, and significantly co-founder and co-CEO Reed Hastings, have lengthy been towards an ad-supported Netflix. Nonetheless, after the subscriber miss and weak steering, that stance could also be altering. On the 1Q22 earnings name, Hastings famous that an ad-supported plan would section in over a few years, whereas stressing that customers would nonetheless be capable of select an ad-free service.

Whereas an ad-supported service might assist the enterprise develop the top-line, shoppers largely do not get pleasure from ad-supported streaming platforms. An October 2021 survey by Morning Seek the advice of discovered of U.S. adults:

- 44% stated there are too many adverts on streaming companies

- 64% stated focused adverts are invasive

- 69% assume adverts on streaming companies are repetitive

- 79% are bothered by the expertise

Time will inform if shoppers flock to an ad-supported Netflix, however the information signifies it might immediately create a worse expertise.

Prime-Line And Subscriber Development Aren’t The Solely Points

Netflix faces a litany of challenges to show its cash-burning enterprise right into a money earner and justify the expectations baked into its inventory worth. Under, we current a quick abstract of these challenges. You will get extra in-depth particulars in our January 2022 report.

Netflix’s First Mover Benefit Is Gone

The streaming market is now house to a minimum of 15 companies with greater than 10 million subscribers, and plenty of of those opponents, corresponding to Disney, Amazon, YouTube (GOOGL), Apple, Paramount (PARA) and HBO Max (WBD) have a minimum of considered one of two key benefits:

- worthwhile companies that subsidize lower-cost streaming choices

- a deep catalog of content material that’s owned by the corporate, fairly than licensed from others

Tougher To Hike Costs With So Many Low-Value Alternate options

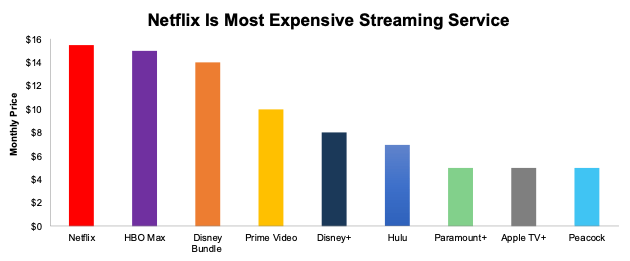

We underestimated Netflix’s capability to boost costs earlier than, however now that competitors is flooding the market, our thesis is enjoying out as anticipated. Netflix’s projection for subscriber losses in 2Q22 signifies that its latest worth hike, amidst a panorama of so many lower-priced alternate options, might have reached a ceiling for a way a lot shoppers can pay. Per Determine 3, Netflix now expenses greater than each different main streaming service. For reference, we use Netflix’s “Normal” plan and the equal packages from opponents in Determine 3.

Determine 3: Month-to-month Value for Streaming Companies within the U.S.

Netflix Value Vs Competitors (New Constructs, LLC)

Cannot Have Development And Money Flows

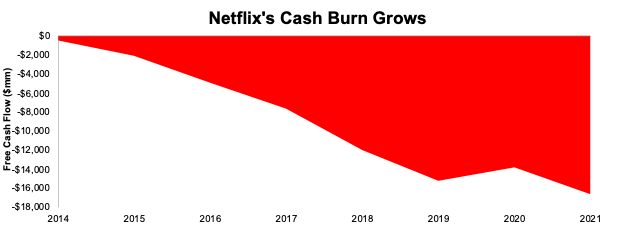

After constructive FCF in 2020, Netflix returned to its cash-burning methods, and generated -$2.8 billion in FCF in 2021. Since 2014, Netflix has burned by $16.6 billion in FCF. See Determine 4.

Determine 4: Netflix’s Cumulative Free Money Move Since 2014

Netflix Money Burn Since 2014 (New Constructs, LLC)

Heavy money burn is more likely to proceed provided that Netflix has one income stream, subscriber charges, whereas opponents corresponding to Disney monetize content material throughout theme parks, merchandise, cruises, and extra. Opponents corresponding to Apple, and Comcast/NBC Common (CMCSA) generate money flows from different companies that may assist fund content material manufacturing and decrease margins on streaming choices.

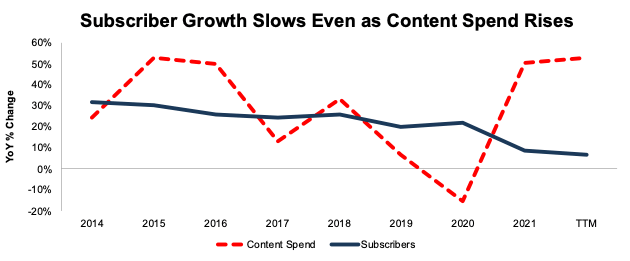

Large Pink Flag – Subscriber Development Fell Regardless of Content material Spend Rising

Netflix’s free money movement was constructive in 2020 for the primary time since 2010. However constructive FCF comes nearly completely from Netflix reducing content material spending through the COVID-19 pandemic. Netflix can’t generate constructive FCF and improve content material spending.

Prior to now, we noticed a robust relationship between content material spend and subscriber development. So, the spend appeared value it. As of yesterday’s earnings launch, we’re seeing that relationship break down.

Per Determine 5, even after considerably growing content material spend in 2021 and over the TTM, Netflix’s subscriber development continued to fall YoY. Contemplating the hyper-competitive, content material pushed nature of the streaming enterprise, an absence of subscriber development is a big crimson flag. Throwing billions of {dollars} at content material is not going to be sufficient to fend off competitors, and even when spending closely on content material, new subscribers aren’t displaying up.

Determine 5: Change in Subscriber Development & Content material Spend: 2014 – TTM

Netflix Subscriber Development YoY vs Content material Spend YoY Change Since 2014 (New Constructs, LLC)

Lack Of Reside Content material Limits Subscriber Development

Netflix has traditionally stayed out of the dwell sports activities area, a stance that appears unlikely to vary. Co-CEO Reed Hastings acknowledged in mid 2021 Netflix would require exclusivity that isn’t provided by sport leagues with a purpose to “provide our clients a secure deal.” For shoppers that require dwell content material as a part of their streaming wants, Netflix is both not an choice, or should be bought as a complementary service with a competitor.

In the meantime, Disney, Amazon, CBS, NBC, and Fox (every of which has its personal streaming platform) are securing rights to increasingly dwell content material, particularly the NFL and NHL, giving them a very fashionable providing that Netflix can’t match. Extra lately, Apple started broadcasting Friday Night time Baseball and it is reported that Apple is nearing a deal for NFL Sunday Ticket, which might solely bolster its dwell choices.

Netflix’s Present Valuation Implies Subscribers Will Double

We use our reverse discounted money movement mannequin and discover that the expectations for Netflix’s future money flows look overly optimistic given the aggressive challenges above and steering for additional slowing in person development. To justify Netflix’s present inventory worth of ~$220/share, the corporate should:

- keep its 5-year common NOPAT margin of 12% [1] and

- develop income 13% compounded yearly by 2027, which assumes income grows at consensus estimates in 2022-2023 and 12% annually thereafter (equal to 2022 income estimates)

On this state of affairs, Netflix’s implied income in 2027 of $59.5 billion is 4.4x the TTM income of Fox Corp (FOXA), 2.1x the TTM income of Paramount World, 1.5x the mixed TTM income of Paramount World and Warner Bros. Discovery (WBD) and 82% of Disney’s TTM income.

To generate this degree of income and attain the expectations implied by its inventory worth, Netflix would wish:

- 335 million subscribers at a median month-to-month worth of $14.78/subscriber

- 424 million subscribers at a median month-to-month worth of $11.67/subscriber

$14.78 is the typical month-to-month income per membership in america and Canada in 1Q22. Nonetheless, the vast majority of Netflix’s subscriber development comes from worldwide markets, which generate a lot much less per subscriber. The general (U.S. and worldwide) common month-to-month income per subscriber was $11.67 in 2021. At that worth, Netflix wants to almost double its subscriber base to over 424 million to justify its inventory worth.

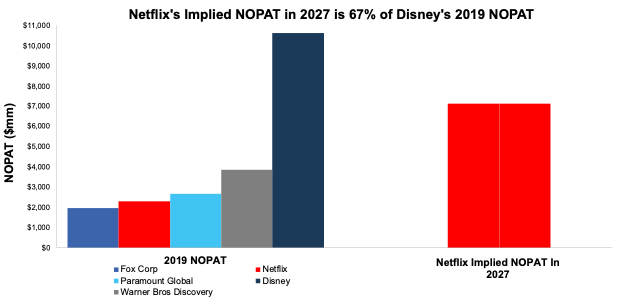

Netflix’s implied NOPAT on this state of affairs is $7.1 billion in 2027, which might be 3.6x the 2019 (pre-pandemic) NOPAT of Fox Corp, 1.9x the 2019 NOPAT of Paramount World, 1.1x the mixed 2019 NOPAT of Paramount World and Warner Bros. Discovery, and 67% of Disney’s 2019 NOPAT.

Determine 6 compares Netflix’s implied NOPAT in 2027 with the 2019 NOPAT[2] of different content material manufacturing corporations.

Determine 6: Netflix’s 2019 NOPAT and Implied 2027 NOPAT vs. Content material Producers

NFLX DCF Implied NOPAT vs Friends (New Constructs, LLC)

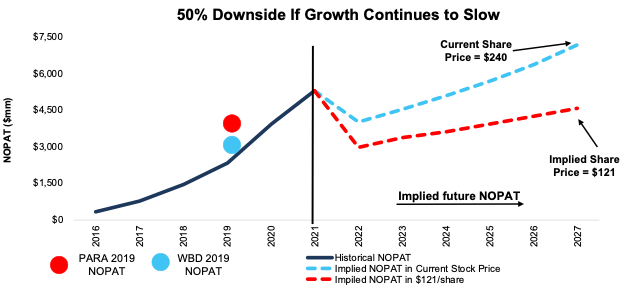

There’s Practically 50% Draw back If Margins Fall To Streaming Historical past Common

Ought to Netflix’s margins fall even additional given aggressive pressures, extra spending on content material creation, and/or subscriber acquisition, the draw back is even larger. Particularly, if we assume:

- Netflix’s NOPAT margin falls to 9% (equal to common since 2014) and

- Netflix grows income by 10% compounded yearly by 2027, (equal to administration’s guided YoY income development price for 2Q22) then

the inventory is value simply $121/share immediately – a forty five% draw back. On this state of affairs, Netflix’s income in 2027 can be $51.3 billion, which suggests Netflix has 289 million subscribers on the present U.S. and Canada common month-to-month worth or 367 million subscribers on the total common income per subscriber of $11.67/month. For reference, Netflix had 222 million subscribers on the finish of 1Q22.

On this state of affairs, Netflix’s implied income of $51.3 billion is 3.8x the TTM income of Fox Corp., 1.8x the TTM income of Paramount World, 1.3x the mixed TTM income of Paramount World and Warner Bros. Discovery and 70% of Disney’s TTM income.

Netflix’s implied NOPAT on this state of affairs can be 2.3x the 2019 (pre-pandemic) NOPAT of Fox Corp., 1.2x the 2019 NOPAT of Paramount World, 70% the mixed 2019 NOPAT of Paramount World and Warner Bros Discovery, and 43% of Disney’s 2019 NOPAT.

Determine 7 compares the agency’s historic income and implied NOPAT for the situations above for instance the expectations baked into Netflix’s inventory worth. For reference, we additionally embody the pre-pandemic NOPAT of Paramount World and Warner Bros. Discovery.

Determine 7: Netflix’s Historic NOPAT vs. DCF Implied NOPAT

NFLX DCF Implied NOPAT (New Constructs, LLC)

Possibly Too Optimistic

The above situations assume Netflix’s YoY change in invested capital is 14% of income (half of 2021) in annually of our DCF mannequin. For context, Netflix’s invested capital has grown 40% compounded yearly since 2014 and alter in invested capital has averaged 26% of income annually since 2014.

It’s extra possible that spending will must be a lot increased to attain the expansion within the above forecasts, however we use this decrease assumption to underscore the danger on this inventory’s valuation.

This text initially revealed on April 20, 2022.

Disclosure: David Coach, Kyle Guske II, and Matt Shuler obtain no compensation to jot down about any particular inventory, fashion, or theme.

[1] Assumes NOPAT margin falls to be nearer with historic margins as prices improve from pandemic lows. For instance, Netflix initiatives working margin between 19-20% in 2022, down from 21% in 2021.

[2] We use 2019 NOPAT on this evaluation to investigate the pre-COVID-19 profitability of every agency, given the pandemic’s affect on the worldwide financial system in 2020 and 2021 and the opposite enterprise segments of those friends.