stevanovicigor/iStock through Getty Photographs

Introduction

Once I’m mounted earnings securities like most well-liked shares, I need not have the very best yield, as that generally is a recipe for catastrophe as we, for example, noticed with Argo Blockchain (ARBKL) the place the worth of the newborn bond was crushed. For me, investing in most well-liked shares is at all times a threat/reward tradeoff.

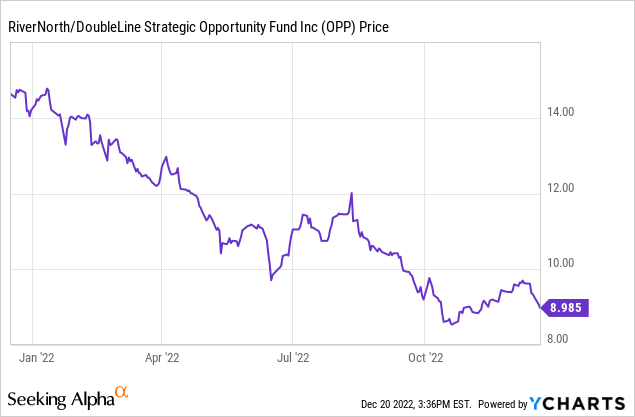

OPP’s efficiency in FY 2022 was okay, and preferreds needs to be wonderful

RiverNorth/DoubleLine Strategic Alternative Fund (hereafter simply ‘OPP’ to maintain it easy) is a closed-end fund specializing in creating worth by specializing in a tactical earnings technique and (as much as 35% of the managed belongings) and the opportunistic earnings technique (as much as 90% of the managed belongings).

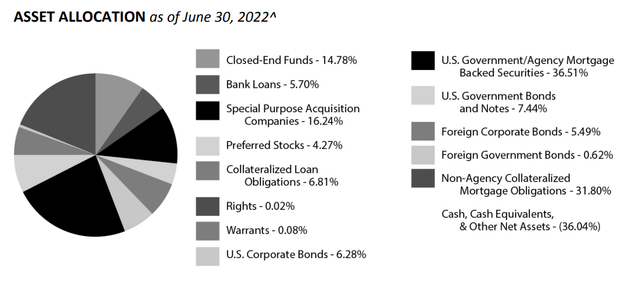

The portfolio primarily consists of bonds, closed-end funds and mortgage-backed securities. Once I final mentioned the CEF, shares and most well-liked shares made up lower than 16% of the belongings, however the portfolio didn’t comprise any widespread fairness anymore whereas the popular shares now nonetheless signify lower than 5% of the portfolio.

OPP Investor Relations

Nonetheless, there’s greater than meets the attention right here: OPP merely modified the outline from ‘widespread shares’ to ‘SPACs’ as that is what the widespread share portfolio consists of. The mixture of SPACs and most well-liked shares now exceeds 20%.

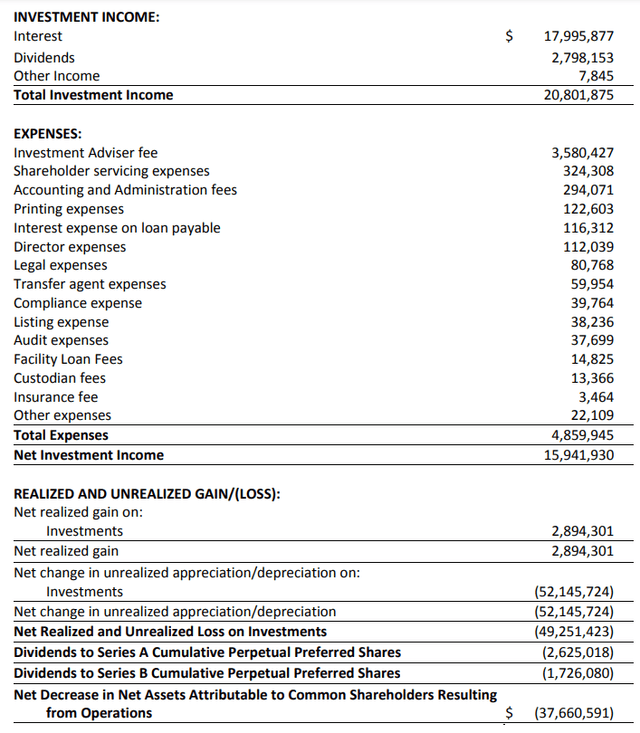

I am primarily taken with how a lot curiosity and dividend earnings the OPP portfolio is producing. Trying on the earnings assertion for FY 2022 (which led to June), the portfolio generated about $20.8M in curiosity and dividend earnings, with virtually 90% of that income coming from the bond and CLO portfolio.

OPP Investor Relations

We additionally see the full quantity of bills is simply $4.9M, leading to a internet funding earnings of $15.9M. As I’m primarily taken with the popular shares, I’ll ignore the $52M in unrealized depreciation on investments. Whereas that has a damaging influence on the NAV of the widespread items, it’s an irrelevant issue to determine how secure the popular shares are: finally the debt shall be repaid to OPP and mark-to-market variations will not make a distinction right here: both the borrower repays OPP, or it defaults. And, in fact, the decrease portfolio worth shall be mentioned after I have a look at the asset protection ratio.

We nonetheless want to take a look at the popular dividend funds. We see there was a $2.6M cost on the Sequence A most well-liked shares and $1.7M on the Sequence B. Consider the Sequence B had been solely issued in the course of the monetary yr and contemplating there are 2.4M most well-liked shares excellent, the normalized most well-liked dividends on the Sequence B shall be simply over $2.8M. On a mixed foundation, the popular dividends will price OPP about $5.5M per yr. With a internet funding earnings of just about $16M primarily based on the FY 2022 outcomes, the protection ratio of the popular dividends is sort of 300%. Not spectacularly excessive, however ok for me.

A more in-depth have a look at the 2 problems with most well-liked shares

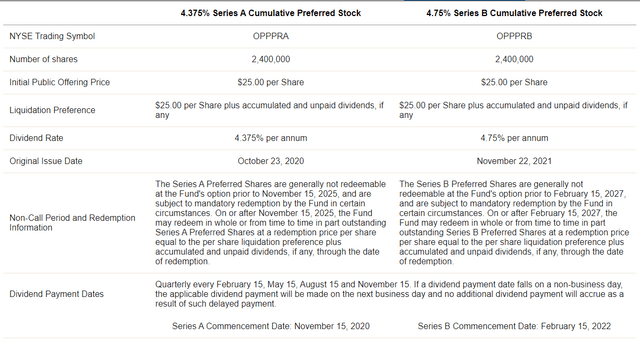

As defined in my earlier article, OPP now has two sequence of most well-liked shares excellent.

The Sequence A most well-liked shares are buying and selling with (OPP.PA) as ticker image and supply a cumulative dividend of $1.09375 per share per yr, which works out to a most well-liked dividend yield of 4.375% primarily based on the par worth of $25/share. These securities may be referred to as from November fifteenth, 2025 on. And to be clear, the popular dividend doesn’t have a reset perform: the $1.09375 stays unchanged till OPP decides to name the popular shares.

The Sequence B most well-liked shares are buying and selling with (OPP.PB) as ticker image and are additionally cumulative in nature. This sequence was issued in Q2 FY2022 (This fall calendar yr 2021) and OPP needed to supply the next most well-liked dividend to get the deal completed, and these most well-liked shares are paying a most well-liked dividend of $1.1875 per share and may be referred to as from February 15, 2027 on.

OPP Investor Relations

What’s fascinating is that because of the growing rates of interest, each most well-liked shares at the moment are buying and selling considerably under par. OPP.PA closed at $17.96 on Monday night time, whereas OPP.PB closed at $18.97, for a yield of respectively 6.09% and 6.26%. For sure that – as each sequence rank equally – I’m favoring the OPP.PB sequence now, given the upper yield and better probability the securities shall be referred to as (observe: these odds are nonetheless fairly slim at 4.75% is fairly low cost for perpetual fairness so though they’re extra prone to be referred to as, I do not suppose a name is probably going).

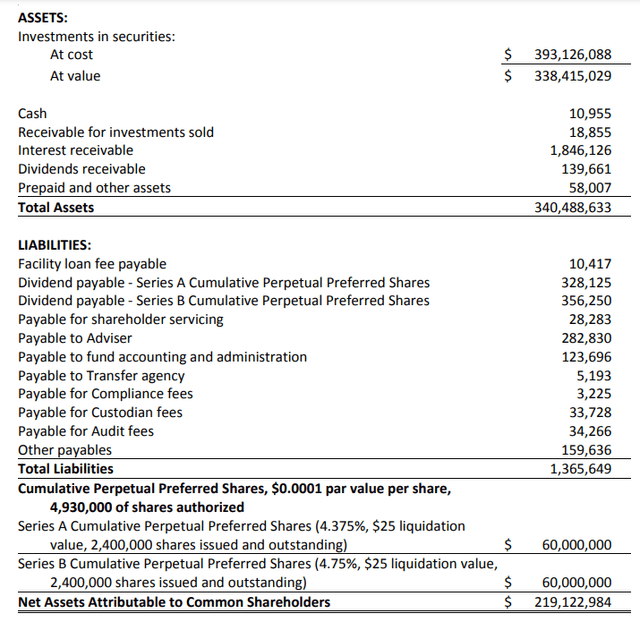

What I like most about all these investments is the shortage of debt on the steadiness sheet. As you’ll be able to see under, the full quantity of liabilities is lower than $1.4M, which is lower than half the full quantity of belongings.

OPP Investor Relations

This implies the popular shares are just about first in line to be paid out ought to one thing go improper. This additionally makes the asset protection ratio fascinating as the full quantity of belongings versus the $120M in most well-liked fairness got here in at 283%. So even when the worth of the portfolio drops by 50%, the popular shareholders can nonetheless be made entire.

The popular shares have a further fascinating function: if the asset protection stage drops under 200% (on this case, the full quantity of belongings must drop under $240M), OPP will both must concern new widespread items to shore up the belongings place, or shall be compelled to redeem the popular shares at par worth. And that is why I’m not too fearful in regards to the unrealized losses. It hits the widespread unitholders more durable, and the popular shareholders are protected by the 200% rule. And understand that subsequent to the top of the monetary yr, OPP raised about $34M in widespread fairness via a rights concern. This makes the popular shares safer.

Funding thesis

I at present nonetheless haven’t got a place in the popular shares of OPP, however I’m planning to go lengthy within the subsequent few weeks. On the present share costs, shopping for the B-series would make extra sense because the yield is larger.

Whereas the popular dividend yield of 6.1-6.25% is unquestionably not the very best yield on the road, it’s a ‘sleep nicely at night time’ kind of yield and the (normal) safety associated to the required 200% asset protection ratio provides a further layer of security.