")

[ad_1]

Final Thursday’s headlines informed us that the world’s fourth largest economic system — Germany — had slipped into recession. German shoppers have been tapped out after struggling by way of months of excessive inflation.

The most recent information reveals the nation’s inflation dropping to 7.2%. Meals and electrical energy costs are each greater than 15% larger than they have been a yr in the past. That’s a pointy reversal for a rustic the place inflation averaged about 1% for greater than 20 years earlier than beginning to speed up in January 2021.

Though the explanations for the recession have been clear, trying again, college students of historical past will surprise about how that interval was outlined. Germany is in recession as a result of the nation suffered two consecutive quarters of declines in GDP.

Right here within the U.S., the query of what makes a recession wasn’t agreed on so clearly. In truth, the controversy over the precise definition of a recession occurred lower than a yr in the past.

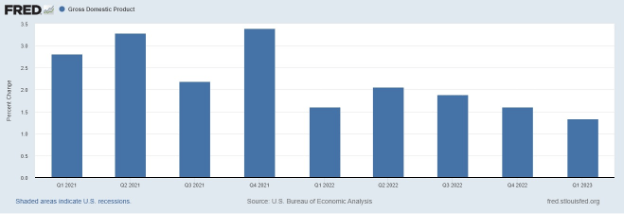

In July 2022, NPR requested if we have been in a recession after the second consecutive quarter of financial contraction. Preliminary estimates confirmed GDP contracting 0.9% within the second quarter of 2022 and 1.6% within the first quarter.

White Home officers, together with President Biden, argued that we weren’t in a recession. They pointed to different financial indicators that confirmed the economic system was persevering with to develop.

Nearly a yr later, we all know these officers have been proper. Two down quarters wasn’t proof of a recession.

Supply: Federal Reserve

What we discovered final yr from the controversy was that recessions are outlined by a number of indicators, as outlined beneath:

- Actual private revenue much less transfers.

- Nonfarm payroll employment.

- Actual private consumption expenditures.

- Wholesale-retail gross sales adjusted for value adjustments.

- Employment as measured by the family survey.

- Industrial manufacturing.

The Nationwide Bureau of Financial Analysis notes: “There isn’t a mounted rule about what measures contribute info to the method or how they’re weighted in our selections.”

Most of those indicators are at or close to all-time highs and in uptrends. That’s why economists argue we aren’t in a recession.

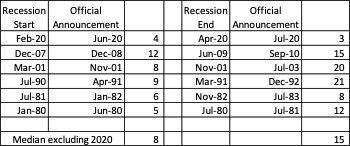

However the issue is that the indications might be at all-time highs when the recession begins. In truth, they usually are.

Economists search for weak spot within the indicators to find out when the recession began. Meaning the willpower will at all times come after the recession is underway. On common, the official announcement comes eight months after the downturn begins.

Word that the desk beneath excludes the 2020 recession as a result of that was a novel information level.

Supply: NBER

This implies shoppers are feeling the ache of recession for months earlier than economists and policymakers agree with them that the ache is actual. Buyers are additionally going through ache throughout that point.

Ignoring the 2020 recession, shares fell throughout the time between the beginning of the recession and the announcement 4 out of 5 instances. Banks shares have been among the many hardest hit throughout that point, dropping a mean of 13%. The worst loss was 39% in 2008. The very best case was a 6% rally in 1980.

Banks are particularly weak throughout that window. The economic system is contracting. However the information doesn’t verify it. This could lead bankers to make unhealthy selections.

Banks are pushed by information even after they acknowledge a state of affairs might finish badly. This was famously summarized by Citigroup’s CEO in July 2007.

The recession hadn’t began but then, however the housing market was already in decline. So have been shares.

In line with The New York Occasions, the previous chief govt infamously mentioned in July 2007 (referring to the agency’s leveraged lending practices): “When the music stops, by way of liquidity, issues will likely be difficult. However so long as the music is enjoying, you’ve received to stand up and dance. We’re nonetheless dancing.”

He admitted that there could be issues. However he couldn’t cease the financial institution from having these points as a result of doing so would imply sacrificing earnings and probably dropping shoppers.

Right now, banks are nonetheless dancing. Historical past tells us that issues will likely be difficult. And they’ll get uglier.

That’s why Adam O’Dell and his group are throughout this. After months of monitoring the monetary banking panorama, they know the more severe is but to return.

They usually’ve discovered a means to assist us put together for what is going to occur when the music ends and extra financial institution failures comply with swimsuit.

Adam went reside yesterday together with his record of 282 American monetary shares he thinks you need to promote now … together with 4 specifically which may be the following to go below.

In fact, it’s not sufficient to easily handle danger in instances of rising inflation.

That’s why Adam’s additionally displaying us place “off Wall Road trades” on a handful of corporations which can be going through main systematic danger for an opportunity to construct wealth throughout the disaster.

All the main points, together with the 4 corporations that will maintain your deposits, are proper right here.

Regards, Michael CarrEditor, One Commerce

Michael CarrEditor, One Commerce

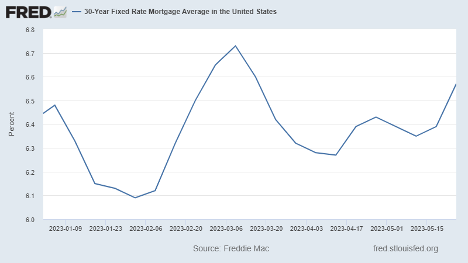

You may need missed it amidst the debt ceiling drama, however U.S. mortgage charges have been quietly creeping larger for weeks. The typical 30-year price is now 6.57%.

Whereas it’s nonetheless beneath the 7.1% hit final November, charges have been pushing larger for many of this yr, and notably over the previous six weeks.

Greater charges make houses much less reasonably priced, particularly for first-time consumers that will not have lots of money available for a down fee.

For instance: A $500,000 home with a $450,000 mortgage at 3% would have a month-to-month principal and curiosity fee of $1,897.

That very same home at right now’s 6.57% charges would have a fee of $2,865. That’s practically $1,000 extra spent on simply your mortgage.

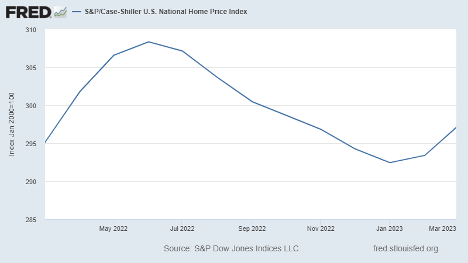

Nevertheless, the harm performed to dwelling costs has been minimal … and it might be over.

The Case-Shiller House Value Index values for March launched this week. And whereas we’re information that’s shut to 2 months outdated by the point it’s launched, the information can nonetheless present us the overall development. House costs rose in each February and March, after a string of declines that began in June of final yr.

Sure pockets of the nation are actually hurting.

For instance, the San Francisco housing market is in unhealthy form following the frenzy of tech layoffs over the previous yr. However nationwide, dwelling costs are roughly flat over the previous yr, and down solely a modest 3.5% from their all-time highs.

Is the decline in dwelling costs over?

Finally, it might rely on whether or not we lastly get that recession we’ve been anticipating for a yr now.

However given that provide stays exceptionally tight, we shouldn’t count on costs to return down an excessive amount of … or not less than not any time quickly.

Regards,

Charles SizemoreChief Editor, The Banyan Edge

Charles SizemoreChief Editor, The Banyan Edge

[ad_2]

Source link