“Quietly” Beat the Market")

[ad_1]

When making an attempt to uncover the type of investor you might be, typically it helps to find out what you are usually not.

For instance, right here’s what I’m not:

- As I discussed final week, I’m not the type of investor to solely “take heed to my intestine.”

- I’m positively not chasing the straightforward commerce of 2023 — mega-cap tech shares.

- However I’m not a Fed-watching, table-pounding perma-bear ready gleefully for the monetary endgame, both.

This already makes me a bit of bit completely different than what you might be used to seeing on the market.

It’d even make me appear a bit of bit boring…

However you recognize what? I’m thrilled to be boring.

As a result of being boring has led my Inexperienced Zone Fortunes subscribers to a close to 400% return up to now three years on a inventory I’ll inform you about at the moment.

You’ve in all probability by no means even heard this inventory’s identify earlier than. But, it’s outperformed practically each mega-cap tech inventory that will get mentions on CNBC each hour of each single buying and selling day.

In reality, those self same shares are this firm’s greatest prospects.

I guarantee you, this isn’t going to be a full-bore brag piece (regardless that I’d say we’ve earned it).

As a substitute, I’ll share the ticker that my subscribers are up practically 400% on… Present you why I noticed this achieve coming virtually three years in the past… And the straightforward, three-point technique you must use if you wish to discover shares similar to this one.

How STRL Quietly Bested Its Personal Clients

Sterling Infrastructure (STRL) is a inventory market outlier you’ve in all probability by no means heard of.

It’s finest described as a “picks-and-shovels” play on each e-commerce and cloud computing. Although, you wouldn’t realize it from studying the corporate description.

The corporate used to concentrate on the comparatively low-margin enterprise of fixing roads, bridges and sewage techniques. Today, it principally builds warehouses and information facilities for the massive tech firms who want them… and quite a lot of different big-name prospects.

That’s everybody from Amazon, Microsoft and Google… to Walmart, UPS and Dwelling Depot.

All of those firms go to Sterling once they need assistance constructing out their digital and real-world logistics networks.

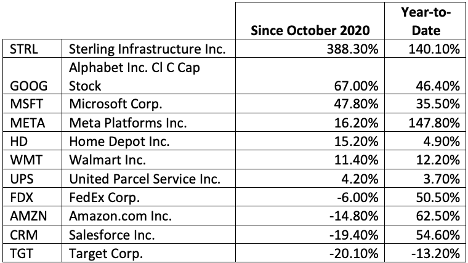

That’s why it ought to be no shock STRL is up extra year-to-date than all of its prospects mixed… And was solely outdone by one in every of them — META, which we’ll get to in a second.

Even when we examine Sterling to its opponents within the infrastructure house, the returns from October 2020 hardly come shut:

This outperformance doesn’t come from nowhere.

One large purpose STRL is so head and shoulders above its competitors (and prospects) is that it’s one in every of only a handful of shares that mainly “skipped” the 2022 bear market.

STRL fell simply sufficient to enter “bear territory” — a hair above 20% — nevertheless it’s nothing in comparison with the a lot deeper drawdowns mega-cap techs suffered.

You see, when a inventory suffers such a significant drawdown, you want a fair larger comeback simply to get again to breakeven. Much less risky shares, like STRL, can get better rather more shortly.

And that brings me again to META…

META has outperformed STRL in 2023, by a smidge.

However, META was down 71% from January 1, 2022, to the worst level in November. Despite the fact that shares have rallied massively since, beating STRL’s year-to-date return, META remains to be down 4.4% from the place it began final 12 months. To distinction, STRL is up over 200% over the identical time.

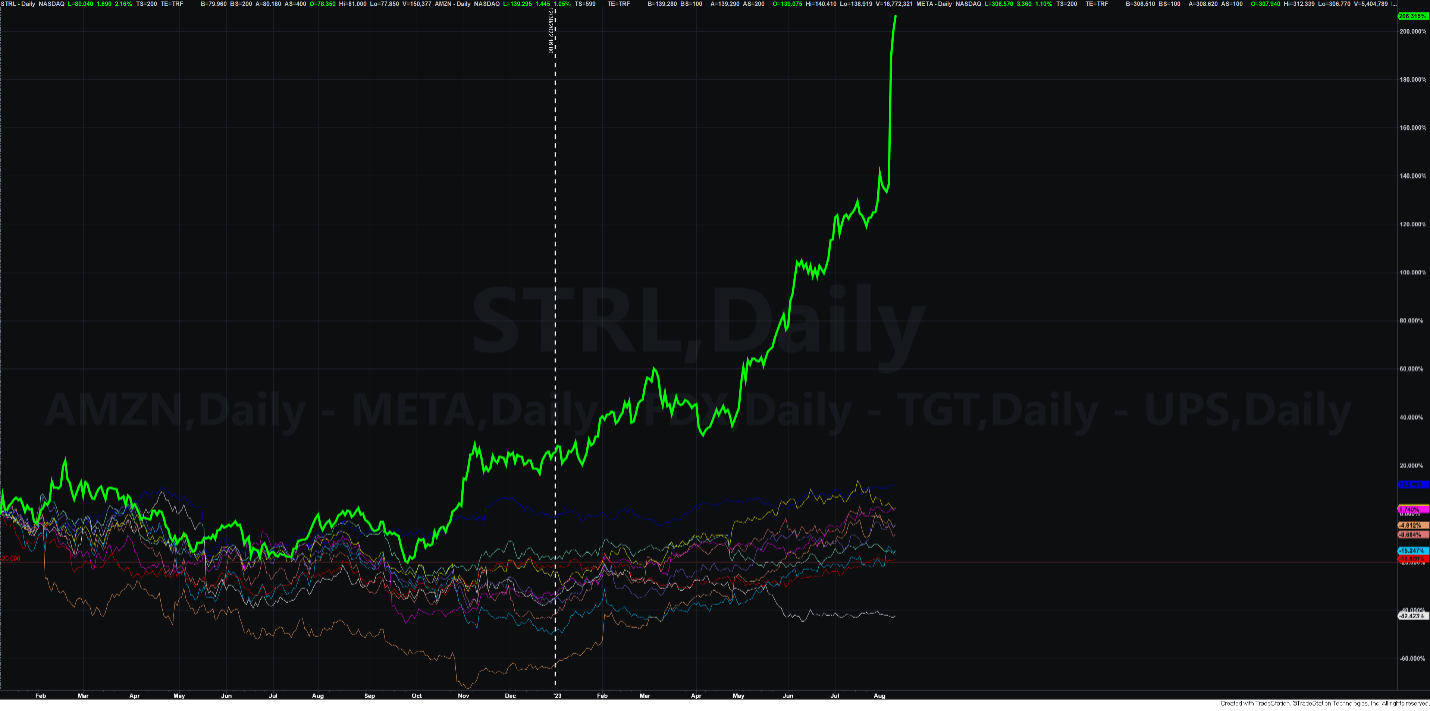

It’s the long-term returns that rely. And right here, STRL gives in spades.

Simply have a look at this chart evaluating STRL to all the opposite shares within the first desk above.

STRL has damaged from the pack in spectacular style.

However why precisely is that the case?

Discovering the Golden Trifecta

There are many methods an organization can generate optimistic returns for its shareholders. However few of them are as constant as these three strategies:

- Develop revenues.

- Broaden revenue margins.

- Earn the next a number of on earnings.

It’s potential to make good cash on a inventory when even one of these three issues occur. However the exceptional returns come when all three happen on the similar time — one thing I name a “Golden Trifecta.”

Sterling has achieved precisely this mix of return-driving qualities. And it didn’t do it as a result of it’s merely a large-cap tech firm popping out of a bear market.

It did it regardless of that … as a development firm that appears boring on its face, however screams worth as quickly as you have a look at its buyer Rolodex.

In reality, the corporate’s worth was its greatest draw once I first beneficial it. I put it to my subscribers like this…

An organization can management how a lot it earns. However it may possibly’t management how a lot buyers are keen to pay for these earnings.

By means of the P/E ratio, we are able to see how a lot buyers are keen to pay for every greenback of firm earnings.

A excessive ratio — say, 30 instances earnings — signifies buyers are keen to pay as much as get in on the motion. A low P/E ratio — say, 10 instances earnings — exhibits both an absence of curiosity as a result of earnings aren’t rising … or a blind spot.

In STRL’s case, it was a blind spot. I noticed three years in the past that the corporate was set to satisfy a necessity of the world’s greatest tech firms. And it was clear to me that not many different buyers noticed the identical factor.

After I beneficial it, the inventory was grossly undervalued in comparison with its friends and ranked a 97 on the Worth issue of my Inexperienced Zone Energy Scores system. In my authentic write-up of the corporate, I stated:

We’re shopping for into Sterling at the moment at a price-to-earnings (P/E) ratio of simply 8.3. That’s lower than one-third of its opponents’ common valuation.

Which means Sterling’s share value might triple — from $15 to $45 — and it might nonetheless be a greater worth!

As we see at the moment, Sterling share value did triple … after which some.

And that’s exactly as a result of it was a “boring” firm that the majority buyers by no means heard of … and is now one many buyers are very a lot conscious of.

In the event you’re a paid-up Inexperienced Zone Fortunes subscriber, I urge you to reread my authentic October 2020 advice on Sterling. You possibly can entry it right here. There I am going into the nitty-gritty of why STRL was such a transparent success story within the making even again then.

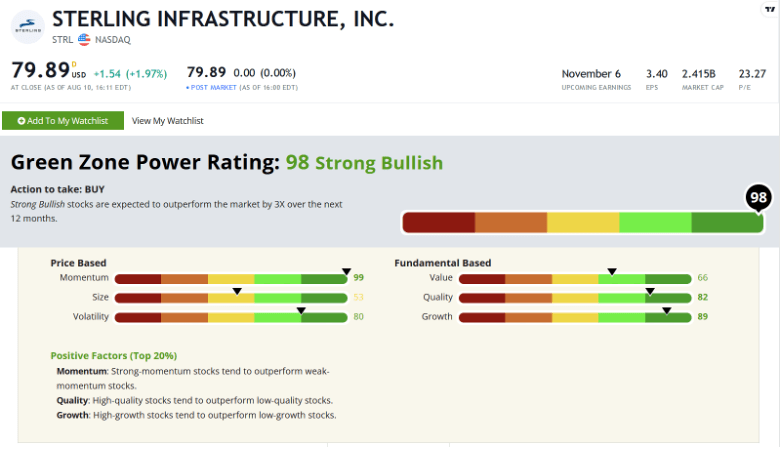

As for what to do with STRL now, my Inexperienced Zone Energy Scores system nonetheless flags it as a powerful purchase. It charges a 98 total at the moment — even increased than once I first beneficial it:

I’ve a value goal that I shared with Inexperienced Zone Fortunes readers, setting us as much as seize a a lot larger achieve in what I hope is the close to future.

If you wish to learn to be part of us, and get an alert to your electronic mail inbox when it’s time to promote, click on right here.

To good income,

Adam O’Dell

Adam O’Dell

Chief Funding Strategist, Cash & Markets

An Unlikely Recession Catalyst

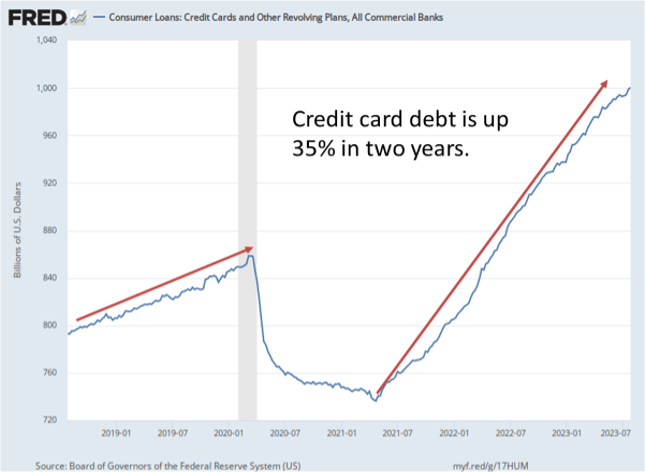

You might need seen the headlines earlier this week. Individuals crossed an unlucky milestone, amassing $1 trillion in bank card debt for the primary time.

It’s not the quantity that will get my consideration. Although, let’s face it, $1 trillion is some huge cash to have racked up on bank cards.

The saddest facet to me is that all of us received a collective mulligan in 2020. Bank card debt truly fell about 14% in 2020 and early 2021. Outdoors of meals service, leisure and retail, most Individuals’ incomes have been unaffected by the COVID-19 pandemic, whereas their bills truly lessened.

There was nowhere to go, and you’ll solely order so many containers on Amazon earlier than that will get exhausting. Add to that the multiyear vacation on pupil mortgage funds and free checks from the federal government, and tens of millions of Individuals had an actual probability to get out of debt and begin with a clear slate.

We received a do-over!

And it appears we blew it…

Sadly, that’s not all. Not solely have we resumed the street to monetary wreck … we’ve slammed our foot on the fuel.

Evaluate the 2 crimson arrows within the chart above. Discover how the more moderen one is far steeper? Properly, we’re racking up debt at a a lot sooner tempo than we did pre-2020. Bank card debt has managed to blow up 35% increased in simply two years.

To be truthful, inflation performed a job right here. With the price of residing rising as quick as it’s, one thing has to offer, and plenty of Individuals have needed to observe its lead so as to cowl the distinction.

I’m extra involved about what this implies for the long run.

There comes a degree when bank card balances develop into unsustainable. The minimal funds develop into too excessive, and the banks cease providing you new credit score. When that occurs, you haven’t any alternative however to chop again in your spending.

And when that occurs to sufficient individuals, you find yourself with a recession.

Are we there but?

The info suggests we aren’t. However that may change shortly. And with pupil mortgage funds set to renew within the coming weeks, we might even see cash-strapped Individuals having to decide on between paying their bank card balances or paying their pupil loans. In both case, they’re nonetheless going to have much less money free to spend.

In the event you’re searching for the potential catalyst for the subsequent recession … I feel we’ve discovered it.

Regards, Charles SizemoreChief Editor, The Banyan Edge

Charles SizemoreChief Editor, The Banyan Edge

[ad_2]

Source link