[ad_1]

In 2014, Prayank Swaroop made a pitch to the storied enterprise agency Accel, the place he labored as an affiliate, about future marketplaces in India.

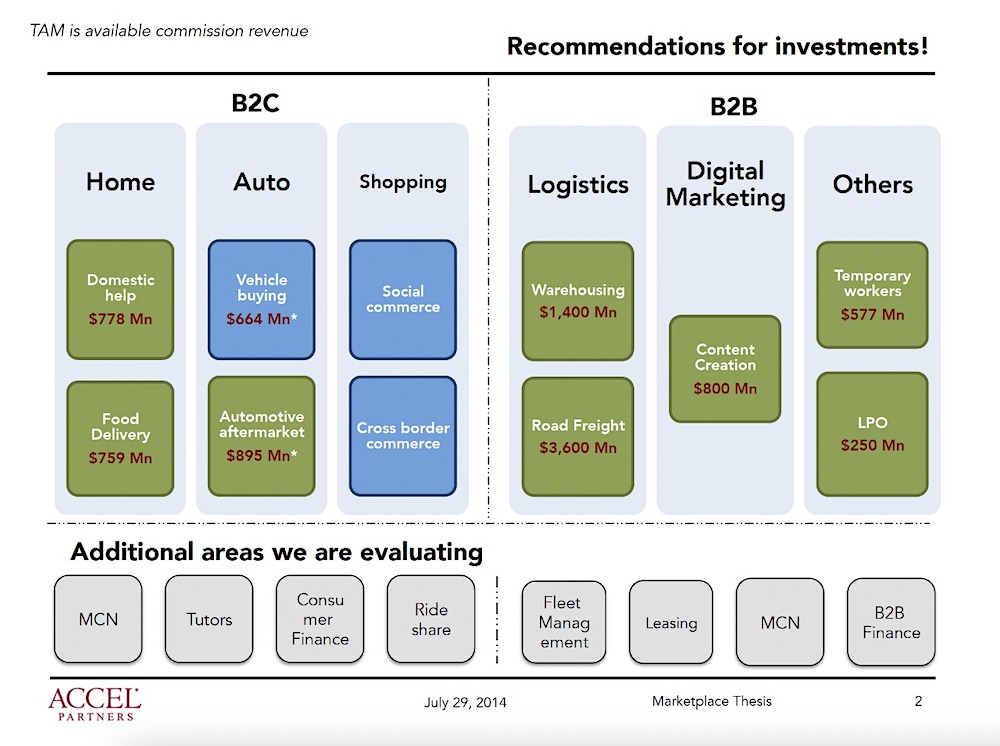

On the time, Flipkart and Snapdeal have been the one two e-commerce startups in India that had proven a semblance of scale. Swaroop made a case that as extra Indians come on-line, alternatives will emerge in meals supply, automotive aftermarket, warehousing, highway freight, and social commerce amongst many different market areas.

Swaroop, now a companion on the agency, turned out to be proper. City Firm, which operates within the home assist sector, is valued at over $2 billion; Zomato and Swiggy are delivering meals to thousands and thousands of shoppers every month; Spinny and Cars24 are promoting a whole bunch of hundreds of automobiles every quarter; social commerce startup DealShare is valued at over $2 billion and Meesho simply wanting $5 billion.

A whole lot of thousands and thousands of Indians have come on-line up to now decade and over 100 million are making on-line transactions and purchases every month. India, which has doubled its pool of unicorns to over 100 up to now two years, has attracted over $75 billion in investments from tech giants Google, Meta and Amazon and enterprise funds Sequoia, Tiger World, SoftBank, Alpha Wave, Lightspeed and Accel up to now 5 years.

Swaroop’s presentation from 2014. (Picture credit: Accel)

However because the native startup ecosystem closes considered one of its hardest years, it’s now looking at one other query that it has lengthy been in a position to brush off as benign: exits.

About half a dozen client tech Indian startups have gone public up to now 12 months and a half and all of them are performing poorly on the native inventory exchanges. Paytm is down 60% this 12 months, Zomato 58%, Nykaa 56%, Coverage Bazaar 52%, and Delhivery 38%.

That is regardless of the Indian shares outperforming the S&P 500 Index and China’s CSI 300 this 12 months. India’s Sensex — the native inventory benchmark — stays up 3.4% this 12 months, in comparison with fall of 19.75% in S&P 500 and 21% in China’s CSI 300.

Because the market modified its route this 12 months, many Indian startups together with MobiKwik and Snapdeal have delayed their itemizing plans. Oyo, which deliberate to listing in January subsequent 12 months, is unlikely to maneuver ahead with that plan, in accordance with two individuals accustomed to the matter.

Flipkart, valued at $37.6 billion and majority owned by Walmart, doesn’t plan to listing till no less than 2024, in accordance with an individual accustomed to the matter. Byju’s, India’s most respected startup, doesn’t plan to listing in 2023 and is as a substitute shifting forward with a plan to listing considered one of its subsidiaries, Aakash, subsequent 12 months, TechCrunch beforehand reported.

These seeking to push forward with their plans to go public will face one other impediment: A number of world public funds together with Invesco that ardently finance the pre-IPO rounds are retreating from the Indian market after getting hammered in China and different rising markets this 12 months, in accordance with individuals accustomed to the matter.

LPs have lengthy expressed issues about India not delivering exits and the early-attempts up to now two years from the business appear nothing to jot down residence about.

Indian enterprise funds have traditionally gotten most exits by the way in which of mergers and acquisitions. However even these exits are getting more durable to return by.

An analyst at one of many prime enterprise funds in India mentioned that for a very long time VCs who backed early-stage SaaS startups at sub-$25 million valuation stood an opportunity of constructing good exits. However as we have now seen in some circumstances in latest months, the exit itself values the startup at sub-$25 million, making it tough for SaaS traders to show a revenue.

II

On a latest night at a non-public gathering of some dozen business figures at a 5 star lodge in Bengaluru, many traders have been exchanging notes in regards to the offers they’d been evaluating. The companions complained that the standard of startups has dropped at the same time as the quantity of pitches has surged.

Two distinguished enterprise funds that run well-regarded accelerators or cohort programmes of early stage investments are struggling to seek out sufficient good candidates for his or her subsequent batches, individuals accustomed to the matter mentioned.

I’ll argue that it’s not simply that the standard of startups which can be rising has taken a success, it’s additionally traders’ urge for food and psychological fashions for what they assume may go sooner or later.

Take crypto, as an illustration. The overwhelming majority of Indian traders have been too late to make investments within the web3 house. (You’ll discover only a few Indian names within the cap tables of native exchanges CoinSwitch Kuber and CoinDCX and till not too long ago, blockchain scaling agency Polygon, as a distinguished VC at one of many world’s largest crypto VC funds not too long ago pointed to me.)

Now many companies in India that had employed various crypto analysts and associates final 12 months are retreating from the web3 market and have requested employees to deal with totally different sectors, in accordance with individuals accustomed to the matter.

Fintech is one other space of concern for traders. India’s central financial institution this 12 months pushed a sequence of stringent adjustments to how fintechs lend to debtors. The Reserve Financial institution of India can also be more and more scrutinizing who will get the license to function non-banking monetary corporations within the nation in strikes that has despatched a shockwave to traders.

Many enterprise traders are actually more and more chasing alternatives to again banks as a substitute. Accel and Quona not too long ago backed Shivalik Small Finance Financial institution. Many are deliberating an funding in SBM Financial institution India, one of many banks that has aggressively partnered with fintechs within the South Asian market, TechCrunch reported earlier this month.

An investor described the development as a “hedge” in opposition to fintech publicity.

Buyers’ enthusiasm within the edtech market has additionally cooled off after re-opening of colleges toppled the giants Byju’s, Unacademy and Vedantu.

Indian startups raised $24.7 billion this 12 months, down from $37 billion final 12 months, in accordance with market intelligence agency Tracxn. The funding crunch and the market dynamics prompted startups to let go of as many as 20,000 staff this 12 months.

Over a dozen traders I spoke with consider that the funding crunch gained’t go away till no less than Q3 of subsequent 12 months regardless of most traders chasing India sitting on document quantities of dry powder.

As we enter the brand new 12 months, some traders can be re-evaluating their convictions and lots of are satisfied that a number of down rounds for main startups are on the horizon. However many star unicorn founders are unwilling to take a haircut of their valuations, partly as a result of they consider that can drive some expertise away. PharmEasy, valued at $5.6 billion, was provided new capital at a decrease than $3 billion valuation this 12 months, in accordance with two individuals accustomed to the matter. (PharmEasy didn’t reply to a request for remark.)

“2022 began off strongly, and it appeared for some time that the Indian enterprise funding market can be topic to totally different gravitational forces than U.S. and China, which have been seeing dramatic declines, however this was to not be. The Indian market finally turned out to be topic to the identical macro headwinds because the U.S. and China enterprise market,” mentioned Sajith Pai, an investor at Blume Ventures.

Pai mentioned that growth-stage offers accounted for almost all of funding final 12 months and noticed wherever from a 40-50% drop this 12 months. “The decline was led primarily by development funds pausing investments as a result of the multiples in non-public markets have been wealthy in comparison with their public friends, and the weak unit economics of the expansion stage corporations.”

[ad_2]

Source link