AlphaStreet Newsdesk powered by AlphaStreet Intelligence

FY26 EPS steerage – adjusted $0.35 – $0.41|Inventory $6.31 (+0.0%)

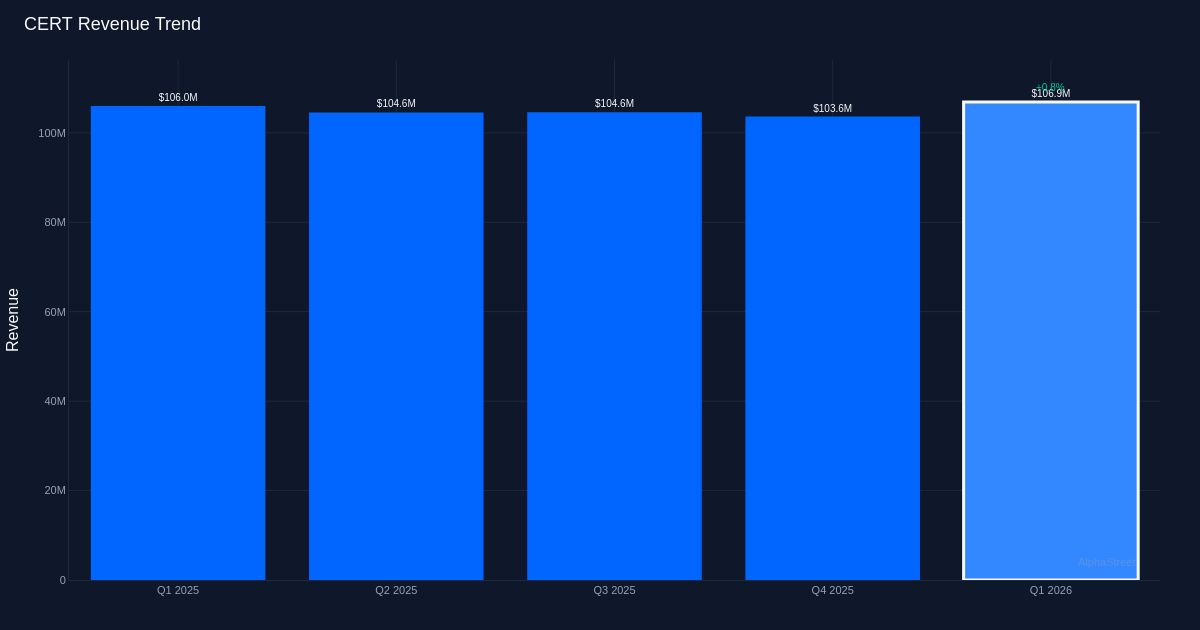

Combined Quarter. Certara, Inc. (NASDAQ: CERT) delivered a break up efficiency in Q1 2026, with adjusted EPS of $0.09 lacking the $0.11 consensus estimate by 18.2% based mostly on estimates from 11 analysts, whereas income of $106.9M edged previous the $106.1M consensus by 0.8%. The well being info companies supplier posted adjusted web revenue of $14.5M. The inventory traded largely unchanged following the report, suggesting traders had already braced for execution challenges.

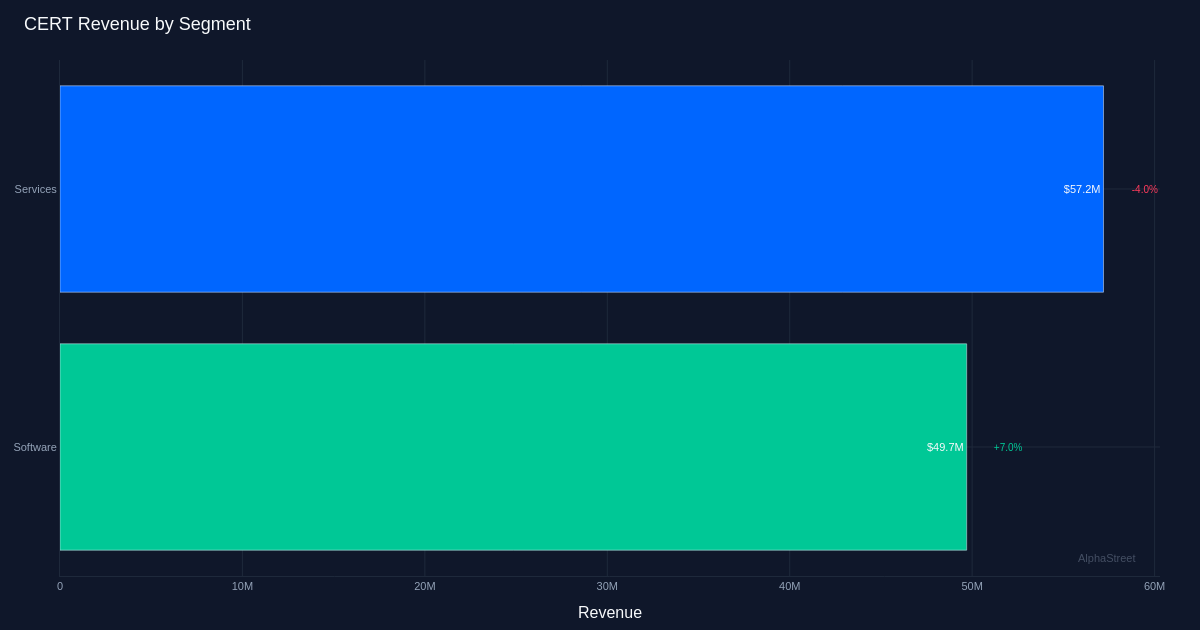

Muted Income Progress. The 1.0% year-over-year income enlargement displays sluggish demand dynamics in Certara’s finish markets, although the corporate did handle to exceed consensus by a slender margin. Whole Bookings reached $115 million for the quarter, a metric that might be crucial to watch for indicators of future income acceleration. The earnings miss seems pushed extra by price construction points than income shortfalls, given the top-line beat, which raises questions on working leverage within the present surroundings. Software program emerged because the clear standout, producing $49.7M in income with 7.0% year-over-year progress, demonstrating that at the very least one phase is gaining traction regardless of broader headwinds.

Steering Gives Restricted Consolation. Administration projected FY 2026 adjusted EPS within the $0.35 to $0.41 vary, whereas income is anticipated to land between $395.0M and $405.0M. The big selection on each metrics suggests significant uncertainty across the firm’s means to speed up progress or enhance margins by year-end. If the quarter’s 1.0% progress charge persists, Certara would want a considerable pickup within the remaining three quarters to succeed in even the midpoint of its income steerage. The EPS outlook, in the meantime, implies important margin enchancment should materialize in coming quarters to offset the Q1 shortfall.

Investor Sentiment Impartial. Wall Road maintains a cautiously balanced view with analyst consensus at 7 purchase rankings and 9 maintain rankings, with no promote suggestions. This break up displays the stress between Certara’s long-term positioning in biosimulation software program and near-term execution challenges. The largely unchanged inventory value following outcomes signifies the market is adopting a wait-and-see posture, unwilling to both abandon the story or reward administration till clearer proof of inflection emerges.

What to Watch: The trail to administration’s full-year steerage hinges on whether or not Software program’s 7.0% progress can broaden throughout different segments and whether or not Whole Bookings momentum builds by Q2, offering visibility into the second-half acceleration required to satisfy income targets whereas concurrently delivering the margin enlargement implied by the EPS vary.

This content material is for informational functions solely and shouldn’t be thought-about funding recommendation. AlphaStreet Intelligence analyzes monetary information utilizing AI to ship quick and correct market info. Human editors confirm content material.