On March twenty second, The Fed determined to proceed to lift charges 1 / 4 of some extent whereas altering steering from “ongoing will increase” to “some further coverage firming could also be applicable,” and reiterated their information dependency. Chairman Powell within the press convention additionally reiterated the security of the banking system.

I imagine we’re more likely to see another fee hike earlier than the Fed pauses and permits the lags in financial coverage, and the tightening of credit score introduced on by this stress within the banking system, to proceed to tighten monetary circumstances to maneuver inflation towards the two% goal with the liberty to lift charges additional if it sees any acceleration in inflationary strain. Time will inform if this shall be sufficient to perform the Fed’s purpose or if additional fee hikes shall be needed. The Financial institution of England additionally raised charges 0.25% as did the Norges Financial institution in Sweden citing the dangers of inflation, so inflation continues to be a world concern.

Present expectations available in the market are for vital fee cuts towards the top of this 12 months. Nonetheless, Blackrock has acknowledged they don’t see fee cuts this 12 months.

“We don’t see fee cuts this 12 months – that’s the previous playbook when central banks would rush to rescue the economic system as recession hit,” the strategists mentioned. “We see a brand new, extra nuanced section of curbing inflation forward: much less preventing however nonetheless no fee cuts.”

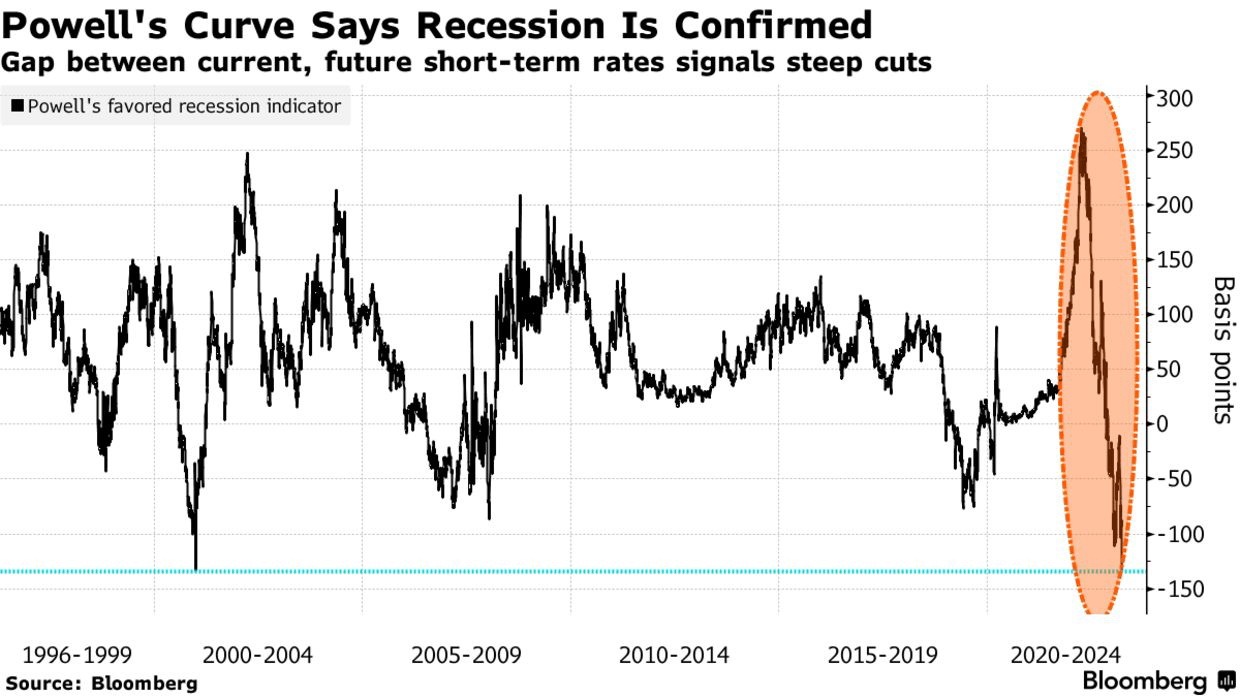

Chairman Powell has unequivocally acknowledged fee cuts should not within the playing cards primarily based on the present information. Nonetheless, the Chairman’s personal most popular gauge of recession danger, is flashing purple.

“Frankly, there’s good analysis by employees within the Federal Reserve system that actually says to have a look at the brief — the primary 18 months — of the yield curve. That’s actually what has 100% of the explanatory energy of the yield curve. It is smart. As a result of if it’s inverted, meaning the Fed’s going to chop, which implies the economic system is weak.” — Fed Chair Powell on March 21, 2022

Bloomberg

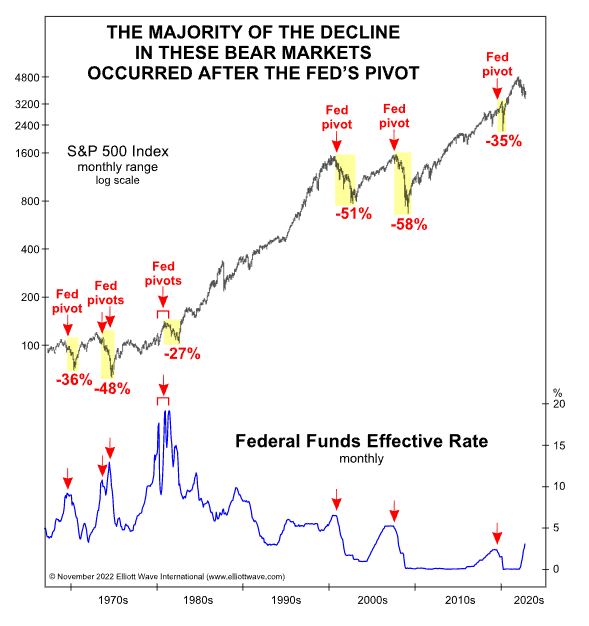

Shares have been rallying after the Fed’s assembly on the thought {that a} Fed pivot is across the nook. Nonetheless, historical past tells us that almost all of the decline in bear markets comes AFTER the Fed pivots. Traders needs to be cautious earlier than shopping for into this rally, as shares stay extremely overvalued at present ranges, primarily based on a variety of valuation strategies, and have solely turn out to be extra so, because the Nasdaq has rallied in current weeks.

“… for the reason that Nineteen Sixties, the Fed has repeatedly hiked rates of interest to fight inflation. Notably, the inventory market continues to carry out when the Fed is lifting rates of interest. Every time, that improve within the inventory market, because the Fed was mountaineering charges, led traders to imagine that this time was totally different. Nonetheless, the Fed paused or pivoted from financial lodging as an financial recession or disaster was realized.”

-Lance Roberts

@TommyThornton

New Dangers From Rising Charges Materialize

Trying on the zeitgeist available in the market right this moment, traders appear to imagine all is obvious. The solar is out, spring is right here, and so is a brand new bull market. I’ve seen quite a lot of items on SA, and elsewhere in monetary media, calling for a brand new bull market. I respectfully demur, there isn’t a proof at this level that each one is obvious. In truth, the stress within the banking system could have come down from a fever pitch of financial institution runs, and fixed worries about who will fail subsequent, however the general danger available in the market could be very actual. The Wall Avenue Journal lately posted an article, The place Monetary Danger Lies in 12 Charts that demonstrates we’re simply starting to really feel the ache from the fast rise in rates of interest.

Dangers Constructing in CRE

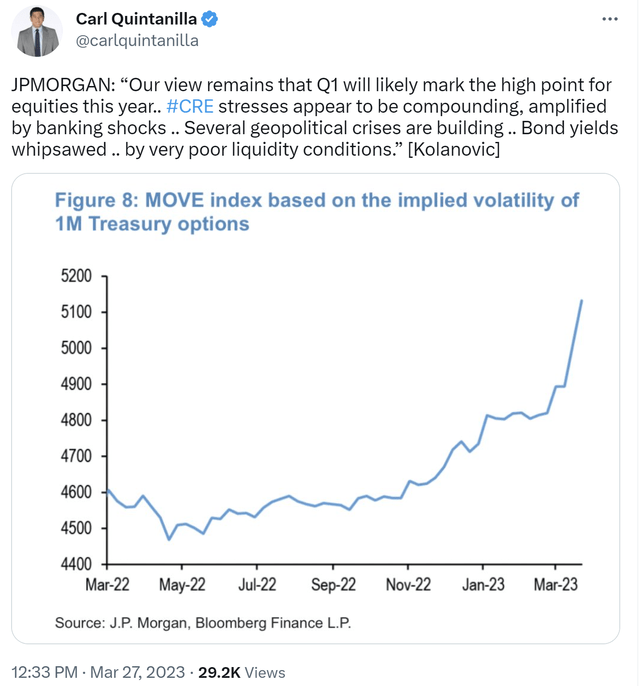

The dangers in business actual property are additionally rising, as Dubravko Lakos-Bujas and the workforce at JPMorgan acknowledged.

“Although workplace CRE has been in a multiyear decline, pressures at the moment are intensifying from increased charges, hedging prices, declining property costs, enterprise cycle slowdown, and secular demand disruption (e.g., workplace emptiness of 13% and whole availability of 16% are at [global financial crisis] stage)…The banking shocks ought to solely amplify these pressures and will complicate the debt roll on condition that sizeable CMBS workplace mortgage maturities are coming due in 2023-2024…Whereas choices stay for debtors/lenders to hunt modifications (e.g., lengthen mortgage phrases to keep away from flood of distressed gross sales), a string of current defaults needs to be interpreted extra as a gap salvo versus a one-off occasion…”

Marko Kolanovic, additionally of JPMorgan put out a word, reiterating his bearish stance on equities.

@carlquintanilla

I proceed to be bearish over the following 12 months for danger property, however within the brief run, I may see the S&P 500 transferring up in the direction of 4,200 accompanied by a transfer increased in yield, decrease in worth for 30-year Treasuries. For my part, traders ought to take any transfer up within the S&P 500 to cut back danger property, together with excessive yield credit score publicity, and add to their holdings of U.S. Treasury securities as charges backup, after a historic transfer.

Deflationary Danger Rising

“In different phrases, given that cash provide development is now even decrease there may be now definitely a danger of DEFLATION within the U.S. sooner or later in 2024-2025.” -Lars Christensen, The Market Monetarist

Kelly Evans at CNBC put out a really insightful word drawing on the work of Lars Christensen, discussing the notion of deflation being the true danger right here. The warning is that the Fed has achieved an excessive amount of already and is at risk of lacking their goal to the draw back, stating:

the market is warning that the Fed is about to overlook its inflation target–to the draw back. The breakevens now indicate that inflation will common a mere 2.1% over the following 5 years, barely above the Fed’s 2% goal. The collection reached as excessive as 3.5% final March, when the Fed had solely simply begun to hike, however has steadily declined since. Even the upward creep we noticed over the previous few months has now been decidedly reversed.

Equally, customers’ expectations of inflation have saved dropping. Their year-ahead inflation expectations are rapidly reversing the Covid surge, falling to three.8% on Friday (they’re all the time a bit of increased than the precise inflation fee). 5-to-ten 12 months expectations dropped as nicely, to 2.8%. Final Friday we additionally noticed one other decline within the index of main indicators–for the eleventh month in a row–and the 6.5% year-on-year drop we’re in has by no means occurred exterior of recessions.

I extremely suggest all traders learn this, because the argument is an alternative choice to most of the arguments we’re listening to right this moment about how the Fed wants to stay targeted on inflation. Personally, I imagine each might be true. Deflation is the longer-term danger; I’ve written about this for a while. Nonetheless, the near-term dangers of inflation are additionally actual. The Fed must be positive inflation is transferring in the direction of goal earlier than it may well make any significant change in financial coverage. At present, inflationary expectations are declining, giving proof to the rivalry that inflation was the truth is transitory. Time will inform if the pattern continues, or if additional tightening is important.

Apollo

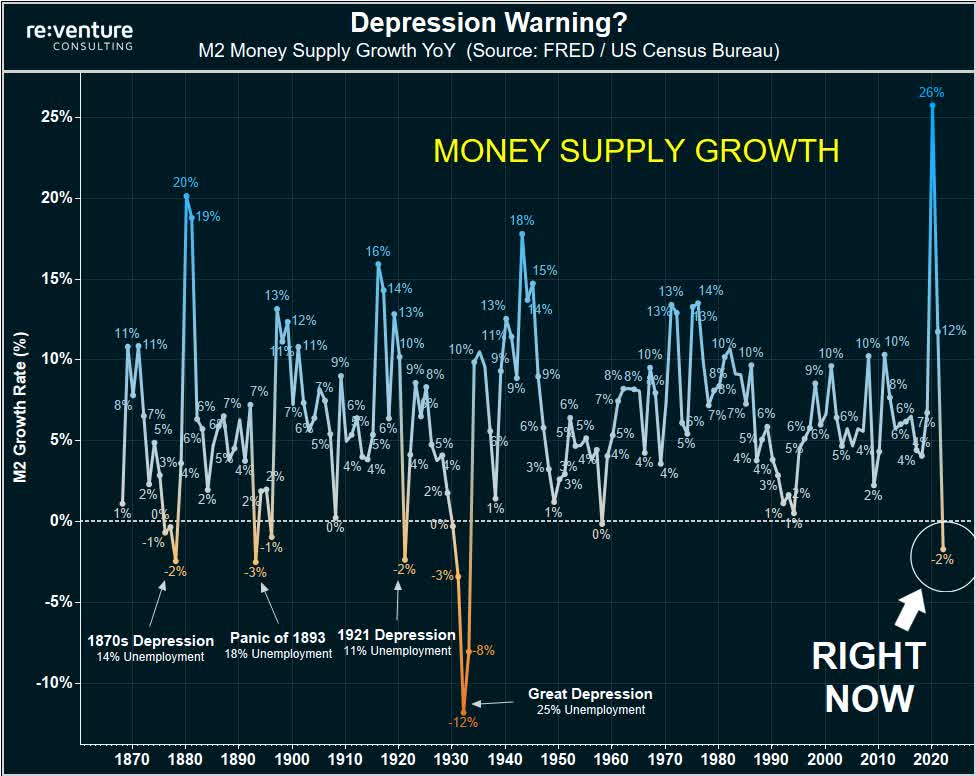

The Ominous Warning within the Collapse of M2

For the fifth time in 153-years an financial indicator is flashing purple. I’m talking in regards to the drastic fall within the M2 cash provide. We all know from Fishers Equation of Alternate, that GDP=M*V, with M being the cash provide and V being velocity on M2. The drastic fall in M2 is a harbinger of issues to come back, specifically, falling GDP. However what is admittedly noteworthy is the dramatic fall in M2 from a historic context. The final time the Fed was elevating charges and M2 fell at this fee was throughout the melancholy of 1921. What adopted was double-digit unemployment and a steep financial contraction.

If historical past is any information, we’re a severe drawdown on the horizon. I imagine the waterfall stage of this bear market may see the S&P 500 fall to my goal of three,000-3,200, representing a 20-25% decline from present ranges, which when added to the earlier 12 months’s decline of 25% needs to be a boring 50% correction, which has been sorely wanted to revive the fairness danger premium.

I’ve written at size about the truth that this market is unlikely to see a single cathartic transfer decrease that alerts the top of the bear. Bear markets so usually transfer in waves. In truth, within the 2000-2002 bear market, there have been 16 double digit bear market rallies on the best way to new lows. We’re more likely to proceed to grind decrease all through 2023, whilst some see the Fed reducing charges within the fourth quarter. I don’t imagine we’re more likely to see fee cuts this 12 months, because of the Fed’s ongoing conflict with inflation.

JPMorgan Chase & Co.

JPMorgan’s CEO Jaimie Dimon, in his annual letter to shareholders commented on the economic system, and the potential outcomes from the inverted yield curve, and the immense stress we’ve got seen on the banking system.

Immediately’s inverted yield curve implies that we’re going right into a recession. As somebody as soon as mentioned, an inverted yield curve like that is “eight for eight” in predicting a recession within the subsequent 12 months. Nonetheless, it is probably not true this time due to the large impact of QT. As beforehand acknowledged, longer-term charges should not essentially managed by central banks, and it’s potential that the inversion we see right this moment continues to be pushed by prior QE and never the dramatic change in provide and demand that’s going to happen sooner or later… Larger rates of interest will clearly have an essential affect, not only for banks however for a few of those that borrow on a floating fee or those that should refinance in a better fee setting. If this tide goes out, it is best to assume that it’s going to expose further weaknesses within the economic system.”

It’s clear that whereas Mr. Dimon goes on to debate the alternatives for his firm, he additionally sees storms on the horizon. Bears have lengthy been perplexed as to how markets can proceed on a seemingly irrational path increased, even because the world round them continues to expertise vital earthquakes.

He offers rise to the concept that the Fed could have modified the construction of the macroeconomy of their response perform and the instruments employed to take care of crises. That is an attention-grabbing level that deserves additional exploration. The yield curve has been inverted for a while nonetheless, no recession has materialized. Are we flawed to be bearish, and is the impact of the Feds extraordinary financial coverage altering macroeconomics as we all know it? I’ll discover this in my subsequent piece, Are we Fallacious to be Bearish?

Conclusion

Any decline in yields shouldn’t be an indication that the FED is about to carry a punch bowl… however moderately an indication that recession likelihood has elevated… we imagine shares are set to weaken for the rest of the 12 months and one needs to be [underweight] from right here.” -Marko Kolanovic, JP Morgan

Deflation continues to be the true danger to the economic system long run. The query stays whether or not the Fed has achieved sufficient to take care of the near-term inflationary pressures or whether or not additional lodging is important. The Fed has achieved a poor job of forecasting and is more likely to tighten too far resulting in undesirable outcomes.

Bob Michele, Chief Funding Officer, and Head of World Fastened Revenue at JPMorgan acknowledged in his March commentary:

“Recession stays our base case and was saved unchanged at 60%. The central banks are in all-out inflation-fighting mode. Charges will go as excessive as needed and finally set off the painful adjustment all of us hoped can be averted… After a 12 months of torture from unfavorable convexity (notably, period extension), the absence of financial institution shopping for and the removing of Fed help, the market appears washed out. A authorities bond with yield needs to be the perfect funding headed right into a contraction.” (Emphasis mine)

It’s clear in instances of market stress; the unfavorable correlation of US Authorities bonds has been a worthwhile selection for traders. As I acknowledged in my final piece, we’re more and more headed towards a Minsky Second. This isn’t the time for traders to tackle further fairness danger. As a substitute, I favor authorities bonds throughout the curve, significantly lengthy period. I imagine traders ought to use any backup in charges so as to add to those positions.

There’ll come a time once more for traders to deploy capital in the direction of danger property, however the present danger/reward is skewed to the draw back, and with excessive yields in top quality paper, it appears a present to lock in these charges. I see your entire curve flattening and echo the prediction of JPMorgan’s Bob Michele who mentioned your entire curve goes down to three% minimal. The bond bull market continues.