Probably the most anticipated second for bulls arrived on Friday. Ever since June, buyers had been sure that the Federal Reserve will ship the goodies in 2023. Each information level was seen with this view. Absolutely, the central financial institution that didn’t see inflation coming in 2020 and noticed it as transitory in 2021, would search for excuses to start out charge cuts in 2023? Not occurring.

Powell’s Speech

The phrase plot on the speech just about instructed you what you wanted to know. It was about excessive inflation and it was about reasserting management on the narrative.

Twitter

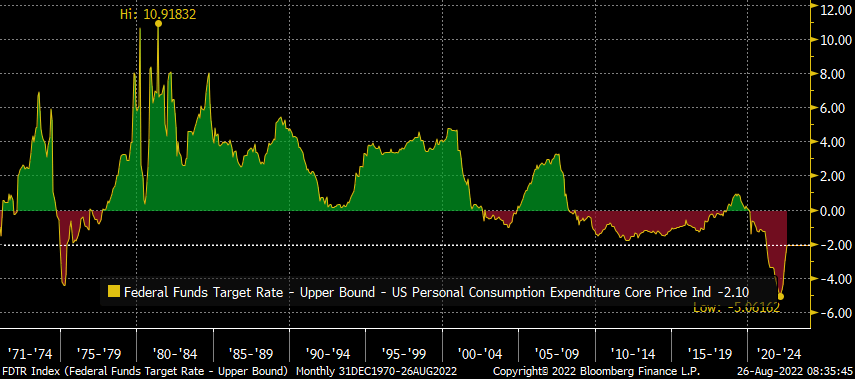

Traders have to appreciate that there are not any goodies coming their means. Powell and Co. could decelerate the tempo of charge hikes, even pause to reassess, however they don’t seem to be reducing, not with their most well-liked measure of inflation being 5% increased than Fed Funds charge.

Richard Bernstein-Twitter

You would possibly discover that it’s nonetheless probably the most destructive quantity within the final 50 years. What does this aggression imply to your investments? We cowl that underneath 4 areas.

US Financial system

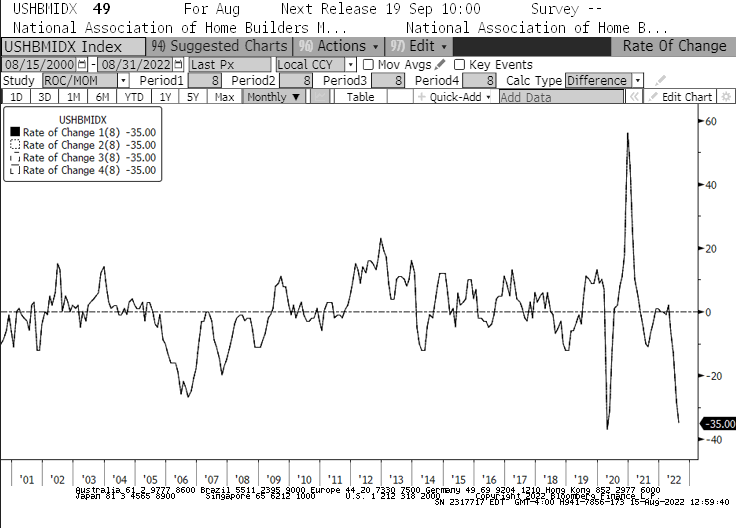

The most important large headwind dealing with US particularly is that housing is totally tanking.

Steph Pomboy-Twitter

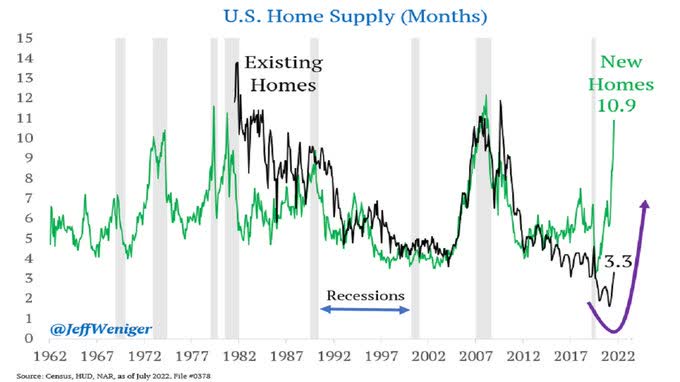

Provide of recent properties is now at 11 months of gross sales.

Jeff Weniger-Twitter

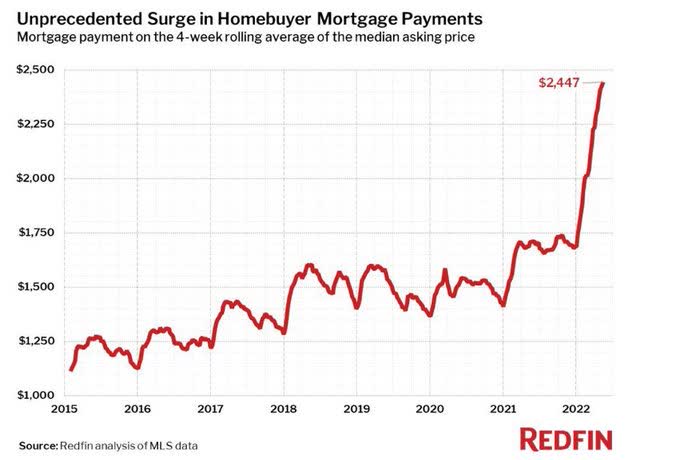

Nobody needs to be shocked by that contemplating the place funds have gone.

Redfin-Twitter

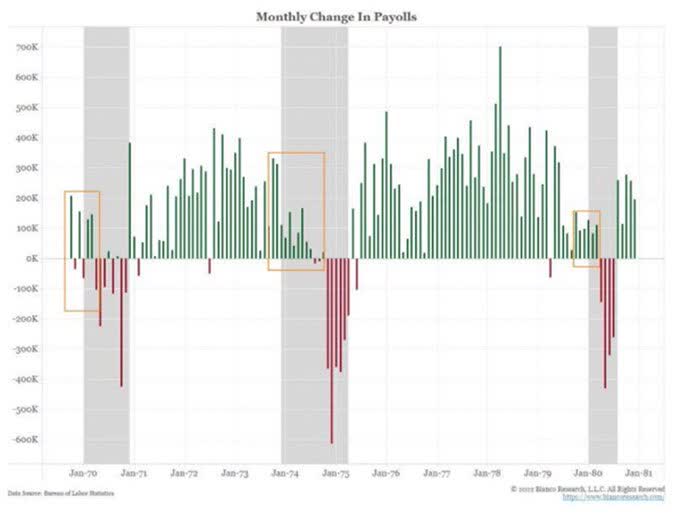

Labor Markets look sturdy, however that’s anticipated in stagflationary recessions.

Twitter

International Financial system

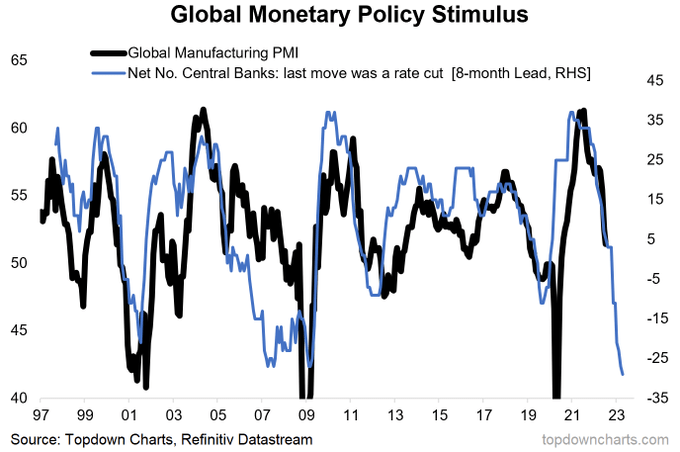

It’s not simply the US Federal Reserve that’s tightening. Most others are and the outcomes will not look fairly. International PMI is prone to crash proper right down to the 40s.

TopDown Charts-Twitter

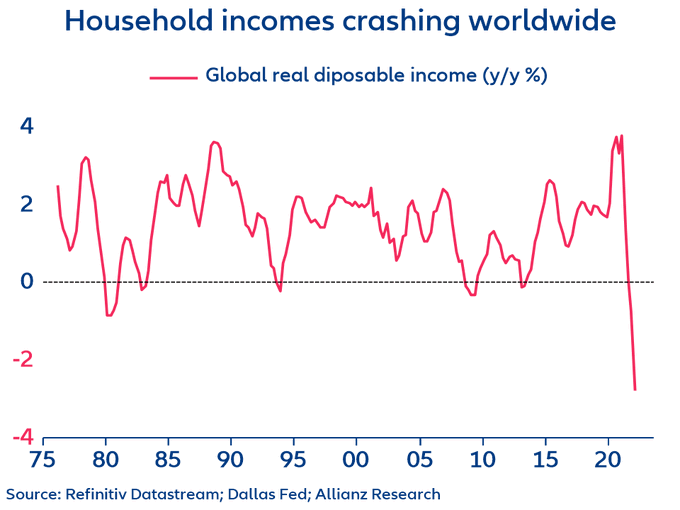

That matches in keeping with how rapidly actual (adjusted for inflation) disposable incomes are crashing.

Dallas Fed-Twitter

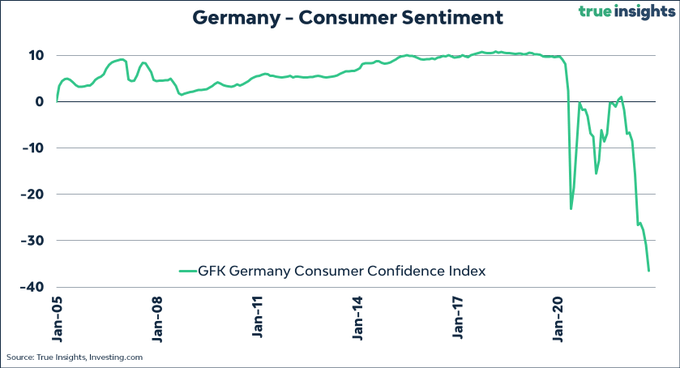

We outlined the problems in China lately and Europe’s powerhouse Germany seems to be about as unhealthy.

True Insights

The chart above needed to be rebased to accommodate that sentiment.

Earnings

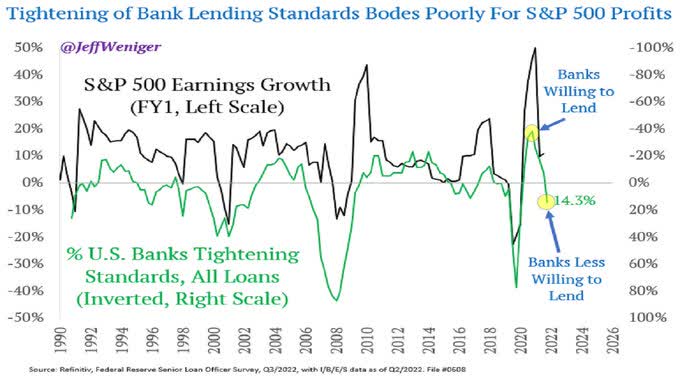

Earnings all the time do far worse than what buyers anticipate in a recession. As banks tighten lending, income observe decrease.

Jeff Weinger-Twitter

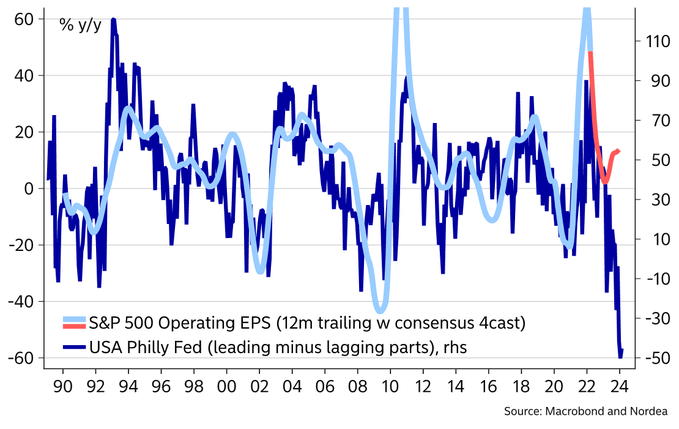

The Philly Fed Mannequin for earnings delta is the bottom it has been.

Nordea

Consensus is in search of $230 in earnings for the S&P 500 (SPY) subsequent yr. We’re in search of $180 in our best-case situation.

Outlook For The Markets

Powell will pivot after the markets transfer far decrease and inflation subsides. If there’s a untimely flip, it is going to be as a result of the financial system performs extraordinarily badly relative to even their pessimistic expectations. Bear in mind in that case, shares will ignore the central financial institution stimulus till valuations normalize. We witnessed this in each the 2009 and 2001 recessions. We’d anticipate a sub 3,000 SPX in that situation.

If our greatest case involves cross and we do ship $180 in earnings on SPX, the markets may do higher. If the Federal Reserve aggressively eases into that as a result of inflation falls, we may help an 18-20X a number of on that degree of earnings. That will get us to SPX 3,240 – 3,600. Keep defensive.

Please be aware that this isn’t monetary recommendation. It might seem to be it, sound prefer it, however surprisingly, it’s not. Traders are anticipated to do their very own due diligence and seek the advice of with knowledgeable who is aware of their aims and constraints.