On April 5, I coated the bull case for Arch Assets (NYSE:ARCH), certainly one of North America’s largest coal mining firms. Since then, the inventory is up roughly 12%, outperforming the S&P 500 by roughly 26 factors. We’re now at some extent the place provide points meet even increased demand as Europe is compelled to return to coal. Not solely is pure fuel too costly, however strain from decrease Russian exports and expectations that Russia might halt all exports are additionally forcing coal energy to return. Whereas Arch coal has excessive metallurgical coal publicity, it advantages from sturdy pricing, an inexpensive valuation, and what might turn out to be a really chilly winter.

Now, let us take a look at the main points!

We Want Coal!

On June 27, I as soon as once more dove into the depths of the European/World vitality disaster. As my day by day publication is paywalled, I will offer you an important elements that specify why coal demand is again.

Listed below are three headlines that I coated in my article:

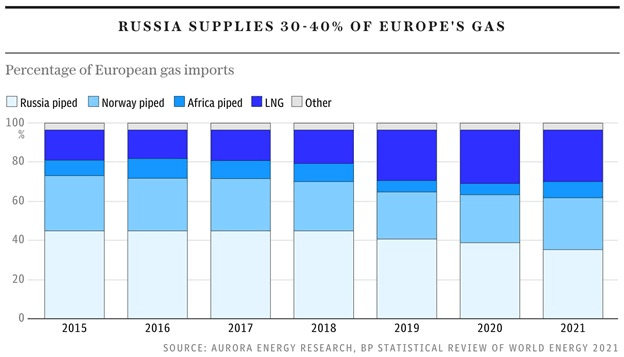

Primarily, now we have a scenario the place Russia might minimize off all pure fuel exports to Europe. Because of this Europe must discover a substitute for near 40% of its pure fuel imports.

The Telegraph

Nearly for sure, that is not a straightforward process. In reality, it is not potential in any respect.

Proper now, the European technique consists of two elements.

Hoping that Russia does not shut off pure fuel exports to Europe.

Saving as a lot pure fuel as potential.

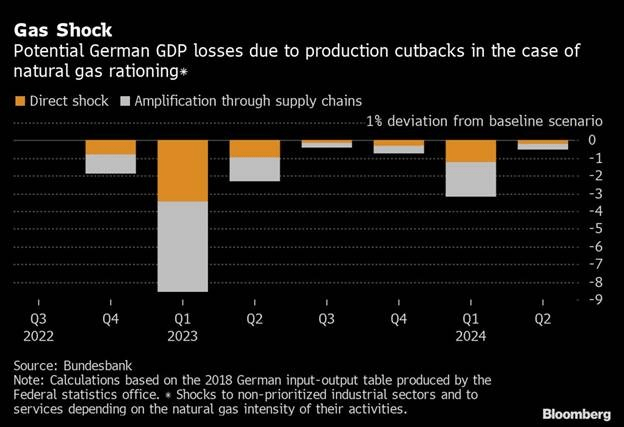

Why? As a result of a “fuel shock” might appear to be this:

Bloomberg

The German economic system alone might face a EUR 220 billion headwind, posing a much bigger threat than the pandemic lockdowns. Personally, I believe the scenario could possibly be even worse as pure fuel isn’t just an vitality supply, however feedstock for lots of chemical processes. The injury can be immense.

So, what does this imply? Saving pure fuel could be achieved by lowering vitality demand, but additionally by boosting coal manufacturing.

In line with the Monetary Occasions:

[…] Germany shouldn’t be alone in its new embrace of the black stuff. Final week the Dutch authorities, led by Mark Rutte, scrapped limits on energy manufacturing from coal-fired vegetation till 2024. And final weekend, Karl Nehammer’s authorities in Austria ordered a reserve fuel plant to modify to burning coal; the Mellach station was mothballed simply two years in the past, when Austria turned the second nation in Europe after Belgium to go coal-free.

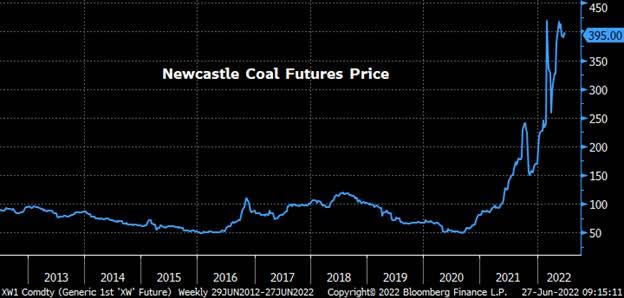

ICE Newcastle Coal futures present what is occurring. Demand is increased than anticipated, and provide is a matter as I’ll present you on this article. Therefore, coal is buying and selling greater than 5x above pre-crisis highs.

Bloomberg

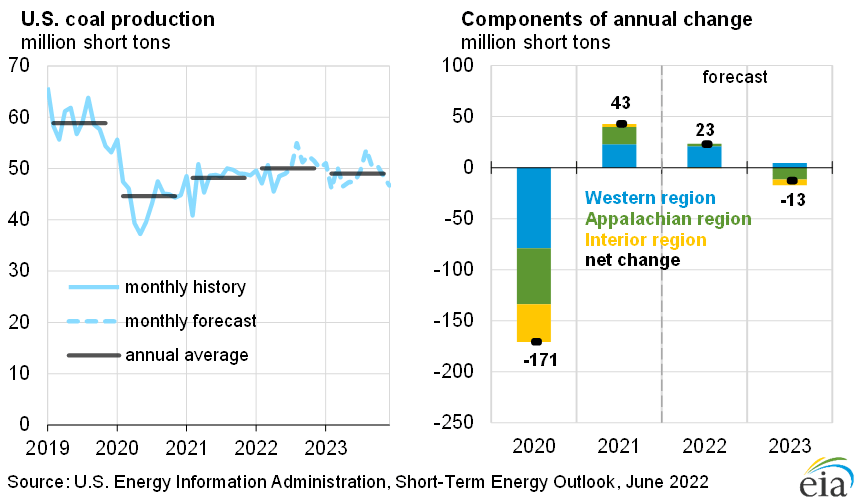

What’s attention-grabbing when taking a look at EIA information is that US coal manufacturing shouldn’t be anticipated to choose up meaningfully. In reality, it is anticipated to be caught at 50 million quick tons per 12 months, which is beneath the 60 million quick tons that have been produced previous to the pandemic.

EIA

Furthermore, it is attention-grabbing that Europe – and Asia – are diversifying towards liquified pure fuel (“LNG”). This permits Europe to turn out to be impartial from Russia (slowly however steadily) and Asia to turn out to be much less polluting. The issue is that the pattern is gradual and much from “climate-friendly”.

This can be a current Wall Avenue Journal headline:

Wall Avenue Journal

Between coal and the seek for LNG, the ESG pattern (setting, social, and governance) is in a really dangerous spot. One might say it is lifeless – for now.

That is the place Arch Assets is available in.

ARCH Is Nonetheless Low cost

The corporate, previously generally known as Arch Coal is a $2.42 billion greenback coal heavyweight. As I wrote in my April article:

Arch produces roughly 11% of the entire annual US metallurgical coal provide, which was estimated to be near 65 million tons in 2021. The corporate offered its product to 6 North American prospects and exported it to 24 prospects abroad in 15 nations final 12 months. All the firm’s metallurgical coal is produced within the state of West Virginia. Thermal coal is produced in Wyoming and Colorado.

Arch Assets (by way of SEC 10-Ok)

This 12 months and going ahead, Arch goals to generate 80% of its EBITDA from metallurgical coal. Notice that thermal coal volumes are increased, however because of decrease margins the impression from metallurgical coal is increased.

ARCH may be very export-focused. The corporate plans to ship 95% of its 2022 coking coal output into the 300 million metric tons per 12 months world seaborne metallurgical market. The corporate advantages from nice infrastructure together with rails and export amenities in addition to long-term contracts with metal producers and associated.

What’s attention-grabbing is that I personal shares in two of three railroads that service the corporate’s mines: CSX Corp. (CSX) and Union Pacific (UNP). BNSF is owned by Buffett.

Arch Assets (SEC 10-Ok)

Roughly half of its output is destined for Asian consumers.

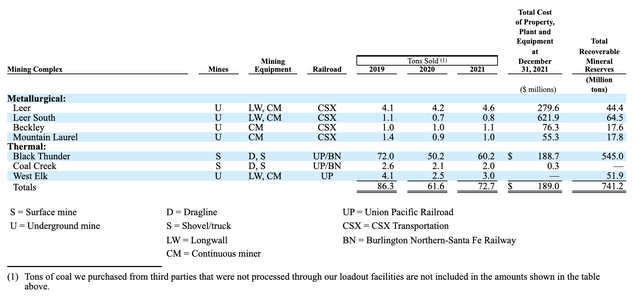

It additionally helps that the corporate has entry to reasonably priced manufacturing. For instance, its Leer mine produces at money prices of lower than $50 per ton. That is among the many least expensive producers on the planet.

Furthermore, EBITDA within the firm’s thermal phase has exceeded capital spending by 8x since 2016. The corporate expects this to widen additional thanks to raised thermal coal costs as I mentioned within the first a part of this text. If something, this tide lifts all boats. Each metallurgical coal and thermal coal are experiencing accelerating tailwinds as provide merely is not there.

Arch estimates that world coking coal demand can be 335 million metric tons in 2026. Provide is estimated to be 277 million metric tons, incorporating present operations and depletions. In different phrases, 58 million tons of provide should be discovered.

On a aspect notice, in its calculations, ARCH used a 2% annual depletion price, which is conservative.

Bringing again coal is not simple. Each coking and thermal coal manufacturing are “soiled” and whereas politicians transfer again to coal, none of them need to decide to bringing again provide on a long-term foundation. That might harm their ESG targets and local weather commitments. Even coal chief Australia is lowering output. In 2021, output was 168 million metric tons. That is down from 184 million tons previous to the pandemic.

As I defined in a variety of prior articles, a method out of the vitality disaster is to acknowledge that we’d like coal (and oil). I am under no circumstances an enormous fan of coal and I believe shifting to cleaner vitality is essential. Nonetheless, I am not somebody who likes compelled local weather targets and associated points. The transition must be very gradual with a purpose to keep away from provide shortages of any form and to keep away from hurting coal communities and reasonably priced vitality sources.

The best way “we” do issues now could be ending in a complete catastrophe.

Valuation

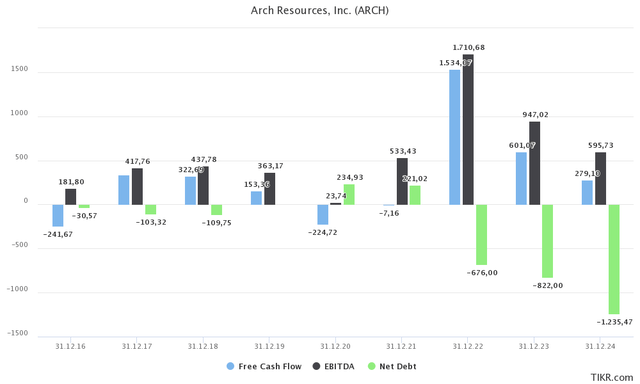

Even when coal costs implode subsequent 12 months (not a prediction), this 12 months is popping into a complete blessing – financially talking. Arch is on observe to do greater than $1.5 billion in free money circulation, greater than half of its present market cap. Adjusted EBITDA is predicted to come back in at $1.7 billion. That is greater than many prior years mixed. Because of this, web debt might fall to minus $680 million.

TIKR.com

In April – of this 12 months – estimates have been that free money circulation can be $1.0 billion. That is a 50% adjustment in only a few months.

On this case, giving the inventory a valuation is not simple. I do not need to use 2022 estimates as it will clearly be a “one-off” 12 months. Coal will stay sturdy, I imagine, however 2022 is shaping as much as be an outlier.

If we assume that 2022 can be good, we will use the decrease (anticipated) web debt load and subsequent 12 months’s EBITDA – assuming that analysts are improper in regards to the decline in coal costs within the 12 months forward. Identical to they missed coal’s upside potential this 12 months given their aggressive changes.

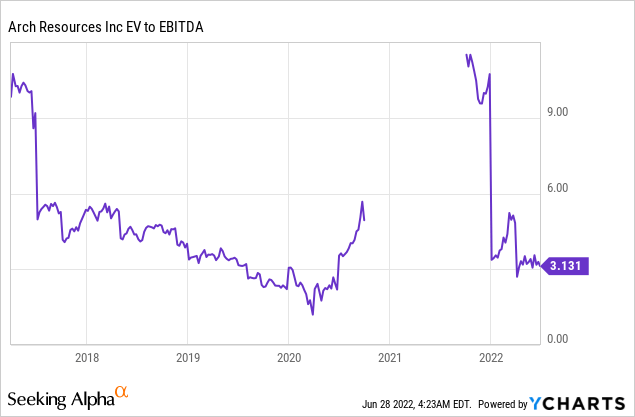

So, utilizing the $2.42 billion market cap, $680 million in web money (detrimental web debt), $75 million in pension-related liabilities, and $950 million in anticipated EBITDA offers the corporate an enterprise worth of $1.8 billion, and a 1.9x EBITDA a number of. This might have been even decrease if I used subsequent 12 months’s web debt expectations. This offers us a margin of security.

1.9x is extremely low cost – even for a coal firm. The a number of would nonetheless be truthful if I used the market cap as an alternative of (decrease) enterprise worth and 2024 EBITDA estimates (4.0x valuation).

Information by YCharts

Given these numbers, I imagine that ARCH has not less than 50% extra upside. This may be gradual over the subsequent 6-12 months or “all of the sudden” when issues began to worsen within the world vitality market.

In any case, this continues to be a headline-driven market with regard to the conflict in Ukraine and supply-related headlines.

Takeaway

Some time in the past I wrote that coal is again. Arch Assets’ EBITDA (and associated) estimates are quickly rising as there is not any means round coal anymore. The ESG playbook has been thrown out of the window as even essentially the most climate-committed nations on the planet at the moment are going again to coal vitality with a purpose to decrease pure fuel demand.

There isn’t any means round the usage of coal anymore as American, European, and Asian prospects are accelerating demand. One of many greatest beneficiaries is ARCH. The corporate has an export-oriented enterprise mannequin and advantages from each excessive margins in metallurgical coal and accelerating thermal coal demand.

Its steadiness sheet has turn out to be extraordinarily wholesome, which helps the corporate’s valuation.

ARCH is extraordinarily attractively valued, which makes my 50% upside estimate relatively conservative.

That being stated, coal is extraordinarily risky and the long-term outlook is unsure. In the event you’re not a dealer, do not begin buying and selling coal now – on your portfolio’s security. One purpose of this text was to tell individuals in regards to the vitality/coal market. Buying and selling coal shares is one thing solely skilled merchants ought to do.

FINVIZ

In the event you resolve to purchase ARCH, preserve your place restricted.

")