iambuff/iStock by way of Getty Photographs

Thesis

It’s no secret that early-stage progress tech shares have suffered main losses through the market rotation that began in late 2021. Fastly, Inc. (NYSE:FSLY), an edge cloud platform supplier, is among the corporations which have misplaced essentially the most as buyers have grown skeptical about slowing progress potential and lack of income. On this evaluation, I look into the present monetary state of the corporate, in addition to whether or not a valuation case might be made, given the great inventory worth retreat the corporate has seen over the previous few months.

Inventory worth efficiency

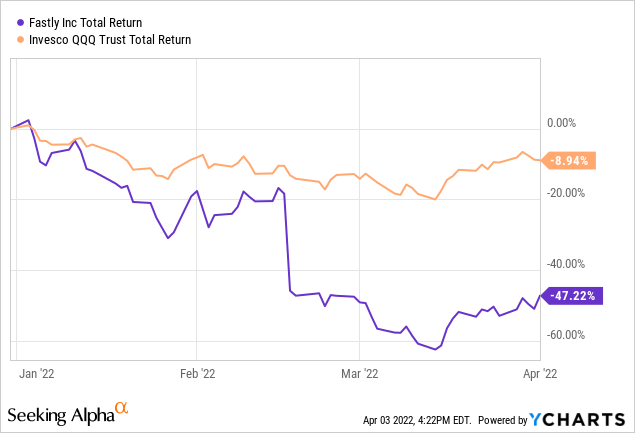

Over the previous six months Fastly’s has marked an enormous retreat in inventory worth. Down greater than -47% YTD and -80% from 52-week highs, many buyers are dropping hope. Whereas the broader market has seen some momentous turmoil, Fastly is considerably underperforming as retail and institutional buyers flip away from the pandemic-hyped shares to hunt shelter in established, cash-flow producing corporations. Presently, Fastly trades at $13 per share, with a $2.25B market cap.

The enterprise

Previously referred to as Skycache, the corporate modified its title to Fastly, Inc. in Might 2012. Fastly operates an edge cloud infrastructure platform that allows builders to construct safe and ship digital experiences with pace. The corporate makes use of the performance of the Content material Supply Community, a geographically distributed community of proxy facilities and information facilities that primarily decentralizes information availability and efficiency, nearer to the end-user. Serving clients in digital publishing, on-line retail, leisure, hospitality, monetary providers and different sectors the corporate, Fastly is a extremely regarded vendor of CDN know-how.

In latest information, the corporate has accomplished the acquisition of Fanout, a platform that allows the real-time constructing and scaling of APIs akin to reside chat help, eCommerce, video streaming, gaming, collaborative modifying, and extra of APIs on March 20, 2022. By way of the transaction, the corporate appears to be like to broaden its progress technique to determine and deploy applied sciences that improve efficiency, safety and innovation for patrons.

Monetary efficiency

Fastly has posted a good progress report over the previous couple of years. Income has grown at a 4-year CAGR of 35%, from $105M in 2017 to $354M in 2020, with the corporate sustaining sturdy gross margins, above 50%. During the last 12 months, nevertheless, progress appears to be slowing, as Fastly elevated income from 2020 to 2021 at a 22% YoY charge. The dearth of total profitability solely provides to the record of considerations, with the corporate posting greater losses in 2021 in comparison with the earlier 12 months, and never anticipating to achieve a optimistic internet outcome any time quickly.

The slowdown in income progress can also be obvious when inspecting analysts’ outlooks over the following few years. Anticipated to develop at a CAGR of 16% by 2024, forecasted income will increase appear unimpressive, contemplating the urgent want the corporate has to generate income. With $561M in gross sales projected for the 2024 fiscal 12 months, Fastly will nonetheless be in need of reaching a optimistic internet outcome, because the EPS estimate for a similar years at present appears to be like for -$0.32 per share.

In search of Alpha

Though somebody may argue {that a} 16% CAGR near-term progress outlook can’t be presumably thought of a bearish signal, I’d counter that an early growth-stage, disruptive firm within the cloud providers trade ought to show higher potential. In spite of everything, the know-how sector, closely weighted in direction of mature and established corporations like Apple (AAPL), Microsoft (MSFT) and Google (GOOG). Fastly has grown extra aggressively, at larger charges, and is predicted to proceed to take action.

Dilution is one other menace dealing with stockholders. Fastly has aggressively elevated its share rely from 23M in 2017 to 116M on the finish of 2021, seeking to cowl mounting losses. Shareholders worry additional dilution is approaching, questioning the administration’s technique, hurting their returns and possession claims.

Stability sheet

Extra considerations appear to come up when taking a better take a look at the corporate’s stability sheet. Fastly’s long-term debt stability has considerably elevated, amounting now to 900M or 40% of the corporate’s market cap. Whereas at this degree of leverage many buyers aren’t notably involved, comparable corporations within the know-how sector are recognized for borrowing significantly much less. Coupled with aggressive shareholder dilution, it’s turning into clear that the battle to turn into worthwhile is severely impacting long-term survivability. Liquidity then again seems sturdy as Fastly carries a cushty 4.74 present ratio and a 4.49 fast ratio.

Valuation

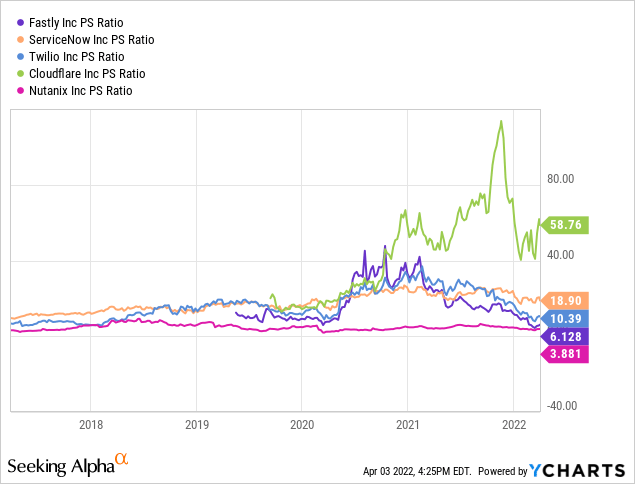

With the inventory recording an enormous pullback over the previous months, stockholders in search of a silver lining to encourage them to carry on to their place, together with potential buyers inspecting the attractiveness of an extended place at present worth ranges, may rotate their focus in direction of valuation. Regardless of the worth retreat, nevertheless, with the corporate nonetheless at a 6x P/S a number of, it’s arduous to see how Fastly may current a price alternative until the corporate’s progress outlook drastically modifications and profitability struggles fade. Whereas a P/B ratio of 1.92x may point out that the inventory in all fairness valued, it is very important observe that this specific metric is ineffective in valuing corporations within the cloud service trade which can be notoriously asset-light.

Alternatively, when having a look at P/S multiples throughout totally different corporations working within the cloud area, at 6x gross sales it may even be argued that Fastly is buying and selling at an inexpensive valuation. Nevertheless, a lot of the comparable corporations portrayed on this evaluation keep stronger progress outlooks or bettering profitability metrics and encourage buyers in that sense to pay a better premium.

Last Ideas

In spite of everything issues are thought of, I nonetheless discover it arduous to embrace a bullish outlook for Fastly, regardless of the numerous drop within the inventory worth, which ought to in principle make the inventory extra enticing, a minimum of on a valuation foundation. Profitability struggles, growing leverage, shareholder dilution, and an underwhelming progress outlook ought to maintain a extra conservative investor from contemplating including Fastly to a portfolio.