Inventory markets provide one of many nice paradoxes of life – that when circumstances develop troublesome and costs fall, alternatives for revenue will seem. For buyers, it’s an opportunity to money in – after a correct look into the nuts and bolts behind a market decline. As all the time with shares, knowledgeable selections are the more than likely to pan out.

To jumpstart that due diligence, we are able to test in with Wall Avenue’s analysts. These are the professionals, the fairness specialists who’ve constructed their reputations studying and analyzing the internal workings of the buying and selling surroundings, and their revealed notes and proposals give the investing public a sound information to worthwhile investments.

Utilizing their insights and the TipRanks database, we’ve recognized a number of shares which can be primed for good points – however are priced low for now. These are Purchase-rated equities which have fallen on onerous occasions – with over 60% losses up to now yr – however in response to the analysts, they nonetheless provide triple-digit upside potential. Let’s take a better look.

Plug Energy (PLUG)

First on our checklist is Plug Energy, a ‘inexperienced energy’ participant designing and manufacturing zero-emission hydrogen gas cell programs, together with the manufacturing, storage, and supply infrastructure wanted to construct out this new expertise to industrial or utility scales. Hydrogen gas cells use electrochemical reactions to generate usable electrical energy. The result’s a cleaner energy supply, primarily based on clear, renewable hydrogen – the commonest factor within the universe.

Plug Energy’s hydrogen gas cell battery merchandise have discovered makes use of in each motive and stationary purposes, together with backup energy technology and in warehousing. The gas cells are rising in reputation with information facilities, and have been discovered to be cost-effective in warehousing, the place they’re used to energy pallet jacks and fork lifts. Different purposes embody dwelling heating programs and moveable electronics. Up to now, Plug has deployed greater than 60,000 energy cells for e-mobility, and has grow to be the most important purchaser of liquid hydrogen in North America. The corporate’s buyer base consists of names akin to Amazon, Walmart, and BMW.

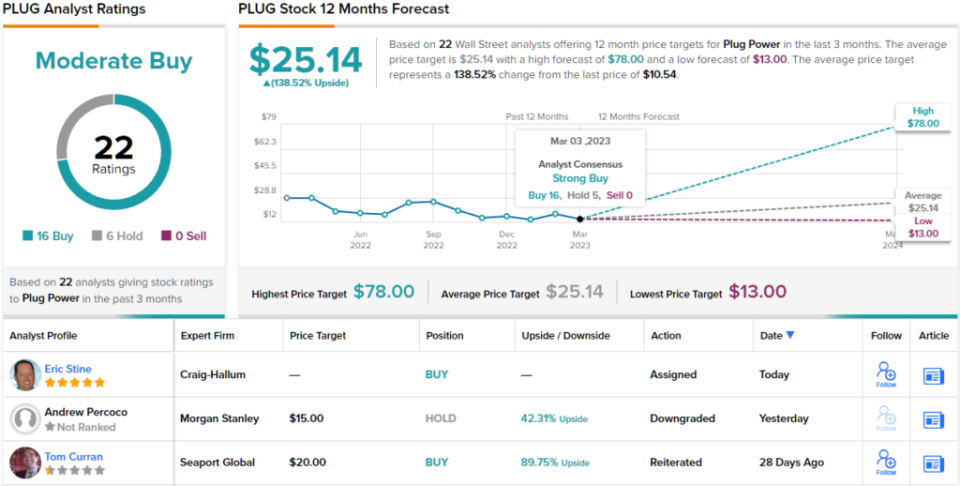

The long-term prospects for Plug look good. In at the moment’s cultural surroundings, which locations a premium on each clear and renewable power sources, Plug may be positive of discovering each political and social help. Brief-term, nevertheless, the image is much less rosy, and PLUG shares are down 67% over the past 12 months.

At the very least a part of the rationale may be seen in Plug’s latest quarterly earnings reviews. The corporate is solely not hitting the income expectations. Within the final report, from 4Q22, Plug reported a prime line of $221 million – that was up 36% year-over-year, but it surely missed the $277.3 million forecast by a 20% margin. Worse, the corporate’s annual web diluted EPS loss worsened y/y, from -$0.82 cents to -$1.25.

On a optimistic notice, Plug does have loads of enterprise lined up going ahead. The corporate got here out of 2022 with a stable backlog of labor, in each the hydrogen manufacturing electrolyzer enterprise and in hydrogen liquefaction orders.

The backlog and the prospect for continued orders increase momentum going ahead type the bottom for Wolfe analyst Steve Fleishman’s optimistic view of this inventory.

“Plug closed 2022 with a miss on income however noticed its backlog soar 27% within the quarter on growing demand for electrolyzers, gas cells, and liquefiers. We see numerous optimistic momentum to return over 2023 for PLUG as hydrogen funding rises and there may be extra readability on the IRA incentives and hydrogen hubs, although execution might be key this yr,” Fleishman opined.

Anticipating that Plug will be capable of execute, Fleishman charges the shares as Outperform (i.e. Purchase) and units a worth goal of $25, suggesting a one-year upside of ~138%. (To look at Fleishman’s monitor file, click on right here)

General, Plug has been producing loads of buzz, and has 22 evaluations from the Avenue’s analysts. These embody 16 Purchase suggestions and 6 Holds, for a Reasonable Purchase consensus ranking. General, the Avenue sees a formidable 138% upside potential right here, primarily based on the common worth goal of $25.14. (See PLUG inventory forecast)

Adicet Bio (ACET)

Subsequent on our checklist is Adicet Bio, a small-cap agency within the biopharmaceutical sector. Adicet is engaged on a brand new line of ‘off the shelf’ T cell therapies for most cancers therapy, primarily based on allogenic gamma delta T cells. These characterize a brand new technology of T cells, when in comparison with the present alpha beta T cell immunotherapies, and provide the promise of larger efficacy in antitumor exercise in opposition to each stable tumors and hematological cancers. The corporate is producing its line of gamma delta T cell drug candidates by way of a proprietary cell platform.

Adicet is at the moment within the transition from the pre-clinical stage to the human medical trial stage. The corporate’s pipeline has a number of analysis tracks ongoing, together with 5 at the moment in discovery/preclinical testing, two on the IND-enabling regulatory stage, and one in a Section 1 human medical trial.

That medical trial is the first issue for buyers to contemplate on this inventory. The drug candidate, ADI-001, is below investigation within the therapy of relapsed or refractory B-cell non-Hodgkin’s lymphoma, in an ongoing Section 1 examine. The drug obtained the FDA’s Quick Monitor designation final yr, and in This fall Adicet launched interim information on security and efficacy.

The launched information confirmed a ‘favorable’ security and tolerability profile in any respect dose ranges, in addition to a 75% total response price (ORR) and a 69% full response (CR) throughout all dose ranges. The corporate is at the moment persevering with enrollment within the trial, with the aim of acquiring further information on sturdiness of response in help of a deliberate Section 2 dose. Further updates are anticipated in 2Q23.

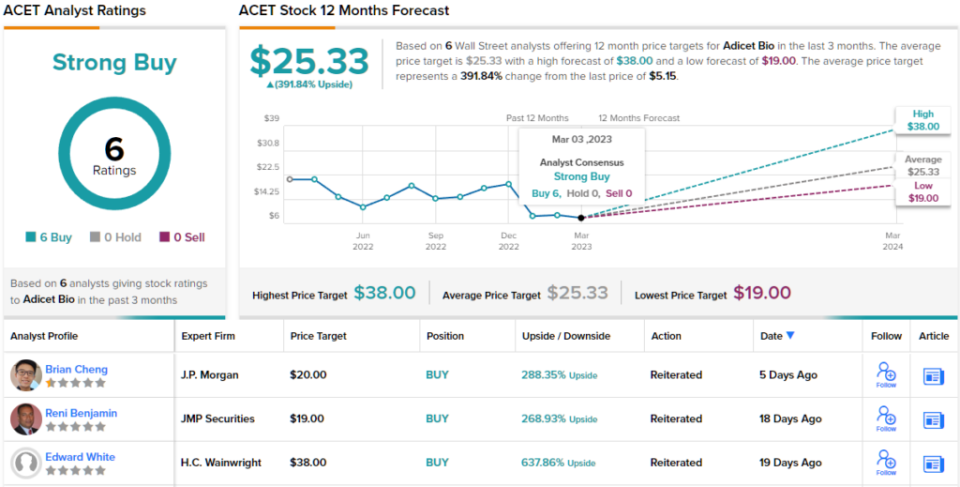

Whereas these information had been optimistic, the corporate’s inventory fell sharply after the outcomes had been launched. Considerations had been raised over the six-month full response price, as the info confirmed a whole response price for dose ranges 2 and three of simply 33%. The corporate plans to deal with these points with the dose degree 4 course of underway. Within the meantime, shares in ACET are down 74% for the previous 12 months.

Regardless of the issues over the sturdiness problems with ACI-001, Wedbush analyst Robert Driscoll stays upbeat on Adicet by way of the remainder of this yr. Explaining his place, Driscoll says, “We proceed to imagine the info stay spectacular with an ORR of 75% included a putting 5/5 CRs in LBCL sufferers who relapsed after prior CD19 CAR-T remedy, and count on longer-term sturdiness information from further dose cohorts will present higher perception into potential sturdiness. We see ACET’s platform as considerably differentiated, and see vital upside potential for shares over the following 12–18 months as applications progress.”

This justifies the Outperform (i.e. Purchase) ranking, in Driscoll’s view, and the analyst’s $30 worth goal signifies his confidence in a hefty 482% upside for the following 12 months. (To look at Driscoll’s monitor file, click on right here)

General, with 6 latest analyst evaluations, all optimistic, Adicet’s inventory has earned its Robust Purchase consensus ranking. The shares are buying and selling for $5.21 and the common worth goal, which stands at $25.33, suggests a formidable acquire of ~392% mendacity forward. (See ACET inventory forecast)

Design Therapeutics (DSGN)

For the final inventory on our checklist, we’ll follow the biotech sector. Design Therapeutics, one other research-oriented biopharma, is targeted on discovering disease-modifying remedies that focus on underlying causes of inherited nucleotide repeat growth circumstances. In brief, the corporate is growing new therapeutic brokers for genetically-based degenerative illnesses with excessive unmet medical wants.

Design’s strategy is predicated on gene focused chimeras (GeneTACs), forming the bottom of small-molecule genomic medicinal brokers. These novel drug candidates work by modifying the faulty inherited nucleotides that underlie the focused circumstances.

The corporate’s analysis pipeline at the moment options three tracks, two of that are attracting investor consideration. Essentially the most superior, on the Section 1/2 medical stage, is drug candidate DT-216, a possible therapy for Friedreich Ataxia. The Section 1 stage of the trial is ongoing, evaluating grownup sufferers to construct a profile on security, tolerability, pharmacokinetics, biodistribution, and pharmacodynamic results, all primarily based on three weekly doses. Earlier outcomes, primarily based on the single-ascending dose (SAD) portion of the trial confirmed that DT-216 was typically well-tolerated; outcomes from a a number of ascending dose (MAD) portion are anticipated by the center of this yr, and the Section 2 portion of the trial is deliberate for initiation in 2H23.

In one other growth of notice to buyers, the corporate’s second drug candidate, DT-168, stays on monitor for a Investigational New Drug (IND) submission in 2H23. This is a vital regulatory milestone, and approval will clear the best way for human medical trials. DT-168 is a possible therapy for the genetic eye illness Fuchs Endothelial Corneal Dystrophy, or FECD.

Regardless of the optimistic place of the corporate’s analysis applications, shares in DSGN are down by 68% up to now yr.

That mentioned, RBC analyst Leonid Timashev takes a bullish stance on the corporate and believes the shares will push forward from right here.

“The crew continues to execute on DT-216, with this system nonetheless on monitor for information mid-year and a ph.II begin in 2H23. Moreover, we notice the corporate continues to maintain prices below management whereas progressing lead program DT-216 by way of ph.I MAD work and two further geneTACs in the direction of the clinic. With shares having pulled again following the December SAD uptake, we imagine buyers are undervaluing the demonstrated proof of precept, and we search for further validation as this system progresses by way of MAD and ph.II to assist shares get well,” Timashev opined.

These feedback again up Timashev’s Outperform (i.e. Purchase) ranking and he has set the one-year worth goal at $24, implying a acquire of ~340% in that point. (To look at Timashev’s monitor file, click on right here)

Wanting on the consensus breakdown, different analysts are on the identical web page. With 4 Buys and no Holds or Sells, the phrase on the Avenue is that DSGN is a Robust Purchase. DSGN shares are priced at $5.46 and their $27 common goal implies a whopping 394% acquire within the subsequent 12 months. (See DSGN inventory forecast)

To seek out good concepts for shares buying and selling at engaging valuations, go to TipRanks’ Finest Shares to Purchase, a newly launched instrument that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is extremely vital to do your personal evaluation earlier than making any funding.