(NASDAQ:STRL)")

Lari Bat

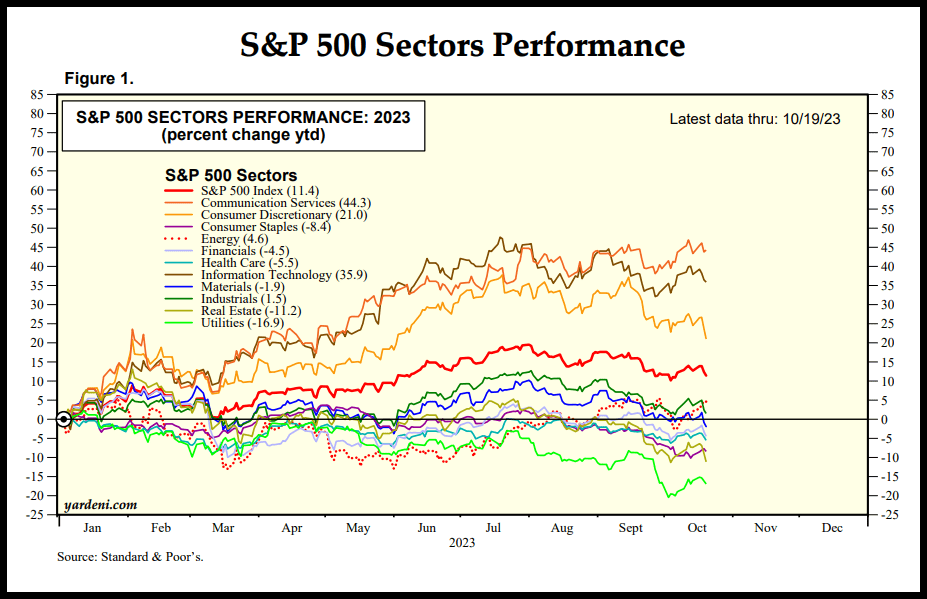

Actual property (XLRE) continues to be one of many worst-performing sectors, -10.86% YTD, amid traditionally excessive charges, tight provides, and customers’ reluctance to buy after locking in traditionally low charges in the course of the pandemic.

S&P 500 Sectors Efficiency (Yardeni Analysis, S&P)

Mortgage charges are nicely above 7%, dampening gross sales, which is why Firstam deputy chief economist Odeta Kushi acknowledged, “Immediately’s housing market is not something just like the housing market of the mid-2000s – the housing market immediately just isn’t overbuilt, neither is it pushed by free lending requirements, sub-prime mortgages, or householders who’re extremely leveraged.” Regardless of tight provides and the slowdown within the housing market, costs proceed to climb, posing alternatives for buyers all in favour of construction-related shares.

Moderately than have interaction in bidding wars, some homebuyers want to construct from the bottom up. The iShares U.S. House Development ETF (ITB) is +18% YTD and up almost 44% over the past yr. Along with the uptick in U.S. house development, the SPDR® S&P Homebuilders ETF (XHB) is +16.95% YTD. Though provide chain constraints and financial uncertainty are potential dangers, particularly given the present geopolitical and macroeconomic considerations for industrials, a few of the fall in development shares could show to be nice buy-the-dip alternatives. Sterling Infrastructure (NASDAQ:STRL) fell as a lot as 15% intraday on October thirteenth amid promoting pressures but gives wonderful fundamentals and a powerful outlook. Tripling its share worth over the past yr amid an increase in infrastructure tasks, think about this prime inventory for a portfolio.

Sterling Infrastructure, Inc. (STRL)

-

Market Capitalization: $2.21B

-

Quant Score: Sturdy Purchase

-

Quant Sector Rating (as of 10/20/23): 6 out of 654

-

Quant Trade Rating (as of 10/20/23): 3 out of 34

Providing a buy-the-dip alternative after its decline in latest weeks, Sterling Infrastructure is an trade chief in E-infrastructure, large-scale web site growth for information facilities, transportation, and constructing options. Delivering super top-line progress and increasing margins, Sterling’s observe file of differentiated, higher-margin freeway development and engineering permits STRL to boast of constructing, creating, and facilitating change and that “Our folks work smarter, not more durable” to provide excessive outcomes for the group. After the Utah Division of Transportation awarded a big freeway venture and a $216M UDOT contract with its three way partnership associate, W.W. Clyde & Co., Sterling is an undervalued firm that provides sturdy progress and profitability by strategic execution.

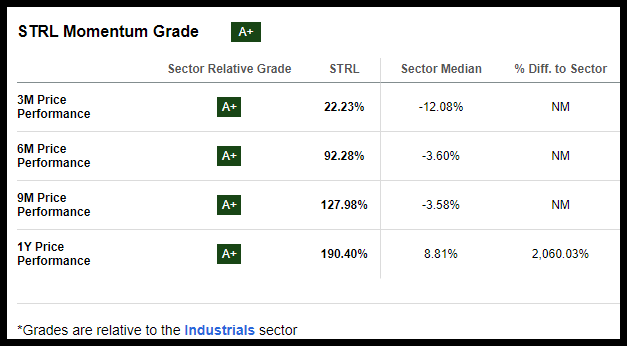

STRL Inventory Valuation and Momentum

Regardless of Sterling Infrastructure’s bullish momentum, with a YTD value efficiency of +109% and +183% over the past yr, STRL maintains a reduced valuation.

STRL Inventory Momentum Grades (SA Premium)

Sterling’s quarterly value efficiency considerably outperforms the sector median and its B- Valuation Grade is supported by a ahead PEG of 0.88x versus the sector median of 1.61x. Sterling’s ahead Value/Gross sales is a 13% low cost to the sector, and the corporate has a powerful 6.17x Value/Money Circulate (TTM) in comparison with the sector’s 12.33x. Contemplating its steadily growing quarterly value efficiency and A+ momentum, I imagine this inventory is primed for potential upside.

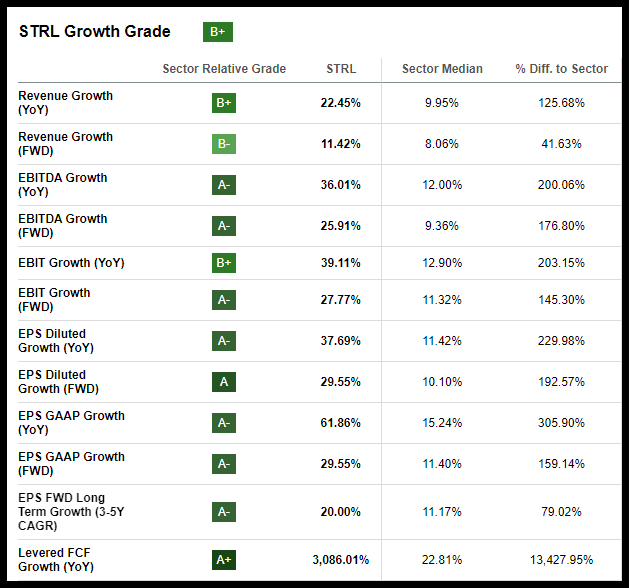

STRL Inventory Progress and Profitability

Because the pattern for car electrification grows, Sterling Infrastructure has seemed to capitalize. Nabbing an EV battery facility venture for Hyundai and a $45M web site growth contract for Rivian’s Georgia EV facility, it must be no shock why STRL was chosen as one in all my Prime 10 Shares for the second half of 2023 and was chosen by one of the best of one of the best quant shares for Alpha Picks.

STRL Inventory Progress Grades (SA Premium)

Sterling Infrastructure’s progress is powerful on the heels of 9 back-to-back earnings beats. Exceptionally sturdy money flows for its newest earnings beats and 42% progress in its backlog from year-end 2022 have allowed its steadiness sheet to be in nice form. Sterling’s Q2 2023 EPS of $1.27 beat by $0.35, and income of $522.33M beat by and margin producing segments. STRL delivered 22% natural top-line progress. Highlighted by its President and CEO, Joseph Cutillo, in the course of the Q2 earnings name,

“Our persons are out within the discipline day by day, utilizing their entrepreneurial spirit to win tasks, execute flawlessly, and push Sterling to the following degree…Our sturdy backlog place provides us confidence in our beforehand issued steerage ranges, which we’re reiterating immediately. Primarily based on our first quarter outcomes, we imagine we’re monitoring in direction of the excessive finish of our 2023 steerage, which suggests a 13% enhance in income and a 14% progress in web revenue.”

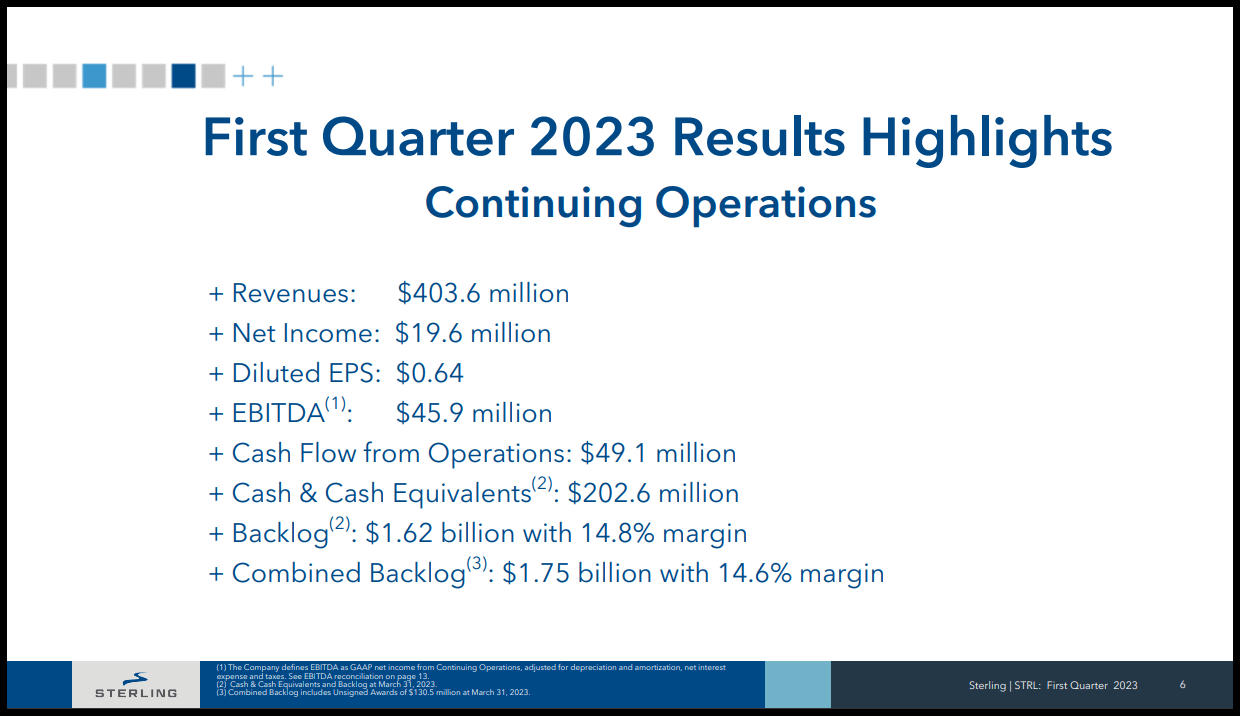

STRL Inventory Q1 Outcomes (STRL Inventory Q1 2023 Investor Presentation)

Sterling’s backlog totals $1,624B, up $210M from the start of the yr, and its, backlog gross margins have been almost 15%, its best backlog margin in historical past. Given the super progress, two Wall Road analysts have revised their FY1 estimate up over the past 90 days with zero downward revisions. With plans to profit from the 2021 Infrastructure Invoice and a path towards sustainability, STRL hopes to increase its geographic footprint, income, and margins. With the easing of provide chains since COVID, Sterling has recaptured a few of the losses from inefficiencies that impacted their margins in the course of the pandemic and plans to ramp up its giant tasks.

Potential Dangers

Provide chain constraints and macroeconomic challenges can pose dangers to industrials, particularly amid larger charges and customers’ budgets. The surge in Rates of interest and value of uncooked supplies has prompted many corporations to really feel the consequences of elevated bills – an hostile impact on corporations. Larger leverage tends to create larger quantities of curiosity to be paid, which may show taxing for corporations struggling to repay loans. The costly price of capital for corporations unable to provide returns could discover it difficult to remain afloat financially ought to a market slowdown happen.

Labor shortages and well being and security hazards additionally have an effect on the development and engineering industries. Though security is a priority, STRL prides itself on attaining one of many trade’s finest security data – the cornerstone of its operations.

Concluding Abstract

Industrials, specifically development, have skilled some volatility as financial slowdown, inflation, and geopolitical fears create headwinds. The place many corporations lack progress or are buying and selling at poor valuations, STRL is powerful on every of the 5 core traits of valuation, progress, profitability, momentum, and EPS revisions.

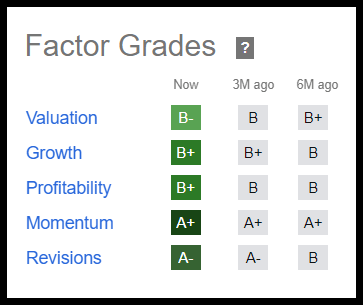

STRL Inventory Issue Grades

STRL Inventory Issue Grades (SA Premium)

Searching for Alpha’s Issue Grades fee funding traits on a sector-relative foundation, and STRL is without doubt one of the best-performing development and engineering shares over the past yr. With a wholesome backlog of enterprise, high-margin tasks within the pipeline, and its innovation and diversified segments, STRL is in an excellent place financially and has sturdy momentum. Think about shopping for STRL long-term in a sector generally known as one of many industries driving the U.S. financial system.

We have now many Prime Industrial shares to select from, or in case you’re in search of a restricted variety of month-to-month concepts from the tons of of prime quant shares, think about exploring Alpha Picks.