AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Q2 EPS steerage – adjusted -$0.29 – -$0.23|Inventory $66.37 (+45.3%)

EPS YoY +98.7%|Rev YoY +59.3%|Web Margin -40.6%

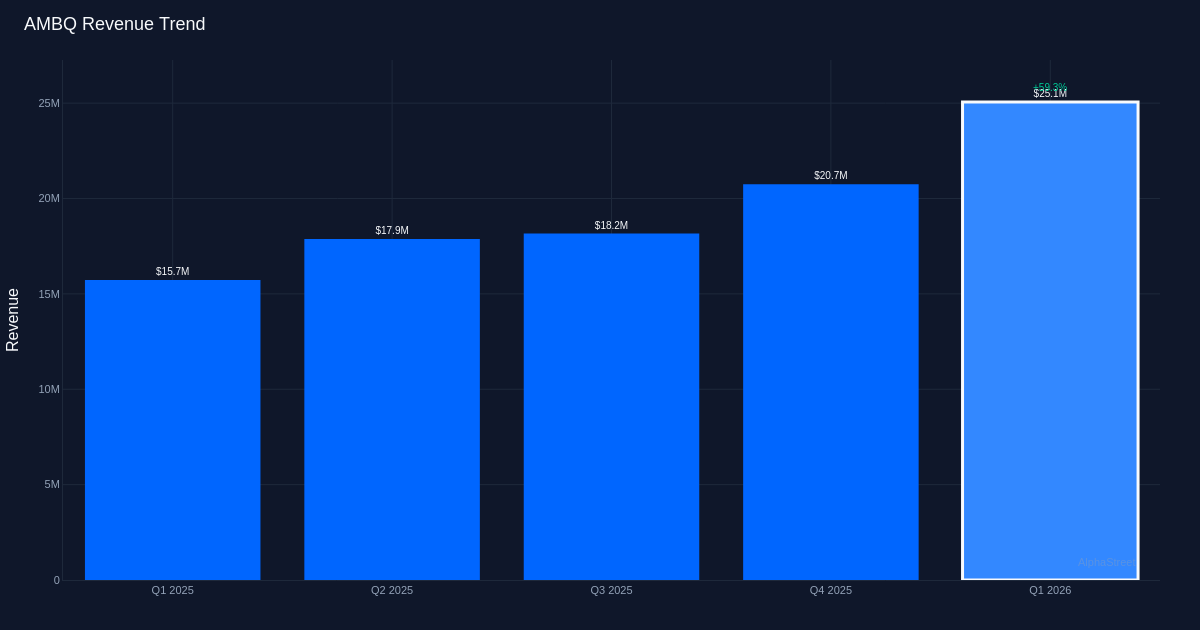

Ambiq Micro delivered a considerable beat in Q1 2026, posting a lack of $0.25 per share in opposition to expectations of $0.36, a 30.6% outperformance that despatched shares hovering 45.3%. The semiconductor firm’s income of $25.1M represented 59.3% year-over-year progress, marking the fourth consecutive quarter of sequential income enlargement. At a present inventory worth of $66.37, traders are clearly betting that the corporate’s momentum in ultra-low-power semiconductors for AI purposes represents a sturdy progress trajectory somewhat than a cyclical bump.

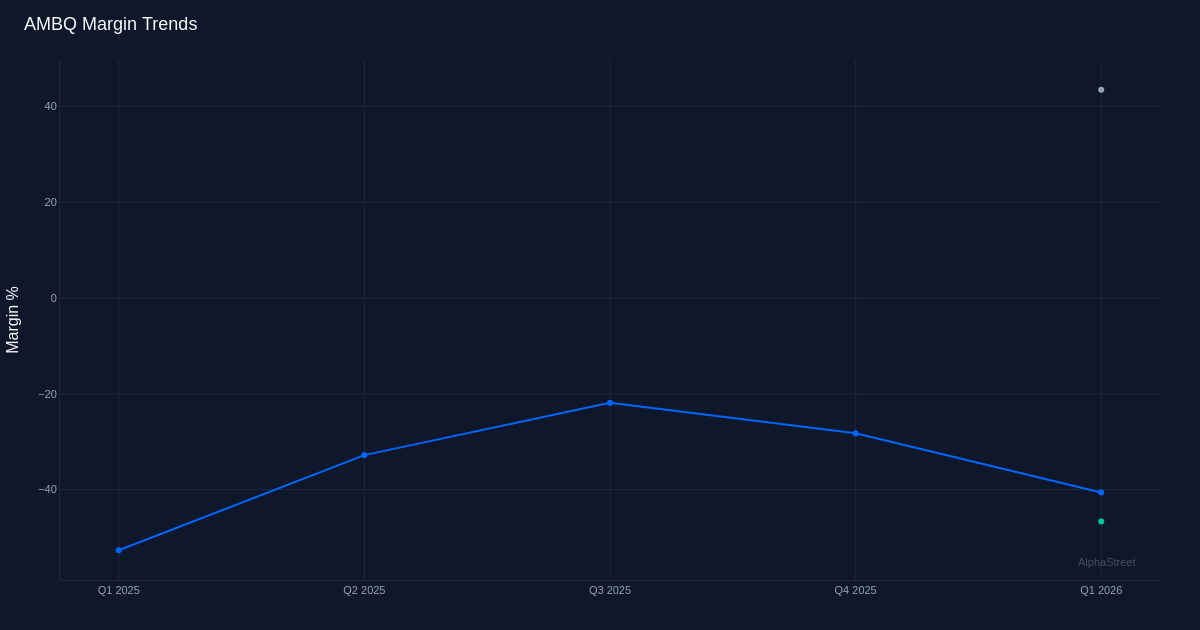

The standard of this beat reveals an organization making significant progress on its path to profitability, although important work stays. The online margin of -40.6% compares favorably to the year-ago determine of -52.9%, representing an enchancment of 12.2 share factors. This narrowing of losses occurred whereas income grew 59.9% year-over-year from $15.7M, indicating operational leverage is starting to emerge within the mannequin. The working margin of -46.6% and gross margin of 43.4% paint an image of an organization with basically sound unit economics on the product degree, however nonetheless carrying substantial mounted prices that haven’t but been absorbed by the income base. Administration famous that spending runs roughly $21 million per quarter at present gross margin ranges, highlighting the stress between funding in progress and near-term profitability.

The shift towards AI-enabled merchandise represents probably the most strategically important improvement in latest outcomes. The corporate reported that 80.0% of models shipped are actually working AI algorithms, a dramatic transformation in product combine that carries profound implications for each aggressive positioning and pricing energy. This isn’t incremental product evolution—it’s a wholesale pivot towards higher-value purposes that ought to theoretically command premium pricing. Administration’s commentary revealed explicit power in market diversification, noting “we grew 100% in a non wearable market” in Q1, suggesting the corporate is efficiently breaking out of its historic focus in wearables to deal with broader IoT and edge computing purposes the place AI performance instructions greater ASPs.

The Q2 steerage framework factors to sustained momentum however requires cautious interpretation. Administration supplied income steerage of $31.0M to $32.0M for Q2 2026, with a midpoint implying sequential progress from Q1’s $25.1M. The underside line steerage of -$0.29 to -$0.23, with a midpoint of -$0.26, implies losses stay elevated relative to the Q1 precise of -$0.25, although this possible displays typical seasonal patterns and funding timing. Administration said “For the second quarter, we anticipate web gross sales to develop roughly 75% 12 months over 12 months with momentum persevering with within the second half of the 12 months,” offering express conviction that progress charges will stay sturdy. The steerage interprets to continued sequential income enlargement, although at what seems to be a decelerating fee from latest quarterly beneficial properties.

Administration’s confidence within the non-wearables enlargement deserves explicit scrutiny. The assertion that “we anticipate to proceed to develop non wearable market as quick as we’ve been doing” following 100% progress in that phase suggests Ambiq is efficiently executing on its technique to diversify past its historic wearables focus. This issues immensely for valuation—wearables signify a concentrated, mature market with established rivals, whereas broader IoT and edge AI purposes supply far bigger TAMs with much less entrenched competitors. The flexibility to take care of triple-digit progress in non-wearables whereas the general enterprise grows 59.3% year-over-year implies the wearables enterprise is probably going rising at a a lot slower fee, elevating questions on long-term combine dynamics.

The money era profile exhibits early indicators of enchancment however stays challenged. Working money circulate of $11.2M in Q1 compares to a web loss, suggesting working capital dynamics or non-cash expenses are offering some cushion. Nonetheless, with quarterly working losses nonetheless substantial, the corporate’s capability to self-fund its progress trajectory with out extra capital raises stays questionable. The 100% beat fee over the past quarter gives restricted statistical consolation, although it does recommend administration has adopted a conservative steerage philosophy following what was possible a difficult interval of misses that preceded the out there information.

The 45.3% inventory surge displays market conviction that inflection is actual, however the valuation now embeds important execution danger. At $66.37, traders are clearly pricing in profitable execution on the AI-enabled product roadmap and continued share beneficial properties in non-wearables markets. The transfer additionally suggests the market views the narrowing losses and accelerating income as sustainable somewhat than transitory. Nonetheless, this optimism creates little room for disappointment—any stumble within the progress trajectory or sudden margin strain might set off sharp a number of compression.

What to Watch: The important thing ahead catalyst is whether or not non-wearables can maintain triple-digit progress charges as the bottom scales, and whether or not the 80.0% combine shift towards AI-enabled merchandise interprets into gross margin enlargement past the present 43.4%. Observe whether or not Q2 outcomes meet the excessive finish of the income steerage vary, which might verify accelerating momentum.

This content material is for informational functions solely and shouldn’t be thought-about funding recommendation. AlphaStreet Intelligence analyzes monetary information utilizing AI to ship quick and correct market info. Human editors confirm content material.