Blue Harbinger Analysis, Massive Dividends PLUS Daria Nipot")

2022 was an unsightly 12 months for development shares. And it’ll worsen for a lot of of them (because the pandemic bubble continues to burst). On this report, we rank 100 high development shares based mostly on the monetary metrics we take into account most vital within the present market atmosphere (i.e. how they perform with greater rates of interest). Now we have a particular give attention to Amazon (NASDAQ:AMZN), evaluating it to friends on these similar monetary metrics, but in addition diving into its particular enterprise fundamentals, together with aggressive benefits (not simply scale and Amazon Internet Providers, but in addition subscriptions like Prime and its burgeoning promoting enterprise), dangers and valuation. We conclude with our robust opinion on Amazon and investing in choose development shares within the present market atmosphere.

100 Development Shares, Ranked

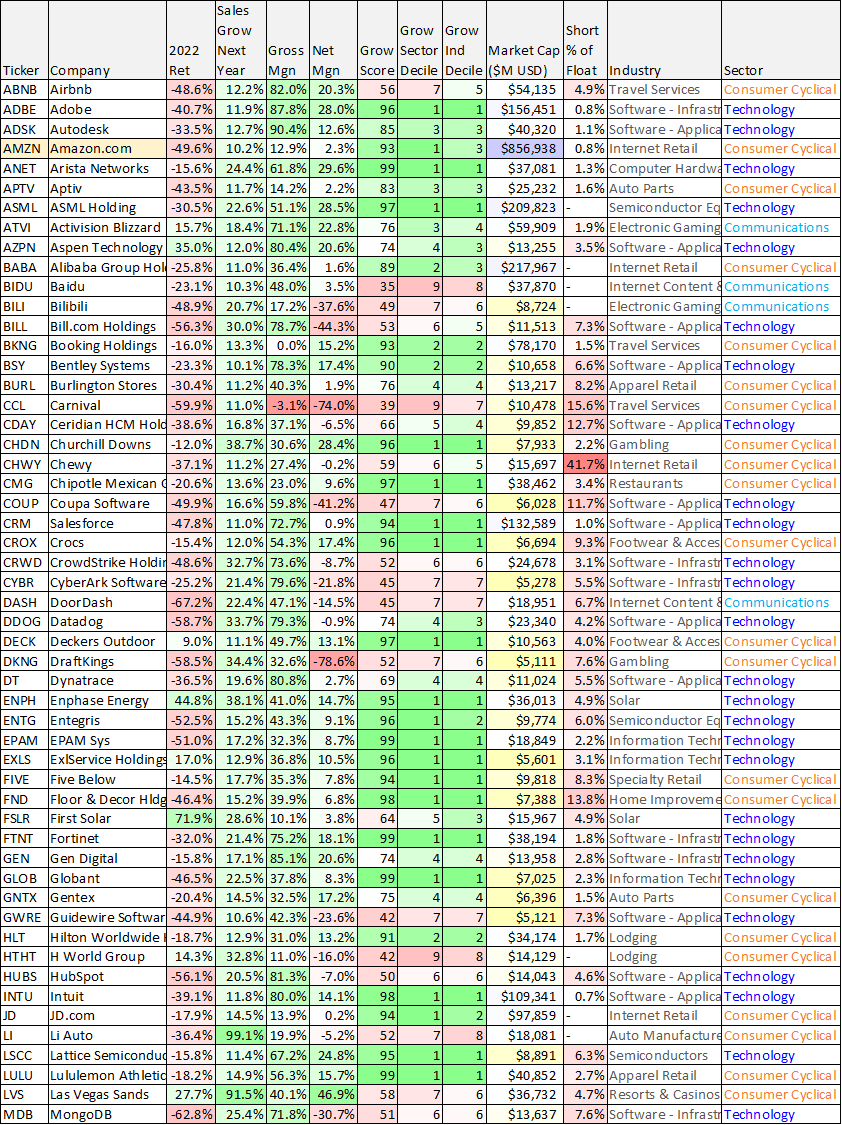

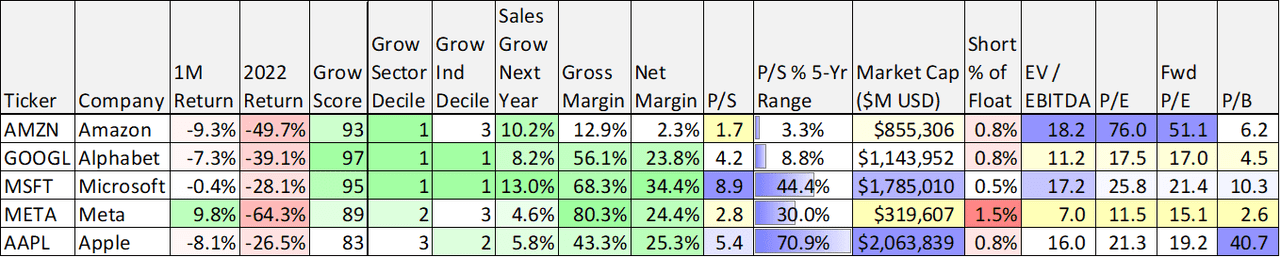

Earlier than entering into the main points on Amazon, right here is our high-level rating of 100 high development shares (see beneath). To be included on this desk, we required at the very least a ten% anticipated development price for subsequent 12 months (lots of them are a lot greater) and a market cap of at the very least $5 billion. We additionally restricted the desk to the three worst-performing market sectors of 2022: Expertise, Communications and Client Discretionary.

One huge theme behind this desk is that worthwhile companies (these with optimistic web earnings margins) have carried out loads higher than these that aren’t worthwhile (as you’ll be able to see within the desk beneath). This has loads to do with quickly elevated rates of interest (greater charges means funding development is dearer, future earnings are discounted extra, and financial development is slower; to not point out issuing new shares is much less engaging for companies now that share costs are down considerably). The desk is sorted alphabetically by ticker.

information as of 31-Dec-2022 (Inventory Rover) information as of 31-Dec-2022 (Inventory Rover)

(ASML) (BABA) (CRM) (DDOG) (EPAM) (SNOW) (SHOP) (SE) (NET) (TTD) (PAYC) (PLTR) (SQ) (SPLK) (NOW) (CRWD) (ENPH) (FTNT) (MELI) (COUP)

For reference, the expansion rating within the desk appears on the 5 12 months historical past, in addition to ahead estimates, for EBITDA, Gross sales, and EPS development. One of the best corporations rating a 100 and the worst rating a 0. We additionally included sector and business development deciles (1 is greatest, 10 is worst) to assist make the scores extra comparable. You doubtless acknowledge at the very least a couple of of your favourite development shares on the record.

You will have additionally seen that Amazon, one of the crucial well-liked and widely known enterprise names on this planet, was down ~50% in 2022, however ranks properly within the desk.

Amazon![]()

Amazon Enterprise Overview:

If you do not know, Amazon divides its enterprise into three segments (North America, Worldwide and Amazon Internet Providers), however that may be a little bit of a disservice to analysts contemplating primarily 100% of the revenue is generated by AWS. North America and Worldwide are principally the geographical breakdown of retail gross sales, which generate primarily zero revenue on a section foundation, however have very worthwhile and rising sub-areas in these segments (primarily subscriptions like Prime and the burgeoning promoting enterprise) that can doubtless be development and revenue drivers sooner or later. Most of Amazon’s revenues come from North America (~60%) and Worldwide (~27%), however just about all revenue (100%) at present comes from its third section, AWS.

Aggressive Benefits:

Amazon has big aggressive benefits over its friends stemming from huge economies of scale (which allow it to ship low price companies) and community results, as described beneath.

(for instance, Amazon gathers all kinds of details about customers that can assist its promoting efforts).

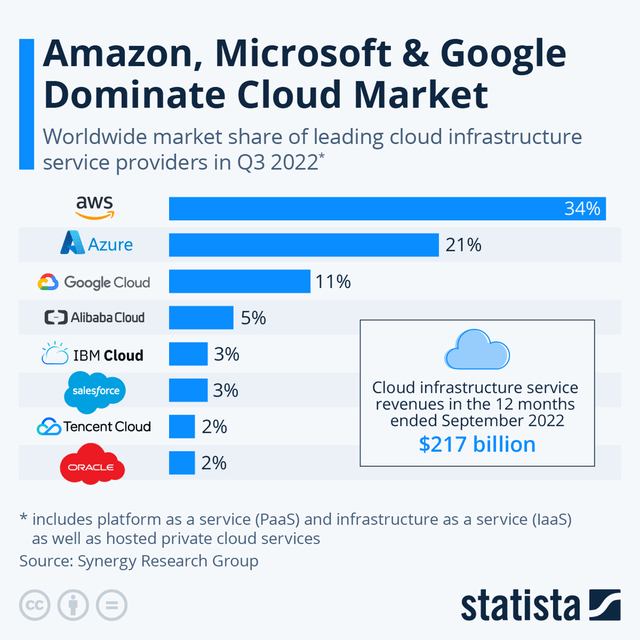

Amazon Internet Providers (“AWS”): For starters, AWS is the main cloud companies supplier (forward of Microsoft Azure (MSFT) and Google Cloud (GOOGL)), and this section has huge long-term development potential stemming from the continued digital transformation and migration to the cloud (an infinite long-term secular pattern that has slowed in current months, however continues to be solely simply starting when it comes to long-term alternative).

Statista

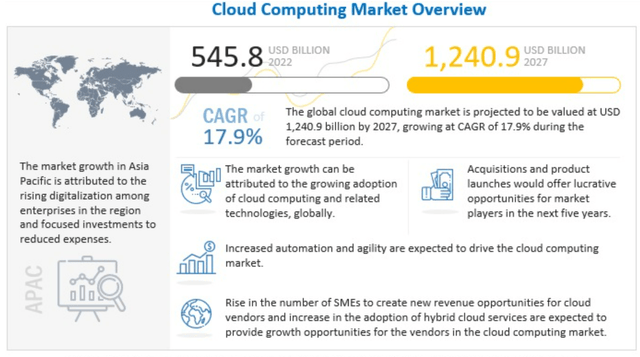

For some perspective, the cloud alternative is predicted to develop dramatically over the following 5 years (and considerably extra within the years after that) as proven on this subsequent graphic.

supply: Markets and Markets

Promoting: And whereas AWS is the one worthwhile of the three major segments, promoting is a smaller, but-high-margin enterprise that already has some scale plus vital extra room to continue to grow. Amazon promoting is particular as a result of it naturally has tons of eyeballs (i.e. folks utilizing Amazon’s platform already) and it has entry to huge proprietary information (together with actual time information). It’s these community impact advantages (present eyeballs, distinctive proprietary information, and scale), mixed with vital room for continued development, that make Promoting an vital future development diver for Amazon.

Amazon Prime: Prime memberships are additionally particular for Amazon as a result of they assist entice sticky prospects and so they generate high-margin recurring income. Amazon Prime is principally a subscription service ($139 per 12 months) that features quick transport, unique gross sales, free film streaming and free entry to Amazon’s 100 million music music catalog, to call just some. What’s extra, Prime helps convey customers into the ecosystem, and as soon as they’re in they use Amazon greater than they’d have and so they’re much less prone to depart (i.e. improved buyer retention).

Amazon Retail: Amazon’s web site and retail enterprise is the very first thing that involves thoughts for many individuals. What’s vital to notice about this enterprise is that it has huge revenues however very slender revenue margins. Nonetheless, it is a important piece of the ecosystem as a result of it brings folks to Prime, it creates the platform for promoting and it led to the creation of AWS (Amazon had an enormous head begin versus different cloud suppliers as a result of it had already constructed out nice cloud experience in bettering its personal web site).

Total, Amazon’s spectacular ecosystem and scale has created super aggressive benefits (in addition to highly effective money flows for innovation although analysis and improvement), and can assist the corporate proceed to achieve the years forward.

Amazon Dangers:

Market Cycle: Amazon faces dangers. For starters, the market was upset by Amazon’s most up-to-date quarterly earnings announcement (whereby the shares bought off sharply) stemming from slower development than anticipated in AWS because the aftereffects of pandemic-driven social distancing (and make money working from home) proceed to put on off). What’s extra, this unfavorable pattern might proceed as general financial development has slowed and the potential for an unsightly recession continues to loom. Moreover, there are reviews that Amazon is ready to put off as much as 20,000 staff (a current pattern amongst giant technology-driven corporations) within the coming months; that is encouraging from a proactive cost-control standpoint, however regarding, and indicative of probably tough roads forward.

Overseas Foreign money: One other threat is overseas foreign money results whereby earnings have lately been impacted negatively by unfavorable translation results. The various diploma and tempo of post-pandemic financial coverage shifts and lockdown insurance policies have contributed to a dynamic overseas foreign money threat atmosphere.

Regulation: Regulatory pressures are one other threat for Amazon. Specifically, “huge tech” corporations (together with Amazon) face rising pressures over anti-competitive practices in addition to information privateness points. For instance, in 2021 Amazon acquired a document $888 million EU tremendous over information violations. Regulatory pressures are a relentless threat for Amazon.

Cloud Competitors from Microsoft (which is gaining floor on AWS) and Google are additionally a threat. Nonetheless, given the dimensions of the large cloud secular trend-there is room for a number of huge gamers to succeed, and cloud will doubtless be a number one profit-driver for the following decade at the very least.

Valuation:

Do not be fooled by Amazon’s low web revenue margins (see desk beneath). It’s largely a high-sales low-net-margin retail enterprise. And this huge income retail enterprise creates huge financial moats and community results that strengthen its different worthwhile high-growth operations (AWS, subscriptions, and promoting).

Presently buying and selling at below 2 occasions gross sales (the decrease finish of its historic vary), and with income anticipated to develop (and continue to grow) at roughly double digits (based mostly on huge long-term secular developments), Amazon is extraordinarily attractive-despite the truth that it is rising at a barely slower tempo than most analysts had beforehand anticipated (as they over-extrapolated the short-term “pandemic bump”). Additionally vital to notice, Amazon spends closely on analysis and improvement, a price that may be decreased anytime to extend revenue, however stays vital for future development.

Inventory Rover, information as of 30-Dec-22

Moreover, the Fed’s aggressive rate of interest hikes this 12 months have had a very unfavorable influence of high-growth shares (see efficiency within the tables above). We consider these components assist clarify the share worth declines, and in addition contribute to the attractiveness of the funding alternative as inflation will ultimately gradual, the Fed’s aggressively hawkish insurance policies will average (hopefully ahead of later), and Amazon will continue to grow quickly for a few years.

Conclusion

Development shares, together with Amazon (down ~50% in 2022) have been hit significantly onerous by quickly rising rates of interest. And as we wrote in our new 2023 Outlook: 10 Shares Price Contemplating:

We may very well be within the very early innings of a brand new long-term market paradigm whereby near-zero rates of interest are gone for many years and so too stands out as the unimaginable management and efficiency of development shares.

That stated, lots of the high-growth pandemic darlings which have already fallen so onerous, should have additional to fall as greater rates of interest have pushed profitability additional into the long run (and possibly by no means).

Amazon, nevertheless, is without doubt one of the choose development inventory leaders that’s already worthwhile and has the monetary wherewithal to sidestep the numerous capital market challenges that many (unprofitable) development shares will doubtless succumb to within the years forward. We do not know the place the market will likely be subsequent week, subsequent month or on the finish of 2023, however over the long-term Amazon (and choose financially-strong growth-stock leaders) will doubtless be buying and selling dramatically greater.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a significant U.S. change. Please pay attention to the dangers related to these shares.