[ad_1]

by Econ–Intel Crew

One of many instruments that the Federal Reserve has to handle the cash provide is the reserve requirement. Importantly, the reserve requirement can be a potent software to handle systemic threat of the banking system. The Federal Reserve has not too long ago abolished the reserve requirement. This text examines a number of doable impacts of this motion.

The reserve requirement is actually the share of deposits {that a} financial institution should maintain. As outlined by Investopedia:

Reserve necessities are the amount of money that banks should have, of their vaults or on the closest Federal Reserve financial institution, consistent with deposits made by their prospects. Set by the Fed’s board of governors, reserve necessities are one of many three fundamental instruments of financial coverage—the opposite two instruments are open market operations and the low cost fee.

www.investopedia.com/phrases/r/requiredreserves.asp

The reserve necessities are traditionally essential within the U.S. and applied in response to a banking disaster:

The fractional banking system got here into place as an answer to issues encountered throughout the Nice Despair when depositors made many withdrawals, resulting in financial institution runs.

corporatefinanceinstitute.com/assets/information/finance/fractional-banking/

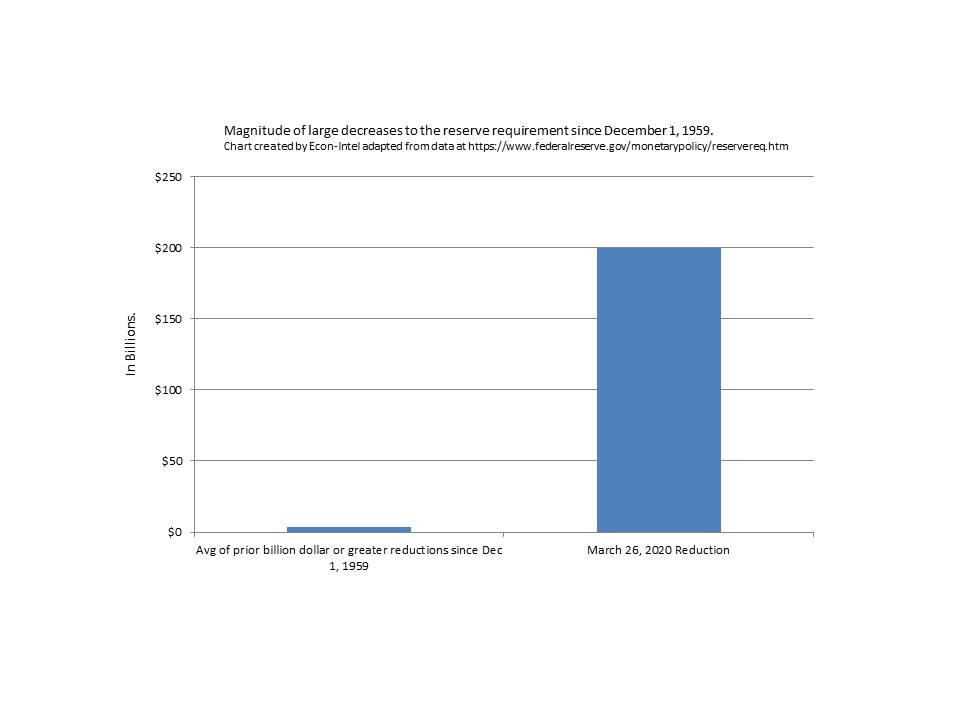

Since December 1, 1959, the Federal Reserve has adjusted the reserve necessities 105 instances previous to the latest time. At which level, the reserve requirement was abolished. The overwhelming majority (80.9%) of these changes, the reserve necessities affected the banking system by lower than $1.0 Billion. Of these instances that the Federal Reserve did change the reserve requirement, such that it affected the banking reserves by greater than $1.0 Billion, 6 elevated the reserve requirement and 14 decreased the reserve requirement. The chart under compares the dimensions of these prior giant decreases within the required banking reserves to the present change within the banking reserves.

As you’ll be able to see, this variation is unprecedented in scale. No different reductions in reserve necessities have come anyplace shut. The reserve requirement had by no means been abolished prior! The prior report for lowering the reserve requirement was roughly $8.9 billion on April 2, 1992. This time it was roughly $200 billion. This essentially modifications the whole U.S. banking system. It’s not a fractional reserve system. Now, there isn’t any authorized requirement for banks to keep up reserve balances.

The Fed’s Reasoning For Abolishing the Reserve Requirement:

On March 15, 2020, the Federal Reserve issued three press releases taking a collection of actions. One motion abolished the reserve requirement. Chosen textual content from every is cited under, then examined:

Federal Reserve points FOMC assertion:

The coronavirus outbreak has harmed communities and disrupted financial exercise in lots of nations, together with the US. World monetary circumstances have additionally been considerably affected….On a 12‑month foundation, general inflation and inflation for objects apart from meals and power are working under 2 %. Market-based measures of inflation compensation have declined; survey-based measures of longer-term inflation expectations are little modified.

The consequences of the coronavirus will weigh on financial exercise within the close to time period and pose dangers to the financial outlook. In gentle of those developments, the Committee determined to decrease the goal vary for the federal funds fee to 0 to 1/4 %. The Committee expects to keep up this goal vary till it’s assured that the financial system has weathered current occasions and is on monitor to realize its most employment and worth stability objectives. This motion will assist assist financial exercise, sturdy labor market circumstances, and inflation returning to the Committee’s symmetric 2 % goal.To assist the sleek functioning of markets for Treasury securities and company mortgage-backed securities which might be central to the move of credit score to households and companies, over coming months the Committee will enhance its holdings of Treasury securities by no less than $500 billion and its holdings of company mortgage-backed securities by no less than $200 billion. The Committee can even reinvest all principal funds from the Federal Reserve’s holdings of company debt and company mortgage-backed securities in company mortgage-backed securities. As well as, the Open Market Desk has not too long ago expanded its in a single day and time period repurchase settlement operations.

www.federalreserve.gov/newsevents/pressreleases/monetary20200315a.htm

Federal Reserve Actions to Assist the Circulate of Credit score to Households and Companies

The Federal Reserve encourages depository establishments to show to the low cost window to assist meet calls for for credit score from households and companies presently. In assist of this purpose, the Board at the moment introduced that it’ll decrease the first credit score fee by 150 foundation factors to 0.25 %, efficient March 16, 2020.

The Federal Reserve is encouraging banks to make use of their capital and liquidity buffers as they lend to households and companies who’re affected by the coronavirus.

For a few years, reserve necessities performed a central function within the implementation of financial coverage by making a steady demand for reserves. In January 2019, the FOMC introduced its intention to implement financial coverage in an ample reserves regime. Reserve necessities don’t play a major function on this working framework.

www.federalreserve.gov/newsevents/pressreleases/monetary20200315b.htm

Coordinated Central Financial institution Motion to Improve the Provision of U.S. Greenback Liquidity

The Financial institution of Canada, the Financial institution of England, the Financial institution of Japan, the European Central Financial institution, the Federal Reserve, and the Swiss Nationwide Financial institution are at the moment asserting a coordinated motion to boost the availability of liquidity by way of the standing U.S. greenback liquidity swap line preparations.The swap strains can be found standing amenities and function an essential liquidity backstop to ease strains in world funding markets, thereby serving to to mitigate the results of such strains on the availability of credit score to households and companies, each domestically and overseas.

www.federalreserve.gov/newsevents/pressreleases/monetary20200315c.htm

Summarized, the Federal Reserve acknowledged that as a result of coronavirus there was financial hurt. As a result of inflation was low, they had been going to supply financial stimulus by way of decrease rates of interest. In addition to treasury and company mortgage-backed securities purchases. Moreover, they introduced that they had been going to lend liberally by way of their repo facility. They additional went on to encourage banks to proceed to lend and abolished the reserve necessities. In addition to, coordinated with a number of different reserve banks to keep up liquidity within the greenback swap markets.

In the course of the panic and financial stresses surrounding the early portion of the coronavirus pandemic, these actions are defendable. Now, circumstances have modified and it’s obvious that the large financial stimulus has led to an inflationary atmosphere. Apparently, the Federal Reserve both misjudged the optimum amount of financial easing or waited too lengthy earlier than lowering financial stimulus.

Abolishing Reserve Necessities in an Period of Tightening Makes no Sense:

Now, the Federal Reserve has reversed course on rates of interest and is now aggressively elevating charges. In addition to promoting off treasuries and mortgage-backed securities relatively than buying them. The logic of eradicating the reserve requirement briefly to stimulate the financial system was defensible throughout the pandemic response. Nonetheless, leaving the reserve requirement at 0% and experimenting with working with none reserves is a weird and dangerous experiment. Moreover, it’s going to restrict the Fed’s capability to tighten when that’s their purpose.

Reserves are vital to the steadiness of the banking system. For depositors to have the ability to withdraw cash from their financial institution, reserves have to be obtainable. Each logically and traditionally, when some depositors are unable to get their cash out of their financial institution, a panic is probably going. As an elevated variety of folks concern the identical occurring to them and go to withdraw cash from their financial institution. This will create a financial institution run. When banks that had adequate reserves for day-to-day actions are unable to redeem deposits for his or her shoppers throughout the panic. The panic and financial chaos surrounding the following money crunch can unfold and create economically troublesome instances.

Of the instruments that the Federal Reserve has, the reserve requirement is the one that the majority immediately impacts financial institution liquidity. It additionally applies most on to these banks with marginal liquidity with out instantly immediately affecting the extra liquid banks. In different phrases, the reserve requirement is usually a extra focused software than the blunter rate of interest software.

Instance Danger Situation of Abolished Reserve Requirement:

Present reserve necessities are 0%, as they’re now. The least liquid financial institution, as decided by its reserves, is 1.2%. For example, it holds $12,000,000 of reserves in money or on the nearest Federal Reserve department on $1,000,0000,000 of deposits. All different banks are holding 3.0% or extra in reserves on this instance.

If the Federal Reserve had been involved about future financial circumstances, it might select to extend the reserve requirement from 0% to 1%. This variation would be certain that the least liquid financial institution didn’t mortgage out the entire remaining $12,000,000 of reserves.

This might lower the chance of the least liquid financial institution failing because of liquidity points. In addition to enhance certainty that the financial institution has the reserves obtainable when depositors want to withdraw cash. If the Federal Reserve is unsure that the rise from 0% to 1% is adequate to buffer towards these dangers sooner or later, the Fed can even supply ahead steering on the reserve requirement. It will encourage banks to retain more money in preparation for subsequent extra will increase within the reserve requirement. This feature would permit banks to arrange upfront for added will increase within the reserve requirement. This motion will assist guarantee ample liquidity for the banking system to proceed working easily.

The Fed is responding to excessive inflation by elevating rates of interest and lowering its stability sheet by promoting bonds. Each of those actions tighten the cash provide to dampen demand for items and companies. This decreased demand will hopefully dampen inflation and convey it again right down to a extra cheap degree. Why then has the Federal Reserve left in place an unprecedented coverage of utmost loosening by permitting the banks to maintain actually no reserves in any respect? When the Federal Reserve is tightening the cash provide anyway, there isn’t any price to tightening by rising the reserve requirement. This might obtain the purpose of tightening to struggle inflation and would enhance the liquidity of the least liquid banks. Due to this fact, lowering threat to the banking system as a complete.

Three key causes to extend the reserve requirement at once:

- First, when the Federal Reserve is tightening anyway, there isn’t any unfavourable impact of slowing the financial system from having a portion of this tightening come from the rise in reserve necessities. However elevating the reserve requirement at a time when the Fed is loosening financial coverage would counteract their different actions to stimulate the financial system.

- Second, all through the banking system as a complete, there are vital reserves. As of the top of twond quarter 2022, the banking system as a complete, has money to cowl roughly 17.9% of all buyer deposits (See: banking business information for extra particulars). As a result of comparatively excessive money balances within the banking system presently, it must be comparatively straightforward for the much less liquid banks to restructure their stability sheets to realize greater reserve balances. Ready longer till general systemic liquidity decreases would jeopardize the power of the much less liquid banks to extend their very own reserves and liquidity.

- Third, starting the method of accelerating reserve necessities now permits extra time for banks to adapt. A speedy change in reserve necessities could be tougher for banks to answer and would enhance the possibilities of unfavourable penalties throughout the transition.

Conclusion:

The Federal Reserve has a software that each will increase systemic banking security and tightens financial coverage. However, they’ve deserted it. Additional delays in re-establishing an inexpensive reserve requirement jeopardizes the longer term stability of the US banking system. The present coverage of tightening provides a uncommon alternative. The Fed might re-implement reserve necessities to tighten the cash provide and enhance the steadiness of the banking system. The Federal Reserve Abolishing the reserve requirement elevates many potential dangers. Delaying a return to using reserve necessities presently, when the Federal Reserve is tightening coverage, is downright unexplainable.

[ad_2]

Source link