[ad_1]

by David Haggith

Fed Chair Jerome Powell did the very best he may with the restricted choices the Fed has created for itself, and he stated nothing surprising. The Fed will proceed its course at a slower fee of rate of interest will increase however elevate curiosity to the next degree than it has thought it must all 12 months and better than the inventory market has believed.

All completely as anticipated right here, however inflicting the market to lose all of what little carry it obtained the day earlier than from the bettering inflation fee as a result of it didn’t anticipate sufficient.

Then The Fed and Powell’s presser smashed the vase of fantasy on the bottom of actuality with a hawkish assertion and projections and an much more hawkish Powell.

Zero Hedge

So, the S&P and Nasdaq stay sure throughout the bear-market buying and selling vary they’ve been in all 12 months, and the Dow, which broke out of that vary, seems to be to be headed again down into it.

Whereas there have been no surprises, one of many dominant themes was the blind spot I identified a number of months in the past that I stated the Fed would get hung up on, inflicting it to over-tighten because it strikes ahead. Powell took any doubt off of that by saying a number of instances throughout his ready speech and his Q&A time afterward that the one sign the Fed shall be watching greater than any to determine when to cease elevating rates of interest is a significant transfer up in unemployment.

The misunderstanding of languishing labor

Whereas Powell continues to say the labor market is powerful, he confirmed that that labor pressure (the variety of individuals ages 16 and older who’re employed or actively in search of employment) is badly damaged and gained’t doubtless recuperate for a while. He acknowledged the identical numbers I gave months in the past, which is that measurement of the general labor pressure is about 4,000,000 staff decrease than the place it might be if the longstanding and constant development for development within the taking part labor pressure had not been damaged by the Covidcrash. For the second time that I’ve heard (his Brookings discuss being the primary), Powell is now recognizing the contributing trigger I identified again in September, which is the variety of Covid-related deaths and diseases.

So, Powell is coming alongside in recognizing the labor market is damaged and why; but, he retains saying it’s robust as a result of there are much more jobs open than there are laborers. I preserve listening to that critical false impression far and wide:

AP repeated the error even when it wrote initially of this week in regards to the critical ramifications of the wounded labor pressure:

A diminished US workforce may lead Fed to maintain charges excessive

Nonetheless keen to rent, America’s employers are posting extra job openings than they did earlier than the pandemic struck 2½ years in the past. Downside is, there aren’t sufficient candidates. The nation’s labor pressure is smaller than when the pandemic struck.

The explanations differ — an surprising wave of retirements, a drop in authorized immigration, the lack of staff to COVID-19 deaths and diseases. The outcome, although, is that employers are having to compete for a smaller pool of staff and to supply steadily greater pay to draw them. It’s a development that might gas wage development and excessive inflation nicely into 2023.

In a latest speech, Federal Reserve Chair Jerome Powell pointed to the shortfall of staff and the ensuing rise in common pay as the first remaining driver of the worth spikes that proceed to grip the financial system….

But with value will increase nonetheless uncomfortably excessive, Powell and different Fed officers have underscored that they anticipate to preserve charges at their peak for an prolonged interval, presumably by way of subsequent 12 months.

AP

So, the modern information I gave months in the past in regards to the true scenario within the labor market is lastly filtering by way of the mainstream press: a part of the reason for the labor scarcity is Covid-related deaths and diseases (with out stating that some of what’s referred to as “lengthy Covid” may be vaccine accidents). They state that this shortfall in staff goes to proceed to gas wage inflation, which is able to gas normal inflation nicely into 2023.

Powell reiterated right now the next factors, which AP famous he made in latest speeches earlier than this week’s FOMC assembly:

In his latest speech, Powell famous that there are actually about 3.5 million fewer individuals who both have a job or are in search of one in contrast with pre-pandemic tendencies. Of the three.5 million, about 2 million encompass “extra” retirements — a rise in retirements excess of would have been anticipated based mostly on pre-existing tendencies. Roughly 400,000 different working-age individuals have died of COVID-19. And authorized immigration has fallen by about 1 million.

Powell is assuming 2-million of those misplaced laborers are on account of “extra retirements,” however the Brookings Institute says, at the least 2-million and sure 4-million are on account of “lengthy Covid.” Powell is shifting into the Covid camp, however not all the best way there but. The significance of this realization is that useless staff clearly won’t ever come again and people with longterm diseases, no matter how they obtained them, might not ever be capable to come again both.

So, Powell admitted this shortfall goes to endure, and he additionally stated the numbers may very well be a lot greater than the three.5-4-million, which he acknowledged right now is the conservative quantity for the shortfall. He additionally stated there are a lot of different paths by which you’ll moderately argue for a a lot greater shortfall within the taking part labor pool.

The impression of this labor disaster on GDP is important. You could have already seen the fact of what AP stories in your personal life, and I do know I’ve seen it at many institutions in my very own small farm-town group:

Apart from fueling inflation, a smaller workforce is inflicting different penalties. Some companies, notably retailers and eating places, have needed to reduce their hours of operation, dropping income and irritating prospects.

I’ve gone into quite a lot of native eating places the place I’ve been advised or learn over the previous 12 months that the menu was reduce on account of labor shortages and/or that open hours or days have been reduce with the intention to do what they might with the labor pool obtainable to them. Thus, AP right here confirms what I’ve been saying about how you can’t have a critical discount within the labor pressure and never have a discount in manufacturing, whether or not of providers or items. AP notes that improved effectivity may make up the distinction, however states that it’s not making up the distinction and that, in actual fact, effectivity, reminiscent of by way of automation, has gone down.

In fact a discount in manufacturing (GDP) IS a recession by definition. Usually, the one argument is over how lengthy GDP must be in decline earlier than we name it a “recession.” Nicely, that was till the argument lately shifted to say declining GDP merely must be incorrect as a result of “the labor market is powerful.”

The irrationality of this argument is that the scarcity of labor that’s inflicting manufacturing to drop proves we can’t be experiencing a recession (a drop in manufacturing). That’s, on the face of it, fully irrational, nevertheless it comes from entrenched pondering that believes the one explanation for a shortfall in labor is an financial system that’s booming alongside so strongly that demand for labor is exceeding labor provide on account of financial development operating forward of labor development.

This false impression is in every single place as a result of we’ve by no means seen a large drop-off like this in labor provide, so these writing about it don’t know the way to get their heads round it. They interpret it solely from the framework they’ve identified all their lives. Thus we see AP, even on this article, which lays out the explanations for the labor shortfall, repeat the very same mistake:

How the Fed will handle a strong labor market, with its impact on inflation, may show perilous.

It’s mind-boggling to me that they can’t see that labor is languishing at the same time as they describe the interior of causes of labor shortages. How is a labor market that’s quick, at the least, 4,000,000 staff — a lot of whom died and plenty of of whom now have longterm diseases — “strong?” Is dying strong? Is sickness strong? Is a SHORTFALL of 4-million staff “strong?”

They can not wrap their head round the truth that this can be a sick, even dying, labor market that Powell now needs to hit on the top to knock it down additional Thus, Powell repeatedly acknowledged right now the identical level that AP made forward of right now’s assembly:

Powell and different Fed officers have stated they hope their fee hikes will gradual shopper spending and job development. Companies would then take away a lot of their job openings, easing the demand for labor. With much less competitors for staff, wages may start to develop extra slowly.

Assume all of that by way of, and also you’ll notice the unbelievable peril concerned in pondering the explanation we can’t be in a recession after two quarters of receding GDP is that “the labor market is powerful.” Powell drove this level residence by making it clear the Fed needed to see unemployment rise earlier than it should cease growing rates of interest and easily go away them excessive for longer.

Right here is the way you suppose it by way of:

- Labor shortages are already inflicting manufacturing to fall as is clear even in small cities, reminiscent of the place I stay (and doubtless evident the place you reside).

- Consequently, there are thousands and thousands of jobs that haven’t been crammed that stay brazenly listed.

- Because of so many unfilled jobs, manufacturing fell from the beginning of the 12 months in precisely the way that will at all times previously have been referred to as a “recession.”

- As a result of they’ve so many roles they wish to fill, corporations are clinging to workers as they terminate jobs underneath Fed tightening by shifting workers to different positions that stay open.

- Which means, to get unemployment to rise, thousands and thousands of open jobs should be eradicated till there are only a few open positions for current labor to transition to. Then a few of terminated laborers will begin to go on unemployment, as a substitute of shifting laterally.

- Eliminating these openings is not going to impression manufacturing as a result of these jobs are simply empty placeholders producing nothing at current anyway.

- Nevertheless, it should take time for the Fed to clamp down on the financial system sufficient to squeeze so many further open jobs OUT to the place obtainable positions realign with obtainable staff, because the Fed says it needs, with the intention to cut back the pressures of wage inflation.

- Solely AFTER obtainable work matches right down to obtainable staff will additional financial squeezing remove jobs that end in a considerably rising unemployment fee.

- The Fed’s insurance policies have a lagged impact, so by the point it squeezes the financial system and, therefore, jobs down sufficient to lift unemployment considerably, the squeeze may have turn into fairly extreme.

- Lowering jobs and employed staff additional once we know effectivity can also be falling can solely imply a higher drop in manufacturing.

- Assured decrease manufacturing equals even worse shortages.

- Worse shortages put numerous upward stress on inflation, presumably making the entire inflation squeeze futile within the first place, relying on whether or not the Fed catches a break from all the opposite causes of shortages.

THAT is the good peril right here. The Fed may make shortages a lot worse at a time once we have already got too few staff to supply the products and providers we wish or want that we may hit Nice Despair ranges, particularly given the lengthy lag impact between Fed coverage after which between job losses and stock draw downs as shortages in stock in some companies end in shortages in stock in different companies that can’t get substances or elements. Decreased manufacturing, worsening shortages, may doubtless trigger a resurgence in inflation earlier than the Fed is even completed battling it. (And can the Fed even perceive the resurgence when it hits, or will it proceed to suppose meaning it must tighten down on employment even tougher?)

Misunderstanding the current labor market by pondering it’s robust is more likely to show to be the worst mistake the Fed has ever made. And THAT is the state of affairs I’m predicting for 2023. 2022 was all about shortages resulting in inflation resulting in Fed tightening, resulting in inventory and bond market crashes, all of which we noticed. 2023 turns into all in regards to the dire failure of the inflation restoration plan, leading to worse shortages and presumably a resurgent inflation downside that’s extra deeply entrenched, and an amplified recession as a result of the Fed doesn’t consider within the current recession solely on account of its false perception in a sturdy labor market, fairly than a sick and languishing labor market.

Three months in the past, the Fed’s policymakers estimated that the unemployment fee would rise to 4.4% subsequent 12 months, from 3.7% now. On Wednesday, the policymakers might forecast the next unemployment fee by the top of 2023. In that case, that will counsel that they foresee extra layoffs and sure a recession.

They did. Powell stated the brand new regular unemployment fee, given the labor scarcity, is likely to be 4.5%, and that it would take the next fee than that to get inflation down. Don’t ask me why that is smart as a result of it doesn’t in a time the place too few jobs are producing something. (Bear in mind, an unfilled job produces nothing.)

Terminal curiosity could also be terminal certainly

Extra essential than the employment fee Powell is in search of to drive wage-based inflation down is the terminal rate of interest he sees as essential to get there as a result of that may upset each market.

In his speech right now, Powell confirmed graphs of the Fed’s dot plots and acknowledged repeatedly — simply as AP reported the Fed has stated within the latest previous — that the Fed will not decrease rates of interest in any respect in 2023. No pivot! Whereas the Fed will make its interest-rate selections based mostly on the information obtainable to it at every assembly, Powell spelled out that he didn’t see any likelihood the Fed would decrease rates of interest in 2023, nor did every other Fed FOMC member.

Right here is how Fed members revised their collective dot-plot projections for rate of interest modifications greater up and increasing additional out at right now’s assembly from the place they have been on the final assembly: (Every blue dot is one Fed member’s projection at the moment assembly of the place the Fed’s highest base fee shall be in annually forward, whereas the pink line tracks the median degree in every column. The grey line and grey dots present what Fed members had projected at their September assembly.)

Powell admitted that ALL of of the Fed’s dot plots for terminal rates of interest had been too low all 12 months lengthy so that they have been revised upward at every subsequent assembly. Then he admitted the Fed needed to revise them upward once more at this assembly to a projected terminal fee round 5.25%. Furthermore, he stated he couldn’t say with any confidence the Fed was not underestimating this time by simply as a lot as all of the earlier instances.

In truth, it’s been longer than all 12 months lengthy that Fed members have needed to revise their projections upward. Right here is the place the Fed set its overnight-interest-rate projections for the 12 months 2023 at every Fed assembly (blue dots) in previous months. You may see how, at every assembly since March, 2021, the Fed has needed to elevate its projections (skinny pink line) greater for the very best curiosity degree it believes the Fed Funds Charge might want to attain in 2023: (Every column of dot clusters are the member’s projections for that month as to the place curiosity would peak in 2023.)

That’s numerous critical underestimation for 2023’s terminal rate of interest at every assembly alongside the best way, and Powell seemed a little bit embarrassed in saying right now all of them needed to revise upward once more at this assembly, and that he couldn’t promise they wouldn’t have to take action once more on the subsequent assembly.

Shares nonetheless have it incorrect, however they are going to get it proper if it kills them … and it’ll!

Blackrock, the Fed’s agent for the whole lot lately, warned the inventory market yesterday,

Don’t anticipate the Fed to avoid wasting the day – it’ll preserve rates of interest excessive even when a recession crushes shares subsequent 12 months

Don’t assume the Federal Reserve will bail out US inventory markets and bonds subsequent 12 months in the event that they get hammered by a extreme recession, a staff of BlackRock strategists has warned….

The Fed’s actions are more likely to gas a selloff in shares in 2023, as its tightening marketing campaign plunges the US right into a recession, the strategists at BlackRock’s Funding Institute stated….

“Main central banks will hike charges once more this week: getting inflation down means they should crush demand, making recession foretold….”

The Fed, the BoE and the ECB are so targeted on restoring value stability that they’re unlikely to help monetary markets and the financial system by slashing rates of interest, even when there’s a recession….

“Markets are incorrect to anticipate them to later come to the rescue….”

BlackRock’s bearishness comes despite the fact that inventory markets have rallied in latest weeks, buoyed by the thought the Fed would possibly “pivot” — or swap again its course — to start easing up on tightening within the second half of 2023….

Enterprise Insider

“By no means going to occur,” stated I. “No pivot!”

Powell pounded that time within the Q&A right now because the fool market refuses to simply accept it, saying he noticed no scenario through which that may occur and even be thought-about.

Boivin’s staff stated that they’d keep away from each equities and stuck earnings. They consider the markets’ latest overperformance relies on an assumption the Fed will return to its “previous playbook” of low rates of interest and free financial coverage, which it used after the 2008 monetary disaster and different earlier recessions….

“Not going to occur,” stated Powell … and Blackrock … and so they each must know as they work hand-in-hand proper on the core of all of this. Not going to occur.

One different factor that I stated was more likely to weigh on shares within the remaining quarter of 2022 was opposite to what Zero Hedge was saying. They stated buybacks would begin again up and carry the market greater, however I stated buybacks have been going to decrease as a result of company leaders don’t like to purchase again their shares in a recession. And, right now that was confirmed by Bloomberg:

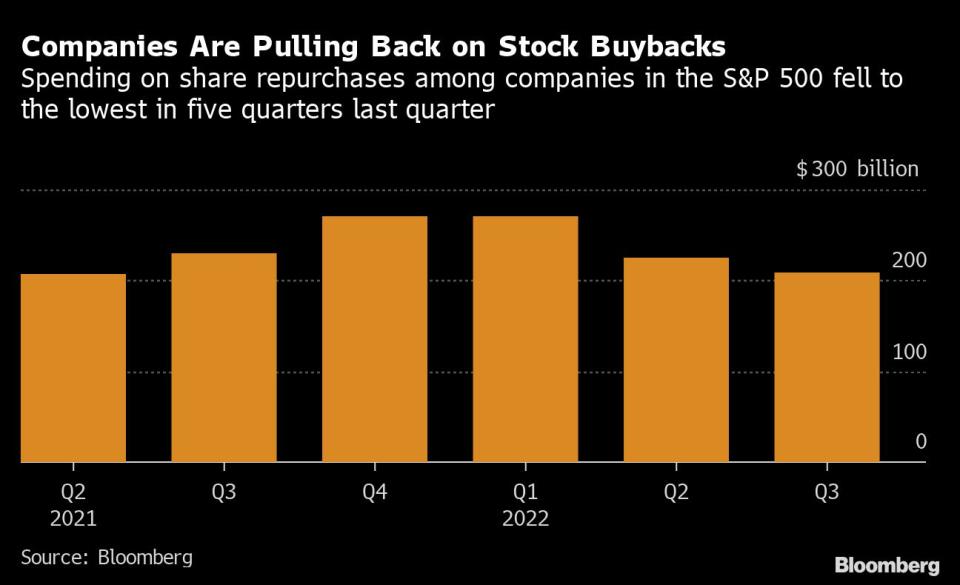

Company America Buys Again Fewer Shares as Recession Fears Rise

US corporations are slicing share buybacks to preserve money within the face of financial uncertainty, which threatens so as to add one other weight to the fairness market’s tried rebound.

S&P 500 Index companies purchased again simply over $200 billion of their very own shares through the third quarter, marking the slowest quarter for repurchases because the center of final 12 months and coming in roughly 25% beneath the degrees seen in late 2021 and early 2022, based on information compiled by Bloomberg….The strikes displays mounting nervousness that development will stall due to the Federal Reserve’s most aggressive interest-rate hikes because the Eighties….

Already, some corporations try to determine how greatest to slice up a shrinking money pie. Goldman Sachs Group Inc. Chief Government Officer David Solomon stated this month that administration groups have to organize for “bumpy instances forward,” and several other massive banks lately joined know-how giants like Meta and Amazon.com in decreasing their payrolls….

Buybacks are a far much less disruptive price to chop than headcount.

Bloomberg through Yahoo!

Bloomberg introduced the next graph of their information:

I’m certain you’ll see these stair steps go down one other notch in This fall now that Powell acknowledged right now the Fed has lastly gotten into “restrictive territory,” which is why it’s slowing the speed at which it raises curiosity with the intention to ease deeper into that restrictive territory with a little bit extra warning.

And, in fact, “restrictive territory” is the place you see the breakdowns begin to happen as emerged first in crypto markets lately, however the Fed is taking us deeper right into a recession Blackrock now says is a “foretold” conclusion and one which may simply turn into “extreme” as a result of there shall be no Fed help potential when the deeper crash hits on account of inflation.

“Foretold,” certainly. That is proper the place I stated many months in the past all of this is able to find yourself this 12 months. In truth, each step of the best way, was foretold right here; and I’m going to put that every one out tomorrow as a path of stepping stones the Fed apparently couldn’t resist and neither may the inventory market. Each step of the best way.

The complete Powell Presser

[ad_2]

Source link