[ad_1]

by Charles Hugh-Smith

For everybody ignored of the Fed’s hyper-financialized, hyper-globalized, hyper-inequality “new prosperity,” there’s all the time the cut price salmon cassarole.

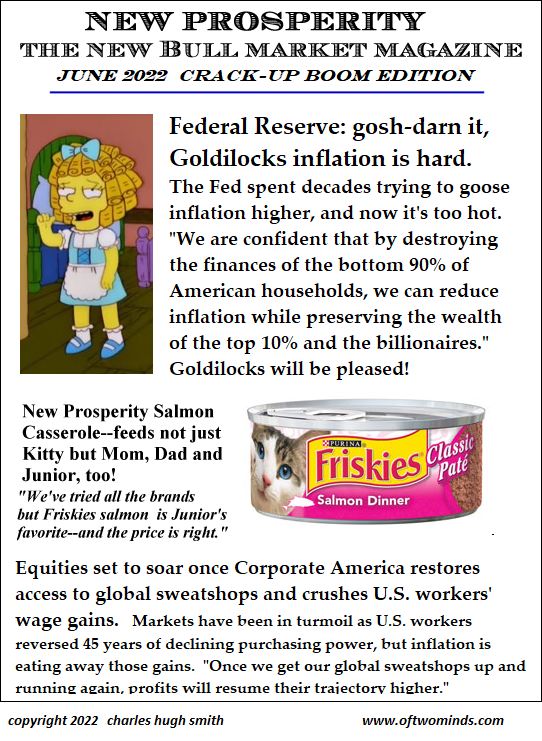

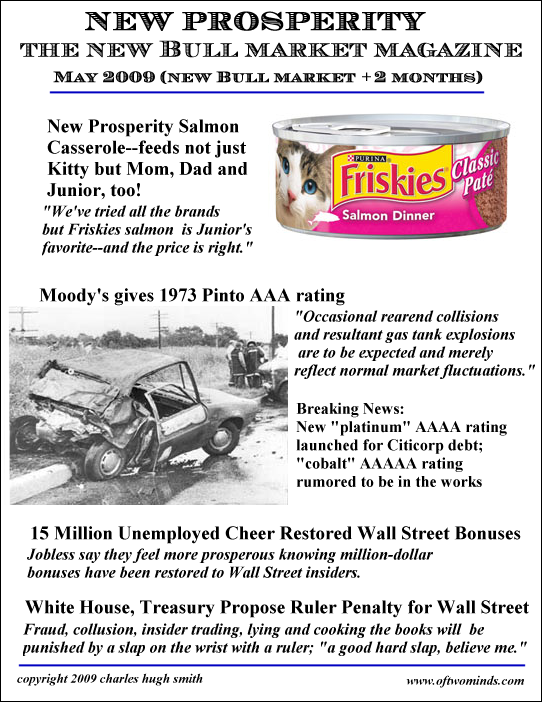

The most recent situation of New Prosperity Journal addresses the Fed’s “Goldilocks” inflation and the approaching crack-up increase. New Prosperity Journal’s maiden situation was revealed again in 2009, shortly after the World Monetary Meltdown had briefly disrupted the trajectory of prosperity. (The Could 2009 cowl is under.)

Curiously, the journal up to date a favourite cost-saving recipe for salmon casserole from the Could 2009 situation. Monetary meltdowns damage everybody who owns any of the property being repriced decrease, in fact, however they’ve a manner of wounding these dwelling paycheck to paycheck even tougher through rampant inflation of necessities and / or mass layoffs.

The Federal Reserve has a “Goldilocks” drawback with inflation: inflation was too chilly for the Fed’s style for the previous decade, and now instantly it’s too sizzling. The Fed received’t let something just like the monetary well-being of the underside 90% of American households get in te manner of its implicit objective, which is defending the wealth of the highest 10% and particularly the highest 0.01%.

To try this, the Fed should get well all the bottom misplaced to 2022’s spot of trouble in shares and bonds, and restore the trajectory of market beneficial properties towards ever-richer valuations. To perform that, the Fed will want a crack-up increase: a hybrid inflation which eviscerates labor’s modest beneficial properties in buying energy whereas massively inflating asset valuations.

Greater rates of interest are a headwind, to make certain, however a crack-up increase can nonetheless be managed if Company America can restore the World-Sweatshop-to-landfill conveyor belt that’s boosted earnings for many years.

The Fed will assist by herding all of the money sloshing round into equities. The first function of the “new prosperity” that started in 2009 is the inequality of its distribution: these with probably the most wealth and entry to low-cost credit score corralled the vast majority of the beneficial properties, whereas those that already owned the property that ballooned (housing and equities) did effectively just by being older than the generations coming into the workforce within the twenty first century.

For everybody ignored of the Fed’s hyper-financialized, hyper-globalized, hyper-inequality “new prosperity,” there’s all the time the cut price salmon casserole. Transfer over, Kitty-Cat, the entire household is sharing your supper.

Right here’s the present situation:

And right here’s the Could 2009 situation:

Latest podcasts/movies:

The Huge Issues And Crash Dynamics Of The Spring/Summer season 2022 Housing Market Disaster, Simplified (1:08 hr)

My new ebook is now out there at a ten% low cost this month: When You Can’t Go On: Burnout, Reckoning and Renewal.

If you happen to discovered worth on this content material, please be part of me in in search of options by turning into a $1/month patron of my work through patreon.com.

Assist Assist Impartial Media, Please Donate or Subscribe:

Trending:

Views:

19

[ad_2]

Source link