")

Klaus Vedfelt/DigitalVision by way of Getty Photographs

Ever for the reason that pandemic light, Uber (UBER) has made its dominance clear. The mobility big’s supply bookings have continued to develop as customers’ attachment to takeout orders has endured, whereas a return to cities has made rideshare demand strong once more.

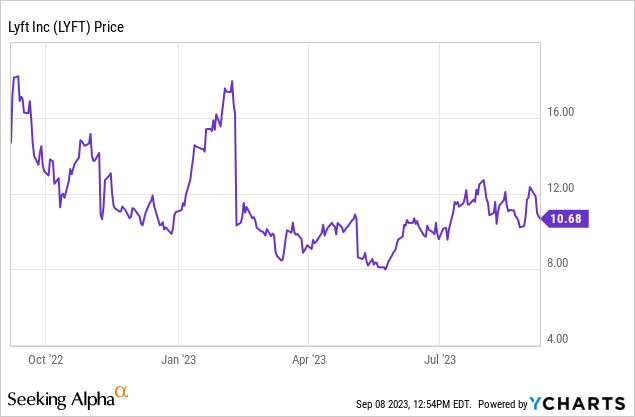

Lyft (NASDAQ:LYFT), in the meantime, has light to the background. The #2 participant within the rideshare area, Lyft has seen its share worth decline within the single digits this 12 months whereas Uber inventory has almost doubled – reflecting the divergence of fortunes in two firms that many American riders considered neck and neck within the race.

To its credit score, Lyft has adopted a prudent technique to compete on this enviornment: shrink, deal with a number of core markets, and worth aggressively in these markets to face on equal footing with Uber. On the identical time, the corporate has launched into large layoffs protecting almost 30% of its headcount, which has pushed the corporate to minor adjusted EBITDA profitability.

After going by means of Lyft’s newest Q2 earnings outcomes (launched in early August, and which did little to both reassure traders of Lyft’s future or spell imminent doom for the corporate), I stay impartial on the inventory as per my prior opinion.

Nevertheless, I do assume a number of the key concerns for each the bull and bear instances have modified, even when they continue to be balanced. A few of the core issues that traders ought to take into account, beginning with the positives for Lyft:

- On high of prudent expense administration, Lyft has additionally amassed fairly a large money stability. The corporate has $1.70 billion of money on its stability sheet, or $890 million of internet money after stripping out $808 million of debt. On high of small adjusted EBITDA income and average money burn, Lyft has time and liquidity to refine its aggressive technique.

- Lyft has constructed a community of partnerships and loyalty drivers to retain a core consumer base. Partnerships with Chase Final Rewards and airways together with Delta (DAL) and Alaska (ALK) has given Lyft a pool of devoted customers, so there’s potential for Lyft to proceed serving this loyal market even when smaller than Uber’s.

On the identical time, nevertheless, we’ve got to be cautious of the next:

- Lyft’s development pales Uber’s, even at a a lot smaller scale. Lyft is a few quarter of Uber’s scale and it is rising slower, and in a enterprise that depends on community results and economies of scale, this may occasionally show to be dire if performed out over time.

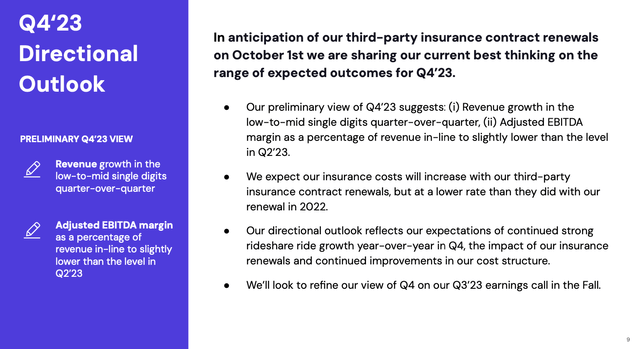

- Insurance coverage renewals are anticipated to throw a wrench in Lyft’s profitability. Larger prices right here could threaten the corporate’s current price-competition technique with Uber.

Extra particulars on the above within the snapshot beneath, taken from the corporate’s current Q2 earnings deck:

Lyft This fall directional outlook (Lyft Q2 earnings deck)

Adjusted EBITDA margins of ~4% are already fairly slim, so a shock right here in insurance coverage renewal prices could threaten the corporate’s current streak of minor income.

The underside line right here: there is not a transparent incentive to stay invested in Lyft or make a giant new wager on it. Lyft could also be interesting if the inventory declines for no purpose, however after the current summer time rally again up previous $10, I do not see a worth alternative right here. Maintain this on the watchlist, however stay on the sidelines.

Q2 obtain

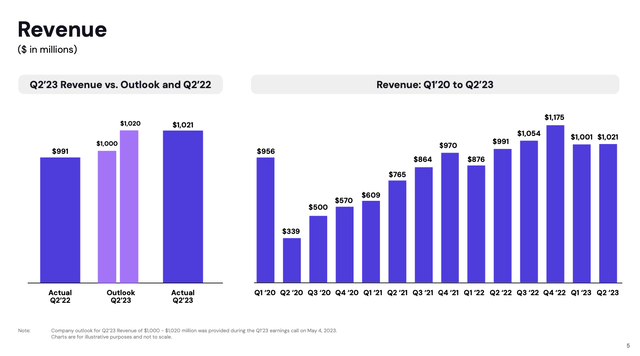

Let’s now undergo Lyft’s newest Q2 ends in better element. The newest income tendencies are proven within the snapshot beneath:

Lyft Q2 income tendencies (Lyft Q2 earnings deck)

Lyft’s income grew 3% y/y (and a couple of% sequentially) to $1.02 billion, which was primarily in-line with Wall Road’s expectations and on the excessive finish of the corporate’s personal steerage.

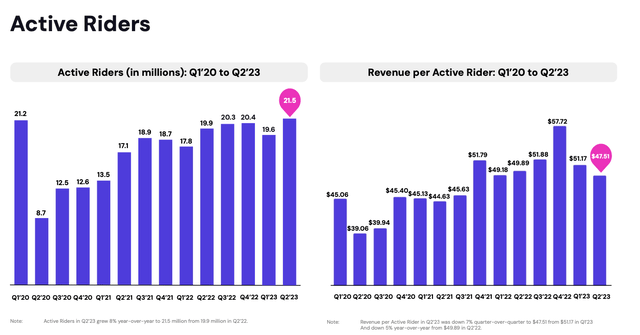

Lyft Q2 energetic riders (Lyft Q2 earnings deck)

And as proven within the view above, the place Lyft excelled this quarter was returning energetic riders to 21.5 million (as a reminder right here, an “energetic rider” is outlined by an individual who has taken at the very least one experience throughout this era). It is a direct results of reducing costs within the markets the place Lyft has deemed it is ready to compete with Uber.

The end result, nevertheless, is a drop in income per energetic rider to $47.51: a -5% y/y decline, and a ~$4 sequential drop.

Right here is extra commentary on rider habits from CEO David Risher’s remarks on the Q2 earnings name:

First, our buyer obsession and deal with robust execution is admittedly paying off. The results may be seen in our Q2 efficiency. Rideshare rides grew 18% year-on-year, accelerating for the second quarter in a row, and customary rides reached the second highest degree in our historical past. Lively rider and drivers, every reached multiyear highs, leading to an improved stability in our market. So relative to Q1, the share of rides affected by prime time pricing dropped by 35% and a bigger proportion of experience intents transformed into rides taken. With extra individuals getting out to work and journey, the market is rising. And with the energy of our actions, they’re more and more selecting Lyft.”

The corporate notes that Lyft’s “wait and save” characteristic (which is extra outstanding than Uber’s, which hardly ever provides the choice) has been a giant stimulator of demand on the platform. On the provision aspect as properly, the corporate has rolled out a lot of new and extra versatile Experience Challenges to incentivize drivers.

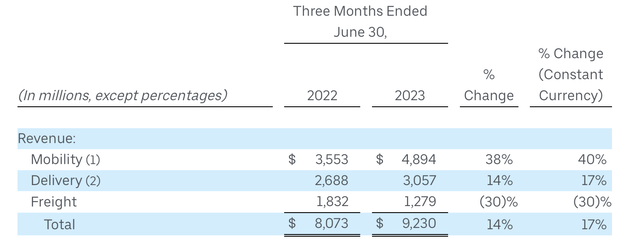

Do word, nevertheless, the sobering proven fact that in the identical quarter, Uber rideshare income grew 38% y/y to $4.9 billion:

Uber Q2 tendencies (Uber Q2 earnings launch)

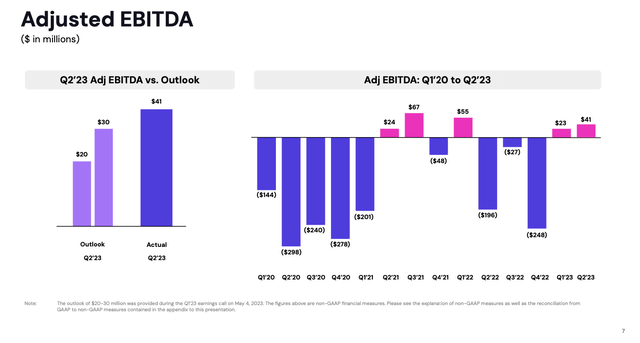

From a profitability perspective, Lyft achieved a $41 million adjusted EBITDA within the second quarter, representing a 4% margin and primarily according to Q1. This was pushed by financial savings on opex, partially offset by decrease income per energetic rider and better insurance coverage prices on a y/y foundation.

Lyft adjusted EBITDA (Lyft Q2 earnings deck)

Valuation and key takeaways

At present share costs close to $10, Lyft trades at a $4.13 billion market cap. After we internet off the $890 million of internet money on the corporate’s most up-to-date stability sheet, Lyft’s ensuing enterprise worth is $3.24 billion.

For subsequent fiscal 12 months FY24, Wall Road analysts expect Lyft to generate $4.84 billion in income, representing a re-acceleration to 12% y/y development. If we take this estimate at face worth, Lyft’s valuation is 0.7x EV/FY24 income. And if we apply the corporate’s newest ~4% adjusted EBITDA margin to this income profile, its a number of could be 16.7x EV/FY24 adjusted EBITDA (word, nevertheless, the unknown dynamics on each insurance coverage prices in addition to the pricing ranges wanted to stay aggressive with Uber to drive double-digit income development).

From this lens, we are able to actually say Lyft is reasonable, however there are loads of query marks on the horizon. I might desire a “watch and wait” strategy right here.