[ad_1]

He made $100 million for himself and $700 million for his traders in 2008.

And now he’s at it once more.

Michael Burry predicted the 2008 international monetary disaster, guess towards the housing market and made a fortune.

There was even a film made about him.

So when Burry tweets, folks listen.

In a publish on X (previously Twitter), on September 29, 2022, Michael Burry predicted one other crash.

This time he’s betting that the inventory market will crash…as soon as once more.

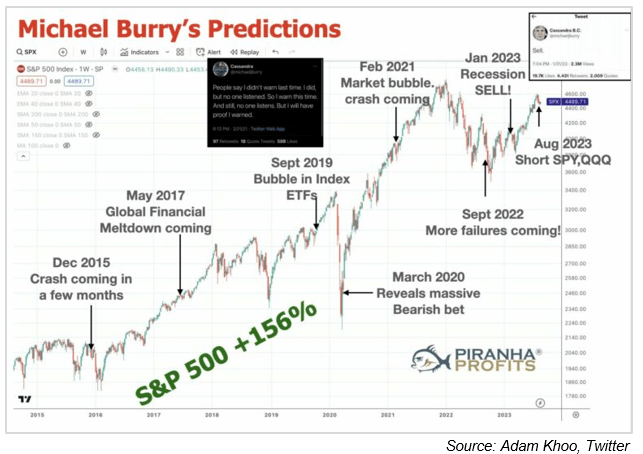

Anytime I see a prediction, I take a look at how earlier predictions panned out.

And Burry’s document of creating huge predictions leaves so much to be desired:

- 2005, he predicted the collapse of the subprime mortgage market. Everyone knows what occurred in 2008…

![]()

- 2015 predicted one other crash — the S&P 500 surged 11%…

![]()

- 2017 predicted a world monetary meltdown — S&P climbed 19%…

![]()

- 2019 predicted a inventory market crash as a consequence of a bubble in index ETFs — the market gained 15% the next 12 months…

![]()

- 2020 made one other bearish guess — the S&P rocketed 72% and he needed to challenge an apology on social media…

![]()

- 2022 — the market shattered one other of his market crash predictions with a 21% surge…

![]()

Burry’s observe document begs the query …why would anybody take heed to his predictions?

(Click on right here to view bigger picture.)

Yogi Berra was spot on when he mentioned: “It’s powerful to make predictions — particularly in regards to the future.”

The underside line, people, is that this … nobody has a crystal ball.

It’s unattainable to foretell the long run and be proper on a regular basis.

I’ve a greater approach … that’s labored for me in addition to a number of the biggest traders of all time.

With out making predictions, I’ve helped my readers make open beneficial properties of 215% in 4 years, 356% and one other 186% in three years.

Right here’s how…

Suppose In a different way

I’m an Alpha Investor.

Which means I don’t want or use crystal balls, astrology, sunspots or learn tea leaves to earn a living within the inventory market.

Alpha Buyers stand head and shoulders above the remaining as a result of…

We don’t make investments as a result of others agree or disagree with us.

We make investments as a result of our info and evaluation are proper.

We’re assured in our choices and don’t want affirmation.

We don’t keep in the midst of the pack … we lead.

We’re not afraid of stepping out.

We expect in a different way than different traders.

THAT’s how we earn a living.

With that mindset, I assist Fundamental Avenue Individuals put money into Alpha corporations … shares that can return a minimal of 100% inside 4 years.

To search out these corporations, I be certain it meets my “4 Alpha Pillars”:

- Alpha Market: Investing in an organization driving a mega pattern.

- Alpha Management: Run by a CEO with integrity, expertise and a confirmed observe document.

- Alpha Cash: In an organization that has a rock-solid stability sheet.

- Alpha Value: When the inventory worth is buying and selling under the underlying price of the enterprise — that’s an excellent worth.

For those who’re fed up with mediocre returns, story over substance or simply wish to begin earning money — I invite you to be an Alpha Investor.

As a result of Alpha Buyers are a breed aside.

Regards,

Charles Mizrahi

Founder, Alpha Investor

Consideration Alphas: Charles noticed his 4 Alpha Pillars flashing in a single sector. A bull market is simply getting began on this Alpha Market. So, if you need his favourite inventory suggestion (buying and selling for lower than $15 proper!) — click on right here for the main points now.

The Credit score Card Disaster

We’re already beginning to see the primary indicators of stress.

Two weeks in the past, I commented that bank card debt had topped $1 trillion for the primary time… and that balances had exploded larger by 35% in simply two years.

Now, a trillion {dollars} is some huge cash.

However in a vacuum, that quantity doesn’t essentially imply a lot. It’s not the stability that disturbed me. It was the pace with which we obtained there that raised the crimson flags for me.

And about that…

Purple Flags

Purple Flags

A current report by JD Energy discovered that solely 49% of Individuals with a bank card are capable of repay the stability every month.

51% of Individuals with a card now carry a stability … and at a mean price of 14.8%.

Now, it’s not the 51% by itself that’s the drawback. If that was a static quantity, I’d shake my head in disapproval, however I wouldn’t essentially take into account it trigger for alarm.

However that quantity isn’t static…

And it’s trending larger.

In reality, that is the primary time within the historical past of the survey {that a} full majority of American bank card holders have been unable to pay their balances in full every month.

After all, you know the way bank card balances work.

When you get right into a gap … it’s actually laborious to dig your self out.

Notably while you’re paying pawnshop rates of interest. The debt snowballs and, for a lot of, finally ends up changing into unpayable.

And naturally, all of that is occurring earlier than pupil mortgage funds restart subsequent month. Including a number of hundred {dollars} of debt cost into the combo will little doubt push the variety of at-risk bank card holders so much larger.

Hassle Forward?

Are the banks in bother? Not likely…

Sure, they are going to take losses, and their shareholders received’t be comfortable, however this received’t be sufficient to essentially blow them up. This isn’t as harmful because the mortgage disaster that took down the banking sector in 2008.

My concern is what it means for client spending.

In some unspecified time in the future, bank card debt turns into unpayable for a big swath of debtors, and the defaults begin … which forces the banks to tighten lending requirements and minimize some debtors off.

Each greenback not borrowed is a greenback not spent. And each greenback used to pay down debt is successfully two {dollars} not spent.

We shouldn’t underestimate the economic system’s skill to muddle by far longer than we think about doable.

If we’re on the lookout for that proverbial straw to interrupt the camel’s again … this is perhaps it.

Have you ever ever needed to repay bank card debt earlier than? Let me know your ideas right here.

Regards,

Charles Sizemore

Chief Editor, The Banyan Edge

[ad_2]

Source link