[ad_1]

A Uniform Industrial Code submitting, also called a UCC submitting, is a doc that lenders use to determine their authorized proper to belongings {that a} borrower makes use of to safe a mortgage. This discover permits the lender to grab the borrower’s collateral within the case of default.

UCC filings can cowl a particular piece of collateral, or lenders can file a blanket lien, which applies to all of a borrower’s belongings. Submitting a UCC lien is a typical follow amongst lenders once they challenge small-business loans.

Do you know…

The Uniform Industrial Code is a set of legal guidelines that govern industrial transactions throughout the U.S. These uniformly adopted state legal guidelines assist promote and simplify interstate enterprise. Article 9 of the Uniform Industrial Code gives tips for transactions secured by belongings or property, ensuing within the time period UCC submitting.

How does a UCC submitting work?

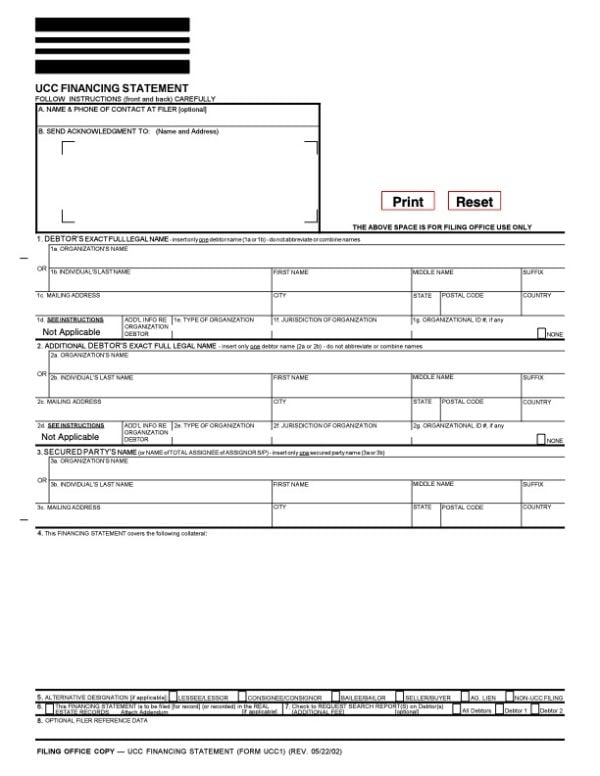

A UCC submitting offers a lender the first-position proper to say a borrower’s collateral within the case of mortgage default. UCC liens are usually filed utilizing a UCC financing assertion, additionally known as the UCC-1 financing assertion.

This doc is submitted to the secretary of state’s workplace within the state the place the enterprise (i.e., the borrower) is situated. The UCC-1 financing assertion identifies the belongings or properties the lender has declare to, and lets different collectors know of its safety curiosity in that collateral.

UCC-1 financing assertion for New York state.

UCC liens may be filed on a spread of non-public and/or enterprise belongings, together with however not restricted to actual property, stock, receivables, autos, equipment and gear.

As soon as a UCC lien is filed with the secretary of state’s workplace, it turns into public report, which means anybody can go browsing and seek for lively filings.

Though the specifics can range from state to state, UCC filings normally final for 5 years. In case your mortgage continues to be lively after that time frame, your lender can apply for a continuation of the lien. The lender also can file amendments or addendums to the assertion, if essential.

Kinds of UCC filings

There are two varieties of UCC filings that can be utilized to safe a enterprise mortgage.

-

UCC lien on particular collateral. Lenders can file a UCC lien on particular items of collateral, similar to actual property or gear. For those who default on your small business mortgage, the lender can declare these belongings to recoup its losses. Nonetheless, it might’t declare every other firm belongings.

-

Blanket lien. This kind of lien covers all of a enterprise’s belongings, not only a particular piece of collateral. For those who default in your mortgage, the lender can declare (and/or promote) any of the belongings it must cowl its losses.

The UCC submitting a lender makes use of can range based mostly on a wide range of elements, together with the sort of enterprise mortgage, your organization’s {qualifications} and the person lender itself.

Particular collateral liens are typically used for special-purpose loans, similar to gear or stock financing. Blanket liens, alternatively, are generally used for traditional financial institution loans, SBA loans and on-line loans.

How a UCC submitting impacts your small business

On the whole, a UCC submitting isn’t unhealthy for your small business — it merely serves as an official discover to different collectors that your lender has a safety curiosity in a single or your whole belongings. Nonetheless, UCC filings can affect your small business credit score, danger your organization’s belongings and/or hinder your skill to get future financing.

-

Impression on enterprise credit score. Though your credit score report will present any UCC filings taken out on your small business throughout the final 5 years, these liens don’t usually affect your small business credit score rating. For those who make late funds or default in your mortgage, although, your credit score may be negatively affected.

-

Danger your organization’s belongings. When a lender information a UCC lien, some or your whole belongings (relying on the kind of lien) are in danger in case you fail to pay again your mortgage. So long as you repay your lender, your belongings will stay protected. However, in case you don’t repay your mortgage, the lender can seize your belongings to get better its losses.

-

Hinder your skill to get future financing. A UCC submitting signifies {that a} lender has the primary place to say your collateral within the case of default. For those who determine to use for added financing, your new lender can search to see if your small business has any liens in opposition to it. In lots of circumstances, lenders are hesitant to take second place on an organization’s belongings and should deny your enterprise mortgage software — or supply restricted funding — you probably have an lively UCC submitting.

The right way to take away a UCC submitting

Even in case you repay a enterprise mortgage, any UCC submitting on that financing will stay lively till it expires — normally after 5 years. Eradicating a UCC lien on a mortgage that you simply’ve repaid can assist you qualify for different enterprise funding choices.

You’ll be able to take away a UCC submitting by asking your lender to submit a UCC-3 kind to terminate the lien.

For those who discover a UCC lien listed in your credit score report that shouldn’t be there, you may contact the credit score bureau (e.g., Experian, Dun & Bradstreet) and file a dispute to have it eliminated.

[ad_2]

Source link