: 000 Investment In 1992 Grew To Over Million – It Can Repeat")

monticelllo

Introduction

It is time to talk about a inventory I’ve by no means mentioned on In search of Alpha – or anyplace else.

Because the title already gave away, that firm is the Starbucks Company (NASDAQ:SBUX), an organization I’ve averted as a result of I’m not a giant fan of client shares, which turned out to be an enormous mistake!

I consider my dislike of espresso and fancy drinks performed a minor position as effectively.

That mentioned, lots of people love SBUX, which has resulted in huge positive aspects.

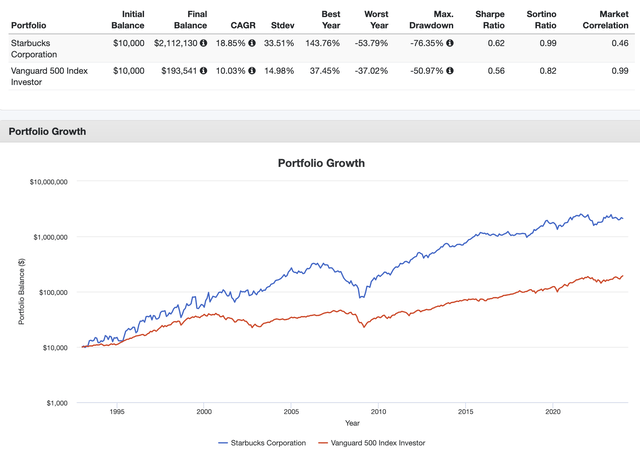

Traders who put $10,000 into Starbucks on the final buying and selling day of 1992 are at present sitting on $2.1 million, together with dividends.

Portfolio Visualizer

This huge return is offered by a compounding annual progress fee of 18.6% throughout this era, which beats the S&P 500’s 10.0% return by a large margin.

Even adjusted for volatility, the inventory had a greater risk-adjusted return than the market (Sharpe/Sortino Ratios).

On this article, I am going to deal with how Starbucks is rising, what to make of its working atmosphere, and why it is nonetheless a fantastic inventory to construct important wealth – in any case, the bullish title is not clickbait.

So, let’s get to it!

The Return Of Confidence May Unlock Enormous Positive aspects

Since October 2003, SBUX has returned 13.8%. That is beneath the long-term annual complete return of 18.6% however nonetheless sufficient to generate super wealth.

To provide you just a few examples:

- In case you discover an funding that may return 13.8% per yr over the following ten years, you may flip $10,000 into $36,400.

- In case you hold this funding for 20 years, that quantity turns into $132,700.

- In case you hold this funding for 40 years, you may generate $1.8 million!

Even higher:

- In case you determine a possible high-flying inventory and purchase it beneath “honest” worth, you may generate considerably greater returns.

- You want simply 32.94 years to show $10,000 into 1,000,000 in the event you discover a 15% CAGR alternative. Once more, 32.94 years might appear to be lots. Nevertheless, $10,000 is not lots. In my nation, that does not even purchase you an entry mannequin of a Japanese/Korean automotive firm.

- $20,000 turns into $1 million after simply 28 years of 15% returns.

With all of this mentioned, on paper, it is easy to get wealthy. Very simple.

It is tougher to seek out good alternatives and put precise cash to work.

That is the place Starbucks is available in.

What I like about Starbucks is that it’s a high-flying progress at a really engaging worth.

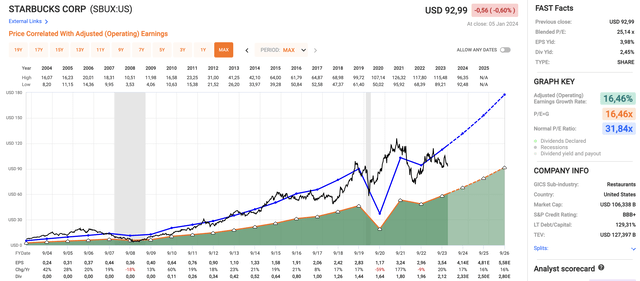

Utilizing the info within the chart beneath, SBUX is anticipated to develop its EPS by 17% in FY2024, and 16% in each FY2025 and FY2026.

Going again to 2003, the normalized valuation of SBUX was 31.8x. This quantity was absolutely justified by elevated progress.

Nevertheless, regardless of the outlook of constant double-digit EPS progress, the corporate is now buying and selling at a blended P/E ratio of simply 25.1x.

FAST Graphs

Based mostly on these numbers:

- Purely theoretically, if the inventory had been to see a valuation shift to 31.8x, it may return 28.5% per yr via FY2026. Once more, that is purely theoretical.

- Nevertheless, even a 24x a number of (beneath its present valuation) may indicate a 17% annual return going ahead.

To place it merely, if we are able to show that SBUX continues to be performing strongly and if we are able to perceive why, it has carried out poorly for the reason that pandemic, we are able to argue that it presents a extremely interesting alternative for long-term dividend progress.

Nevertheless, earlier than we dive into that, let’s check out its dividend.

The SBUX Dividend

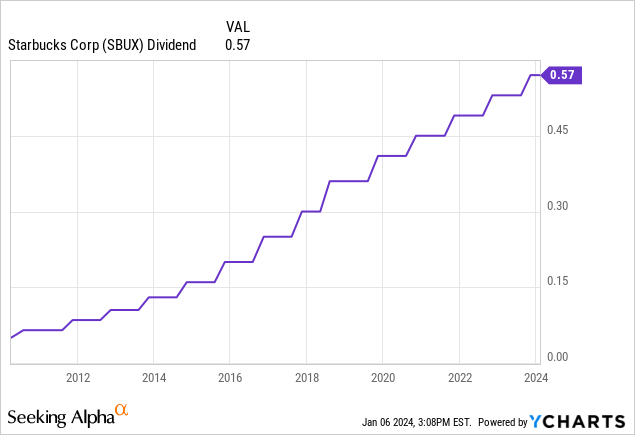

One of the engaging issues about SBUX is its dividend. The present quarterly dividend is $0.57 per share, which interprets to a yield of two.5%.

- The S&P 500 yields 1.4%.

- The Vanguard Dividend Appreciation Index Fund ETF Shares (VIG) yields 1.9%.

On September 20, 2023, Starbucks hiked its dividend by 7.5%. The five-year dividend CAGR is 10.4%.

This yr, the corporate is anticipated to generate $4.14 in EPS, which interprets to an earnings payout ratio of 55%, which may be very wholesome.

Even higher, the corporate has a web leverage ratio of lower than 2.0x EBITDA and a BBB+ credit standing, one step beneath the A variety.

The corporate has hiked its dividend each single yr since its initiation in 2010.

With that mentioned, let’s take a more in-depth have a look at the larger image to learn how sustainable the corporate’s progress is.

Regardless of Headwinds, SBUX Is Poised For Sturdy Progress

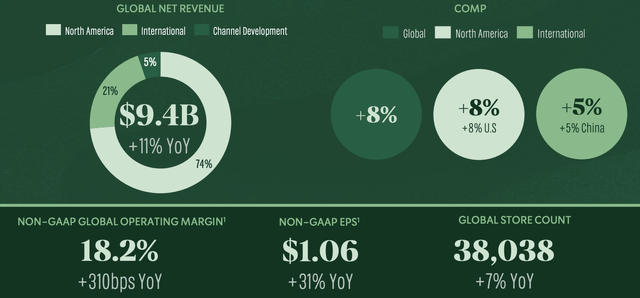

In its most up-to-date quarter, 4Q23, the corporate skilled sturdy progress, with consolidated income up 9% to $9.4 billion.

The U.S. enterprise delivered record-breaking common weekly gross sales, resulting in an 8% comparable retailer gross sales progress globally.

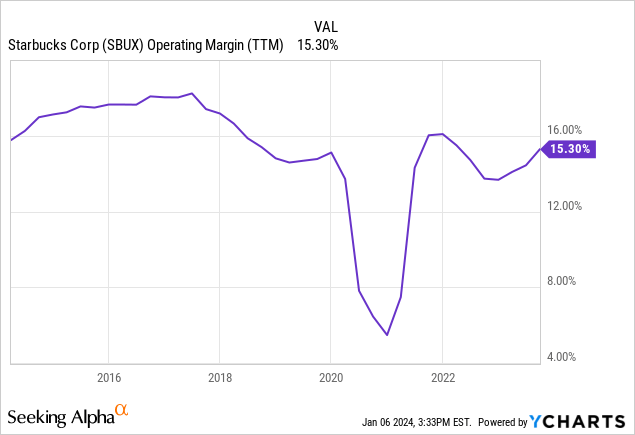

This fall consolidated working margin expanded by 310 foundation factors to 18.2%, surpassing expectations.

Starbucks Company

The Worldwide section delivered $2 billion in This fall income, up 11% from the prior yr.

China performed a major position, contributing to double-digit progress and surpassing 20,000 shops. China’s income in This fall grew by double digits, pushed by new shops and 5% comparable retailer gross sales progress.

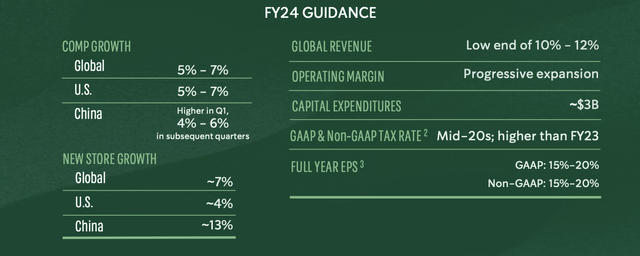

Throughout its 4Q23 earnings name, the corporate outlined strategic and optimistic steering for fiscal yr 2024. The corporate expects international comparable gross sales progress within the vary of 5% to 7%, reflecting a shift from the prior yr’s steering of seven% to 9%.

The U.S. comparable retailer gross sales are projected to develop between 5% and seven%, constructing on the sturdy efficiency of 9% comp progress in fiscal yr 2023.

The corporate forecasts consolidated income progress within the vary of 10% to 12% for fiscal yr 2024, albeit on the low finish of the vary.

Starbucks Company

Whereas this steering is sweet, the corporate’s lower-than-expected comparable retailer gross sales steering is the results of financial headwinds.

Throughout final month’s Morgan Stanley World Client & Retail Convention, the corporate elaborated on a few of these headwinds.

For instance, the corporate acknowledged that the restoration in China is slower than anticipated, reflecting broader financial challenges. Whereas expressing confidence within the long-term energy of the Chinese language market, the speedy future is seen as uneven, marked by uncertainties and a extra promotional atmosphere.

That is no shock, because the Chinese language financial system is beneath super stress.

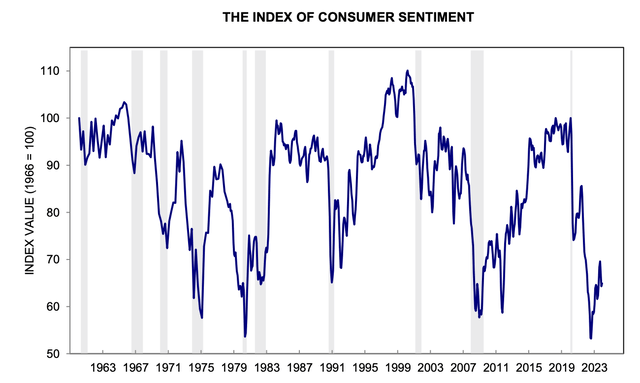

Additionally, that is what client confidence within the U.S. seems to be like:

College of Michigan

On prime of that, geopolitical tensions and conflicts in sure worldwide markets pose challenges.

The corporate acknowledged the impression of geopolitical dynamics on its operations, particularly in areas affected by conflicts. This provides a component of unpredictability to the worldwide enlargement technique, particularly as a result of it’s hit by boycotts of sure political teams (for lack of a greater phrase) in some international locations.

Moreover, whereas enhancements have been made within the provide chain, the corporate has skilled disruptions and challenges.

The necessity to constantly optimize provide chain processes, particularly with the introduction of latest tools and know-how, stays an ongoing focus.

The excellent news is that working margins have stabilized, with the corporate seeing “progressive enlargement” in 2024.

Based mostly on this context, SBUX is closely investing in progress, which may leverage each margins and earnings progress the second cyclical challenges begin to fade.

For instance, throughout the identical convention, the corporate talked about that it has seen success in its present digital run charges and is present process a change in its strategy to digital innovation.

This includes extra frequent releases, with conferences each six weeks to evaluate progress and plan future developments.

Starbucks goals to leverage its present buyer base of over 300 million folks globally, together with 75 million Starbucks Rewards members, to drive extra enterprise into its shops.

The corporate can also be actively participating in partnerships with key business gamers comparable to Microsoft (MSFT), Apple (AAPL), Delta (DAL), and Amazon (AMZN).

FOX Enterprise

These partnerships are strategic in enhancing the digital expertise, providing particular advantages to prospects, and growing the worth proposition for Starbucks loyal.

On prime of that, it’s engaged on new partnerships in different areas.

One other factor I am enthusiastic about (it may get me to go to its shops extra typically) is that SBUX sees untapped potential within the PM daypart, particularly within the beverage and meals segments.

The corporate goals to carry focused and revolutionary merchandise to the PM daypart, capitalizing on its present retailer footprint and the capability to fulfill buyer demand.

Basically, the corporate sees alternatives for progress in each beverage and meals gross sales in the course of the afternoon, with a deal with customization, digital engagement, and attachment to drinks.

Though I’d not evaluate this to McDonald’s (MCD) providing all-day breakfast, it appears to be a really promising improvement.

Thus far, the corporate has noticed excessive attachment charges, particularly within the U.S., with two out of 5 prospects attaching meals to their orders.

However wait, there’s extra!

The corporate sees substantial potential in worldwide markets, notably in areas like Latin America, Continental Europe, Southeast Asia, India, the Center East, and Africa.

With a deal with constructing a worldwide community via digital options, there’s an emphasis on tapping into numerous markets the place espresso tradition is rising.

With regard to the aforementioned Chinese language developments, regardless of present challenges and a slower restoration fee in China, the corporate views it as a important market with long-term progress prospects.

Premium manufacturers, Starbucks and Reserve, are well-regarded, and there is room for additional penetration in cities.

Starbucks Company

Talking of headwinds, the corporate can also be actively addressing the provision chain points I discussed on this article.

The corporate has a $3 billion productiveness program, with 70% allotted exterior the shop, which presents a possibility for steady enchancment and price effectivity.

This consists of optimizing provide chain administration, procurement, and companies globally.

Backside Line

All issues thought of, there are explanation why SBUX is buying and selling beneath its historic, “regular” valuation.

- Financial progress is weakening, whereas the patron is in a troublesome spot.

- It’s nonetheless coping with provide disruptions and margin compression.

- Strikes brought on by labor points and geopolitical developments aren’t serving to, both.

Nevertheless, the corporate’s progress expectations are excessive. Whereas 2024 could also be considerably of an underwhelming yr, we’re nonetheless speaking about elevated EPS progress expectations.

On prime of that, investments in progress ought to hold future progress excessive and buyer satisfaction elevated.

Therefore, I consider the corporate will proceed to persistently develop its dividend and revel in elevated capital positive aspects, making it a fantastic long-term funding.

I’m contemplating shopping for the inventory for my portfolio this yr, as I’m massively underweight client shares.

Because the title prompt, I’ve excessive hopes for SBUX and consider it’ll proceed to generate super wealth for its shareholders for a few years to return.