[ad_1]

Picture credit: Sprinque

Amsterdam-based Sprinque, a versatile funds platform for native and cross-border B2B transactions, introduced on Tuesday that it has secured €20M debt facility from Avellinia Capital.

The announcement comes 5 months after elevating €6M in a Seed spherical of funding led by Join Ventures.

Sprinque says it’ll use the funds to help B2B e-commerce retailers who promote Pay-by-Bill to companies.

The debt facility will even allow the Dutch firm to finance roughly €200M in transactions yearly.

The investor

Avellinia Capital is a non-public credit score funding supervisor offering tailored and versatile asset-based financing options to fast-growing specialty lenders and specialty finance originators.

In a dialog with Silicon Canals, Mark Holleman, co-founder and CPO of Sprinque, shares his insights on persuading Avellinia Capital.

“We had labored with completely different lenders earlier than assembly the Avellinia Capital workforce. After we first met them, Avellinia Capital and Sprinque clicked instantly,” says Holleman.

“We each consider within the potential of the B2B market. The Avellinia Capital workforce understood that their method to working with us have to be versatile and open-minded, and so they liked the Sprinque workforce,” provides Holleman.

Versatile B2B fee platform

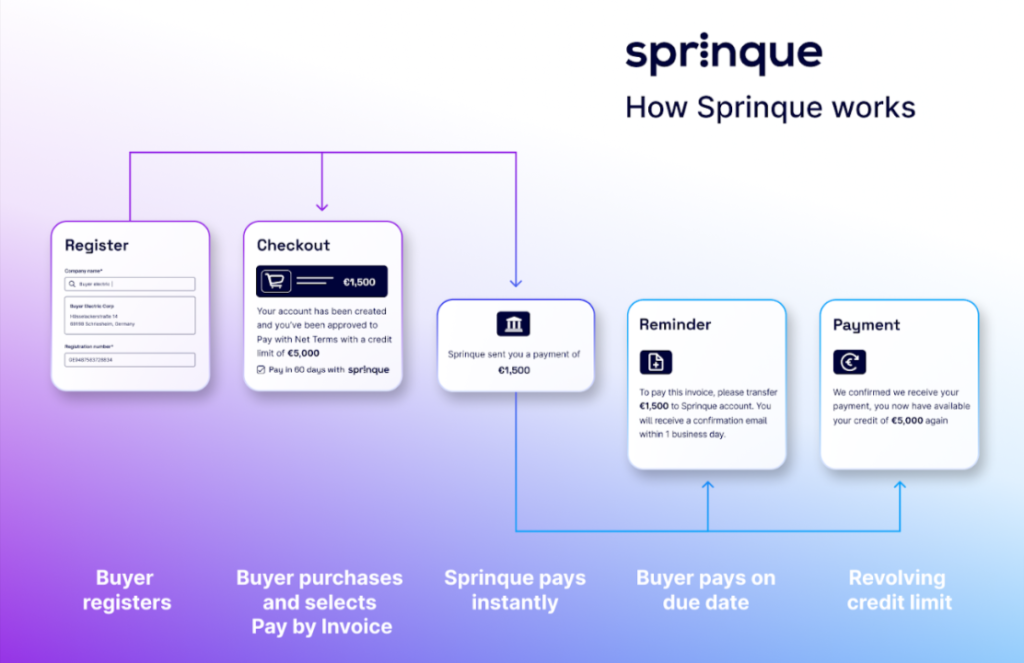

Manoj Tutika (CTO), Mark Holleman (CPO), and Juan Espinosa (CEO) based Sprinque in February 2021. It allows B2B retailers and B2B marketplaces to increase fee phrases to their clients, with the choice to pay 15-90 days later with out further danger or operational overhead.

The inspiration for Sprinque got here from Holleman’s time constructing BNPL experiences for Amazon’s marketplaces in Europe. He realised that constructing such experiences for all of Europe is advanced and dear and that B2B is a massively underserved phase relating to enabling frictionless transactions, on-line and offline.

What makes Sprinque stand out?

“Our focus from the beginning has been on constructing a pan-European platform that goals to go world. We didn’t wish to construct an area resolution and keep an area participant,” Holleman tells Silicon Canals.

“The true alternative exists round cross-border transactions, and this can be a downside price fixing, to contribute to fulfilling the potential of the borderless European market,” he provides.

Sprinque has retailers within the Netherlands, Belgium, Germany, Sweden, the UK, France, and Spain, with consumers throughout Europe and past.

He says, “One other differentiator is that our platform was constructed particularly for B2B buying flows, which are sometimes fairly completely different from B2C e-commerce. With our platform and our APIs, we will help any buying stream, whether or not it’s real-time decisioning in a web based checkout or a gated setting or a quote-to-cash course of.”

Quick and pleasant purchaser buying expertise

Holleman says the method of making use of for Pay-by-Bill companies has not been very accommodating in the direction of companies, particularly when contemplating time sensitivity.

Sprinque addresses this by verifying companies and making fraud and credit score selections in seconds.

“We leverage a broad set of information sources, from conventional credit score bureaus to various knowledge sources, to make these selections in actual time,” provides Holleman.

He additional states, “Additionally, we by no means reject companies outright; if for some cause a purchaser is just not profitable in getting a credit score restrict assigned robotically, they at all times find yourself in our handbook evaluation course of the place we take a more in-depth take a look at the enterprise earlier than making a ultimate resolution. As we study and our danger engine will get smarter, the share of companies ending up in handbook evaluation decreases.”

Sprinque additionally claims to tackle all default dangers for accredited transactions.

Holleman says, “Sprinque takes on all fraud and credit score defaults, which implies retailers can ‘Promote & Overlook’. As soon as we approve a purchaser and an order, from that second onwards, the service provider doesn’t want to fret about if, when and the way they may receives a commission.”

Growing a pan-European financing community

The Amsterdam firm constructed a devoted Particular Function Car (SPV) construction with Collections Foundations for his or her service provider financing companies.

Sprinque claims that this construction is the primary constructing block for a pan-European financing community that can help B2B retailers throughout all European international locations shortly.

“All service provider settlements and all bill funds from consumers stream by way of the Assortment Basis (Stichting Sprinque),” says Holleman.

“Because of this we will add a number of Particular Function Autos behind Stichting Sprinque, with out impacting how we settle to retailers or how consumers pay their invoices. This enables us to simply add SPVs in our construction for brand new markets or lenders,” he tells Silicon Canals.

Mitigating financial pressures

The corporate’s Pay-by-Bill resolution goals to assist companies mitigate financial pressures by way of dynamic settlements.

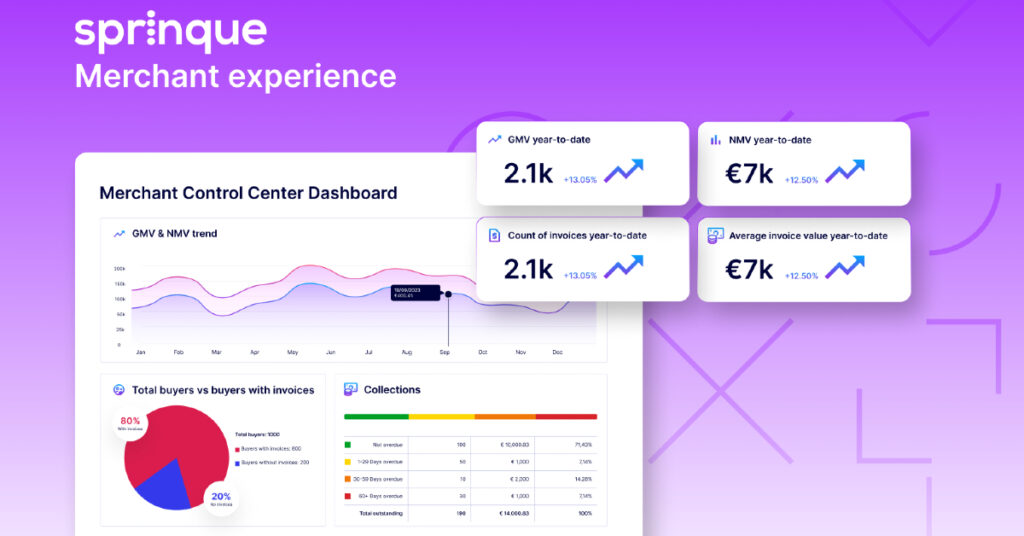

“Retailers can resolve precisely after they wish to be paid for an order. This helps retailers optimise their working capital wants, whereas solely paying financing prices for the financing they want,” Holleman says.

The debt facility affords extra liquidity to present and future B2B retailers who promote on Pay-by-Bill with web fee phrases of seven, 15, 30, 45, 60, or 90 days, in addition to various choices for Pay-in-Instalments.

“With a static settlement framework, retailers will at all times receives a commission the identical variety of days after an order has been positioned or an bill has been issued, no matter whether or not they want the financing for that order/bill, or not. And retailers need to pay for this service, even when they don’t want it,” says Holleman.

Roadmap for 2023

With a present acceptance price of 90%+, Sprinque goals to maintain Pay-by-Bill methods as frictionless as attainable by dealing with the method from end-to-end on behalf of retailers.

It contains onboarding and verifying the enterprise purchaser, setting and managing the credit score restrict for accredited enterprise consumers, settling the transaction with the service provider of their most popular forex, and accumulating bill fee from the enterprise purchaser as soon as the bill falls due.

“Essentially the most formidable upcoming improvement is our growth outdoors of Europe, to assist US retailers promote to consumers in Europe. This can be a improvement that can nonetheless occur in 2023,” concludes Holleman.

[ad_2]

Source link