[ad_1]

Europeans have been able to have fun in 1815. Napoleon was defeated and in exile. The continent was lastly at peace after 12 years of the Napoleonic Wars.

The British have been particularly excited. Their second warfare with America, the Battle of 1812, was additionally over. The textile business was booming.

However by the tip of the 12 months, each Europe and the U.Okay. have been in an financial despair.

This downturn isn’t a shock to financial historians. Financial troubles typically comply with wars.

Not less than for the reason that time of Napoleon, wars are large effort. Troops within the discipline want weapons, ammunition, uniforms, meals and different provides. These calls for typically result in financial booms in nations at warfare.

Militaries demobilize when wars finish. Troops are discharged and returned house. This will increase the dimensions of the civilian workforce at precisely the flawed time.

With the warfare over, orders for brand new provides are canceled. This slows the financial system. On the similar time, returning troops want new garments and objects to restart their lives. There at the moment are new shoppers competing for the restricted provide of products {that a} contracting financial system is producing … and the restricted variety of jobs.

This sample occurred a century later, on the finish of World Battle I. Recessions and inflation additionally adopted World Battle II, the Korean Battle and the Vietnam Battle.

You might not notice it, however america is in a post-war financial system proper now. And as we proceed to unwind, it threatens one other financial downturn that may solely be obvious in hindsight.

Wartime Spending for COVID-19

The coronavirus unleashed a pandemic in 2020. Governments responded as in the event that they have been at warfare.

Sources have been marshaled in opposition to the enemy. Spending soared as governments purchased provides. As a share of gross home product, COVID spending rivaled the efforts of worldwide wars.

Within the previous days, policymakers understood that warfare demobilization would disrupt the financial system. They took steps to keep away from that disruption.

As World Battle II was drawing to an finish, the U.S. developed the GI Invoice. This supplied instructional alternatives to returning veterans. That helped preserve the workforce from swelling.

VA loans have been additionally supplied to assist veterans purchase houses. This led to a building growth, creating jobs in homebuilding to soak up employees now not wanted in factories. Wartime financial insurance policies have been steadily lifted to ease the transition to the peacetime financial system.

However policymakers haven’t been following this sort of strategy previously few years. Because the COVID-19 disaster eased, they resisted change. They stored spending at wartime ranges. The Federal Reserve stored rates of interest at 5,000-year lows.

All this doesn’t come with out penalties…

Bracing for the Financial Downturn

At this time, we’re paying the worth for these insurance policies. Inflation is easing however stays excessive. Companies are struggling to revenue as prices rise and value hikes cut back gross sales.

Shoppers are additionally struggling. Wages aren’t maintaining with inflation. Shoppers are turning to debt to maintain up with bills. Concurrently, firms are downsizing their workforces because the pandemic restrictions have eased and extra employees can be found.

As client stress rises, delinquent loans will rise. That provides strain to the banking system that’s already below stress as a result of rates of interest are now not at 5,000-year lows.

Historical past may also help us perceive the magnitude of the issues we face. We don’t understand how lengthy the financial ache will final, however the sample signifies it’ll actually make an affect.

That post-Napoleonic despair lasted for years. It contributed to the panic of 1819 within the U.S. The nation’s financial system wanted two years to get well from that.

The recession after the Civil Battle lasted 32 months. Two recessions adopted World Battle I. The financial system lastly recovered three years after the tip of that warfare.

World Battle II led to an eight-month recession. The Korean Battle recession lasted 10 months. A 16-month recession adopted the Vietnam Battle.

The post-covid recession hasn’t formally began but. The consequences will definitely final into 2024. Now’s the time to organize for a downturn that’s more and more inevitable.

At a minimal, that you must outline the place you’ll promote. Many buyers noticed the financial system slowing in 2019 and determined there was nothing to fret about. Some obtained fortunate when shares shortly recovered from the pandemic bear market.

However there’s no motive to count on a speedy restoration this time and hoping for one received’t cut back bear market losses.

There is no such thing as a “one measurement suits all” plan for the upcoming bear market. It would rely on the technique you utilize and your private degree of danger tolerance.

You may wish to enhance money holdings … or add gold as a hedge. You might wish to promote primarily based on the worst-case losses you’re prepared to bear, or use a trailing-stop technique to exit positions with good points.

The essential factor is to plan now. As a result of all of the indicators I’m seeing level to a distinguished downturn nonetheless to come back.

Regards, Michael CarrEditor, One Commerce

Michael CarrEditor, One Commerce

In finance, typically the actual kernels of fact are in between the information.

Think about the quick meals chain Wendy’s. On the primary quarter earnings name, CEO Todd Penegor made the offhand remark that Wendy’s was “seeing good progress with the over $75,000 [in income] cohort.”

Now, I feel it’s protected to imagine that the Wendy’s menu hasn’t upgraded to wagyu beef. It’s the identical mediocre hamburger it’s at all times been.

In the event that they’re seeing extra gross sales from professionals incomes $75,000 or extra per 12 months, it’s as a result of that demographic is slicing again on bills.

We noticed the same story popping out of Walmart. Earlier this 12 months, the low-cost retailer commented that about half of its enchancment in market share was resulting from higher-income People slumming it.

Okay, so possibly he didn’t truly use the phrases “slumming it,” however you get the thought.

Once you see higher-income customers buying and selling down, that’s not usually an indication of a wholesome financial system. Inflation has taken a chunk out of buying energy, and it’s exhibiting.

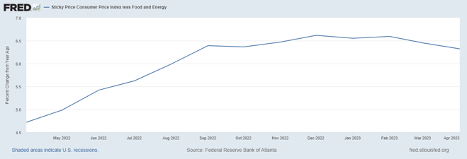

There could also be a minimum of slightly aid on that entrance. April Client Value Index inflation grew at an annualized fee of 4.9% — its lowest enhance in two years.

“Sticky” inflation, or inflation in items and providers that are typically sluggish to lift costs, has been slower to retreat. However it’s trending ever so barely decrease. We’ll name {that a} win.

The inflation fee continues to be a good distance from the Federal Reserve’s goal of two% although. And that’s not one thing that Fed fee hikes alone can repair.

You get inflation from two main sources:

- There’s an excessive amount of demand, which is outstripping the financial system’s skill to produce.

- There’s a disruption to produce.

In the mean time, now we have slightly of each.

Nevertheless, the Fed’s fee hikes (and inflation itself!) have completed a good job of dampening demand — a minimum of for issues that typically require credit score.

And if we get a recession within the coming quarters (which I do count on will come), that may additional assist to cut back demand.

It’s the “provide” half that takes longer to resolve.

As a result of we’re not simply speaking about backed-up provide chains, which have largely been mounted at this level. We’re additionally speaking a couple of reversal of 40 years of globalization.

China exported deflation to the remainder of the world by way of its low cost labor and manufacturing. The reversal of that pattern (a time period we name “deglobalization”) is a significant driver of inflation.

The excellent news is: The investments being made in the present day in automation and synthetic intelligence are poised to spice up productiveness to ranges final seen within the Nineties … and in accordance with the projected information, a lot larger.

If you wish to make the most of this tech pattern that’s taken the world by storm, take a look at Ian King’s newest analysis in microchip shares.

That is the know-how that’s driving AI and automation software program. And in Ian’s free webinar, he explains how chip manufacturing itself is projected to succeed in a $1 trillion worth by 2030. Simply go right here for all the main points.

Regards,

Charles SizemoreChief Editor, The Banyan Edge

Charles SizemoreChief Editor, The Banyan Edge

[ad_2]

Source link